By Brett Munster

Stablecoins are digitizing financial infrastructure

Stablecoins have emerged as one of the most transformative innovations in the cryptoasset space, arguably second only to bitcoin in adoption. While often viewed as a bridge between fiat currency and cryptoassets, stablecoins represent a fundamental shift toward the digitalization of the financial system, offering a new paradigm for global finance that combines the stability of traditional currencies with the efficiency, accessibility, and lower costs of blockchain technology.

Stablecoins are blockchain-based digital assets designed to maintain a stable value, often pegged to a reserve of fiat currency such as the U.S. dollar. The most prevalent model ensures stability by backing each stablecoin 1:1 with a corresponding dollar held in reserve. For every stablecoin issued, an equivalent amount of U.S. dollars is deposited into a bank, and when the user converts the stablecoin back into fiat currency, the stablecoin is destroyed, and the corresponding fiat is returned. This straightforward mechanism has made stablecoins highly effective at preserving value while offering the benefits of digital currencies.

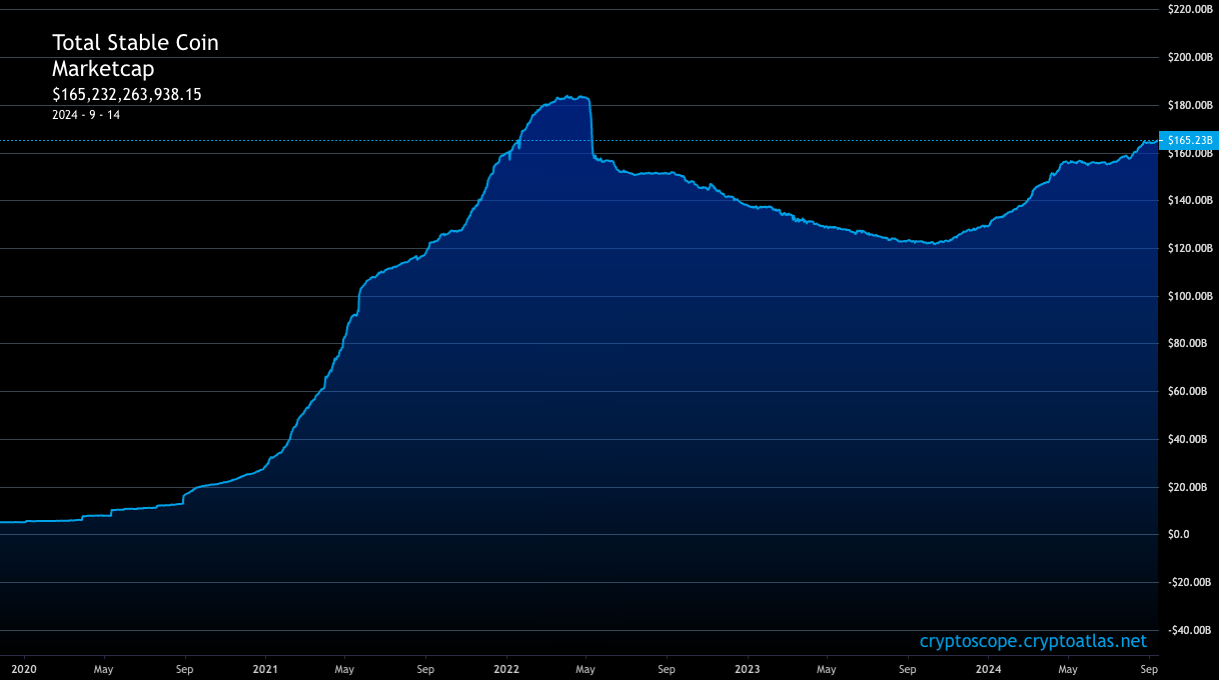

Like other cryptoassets, stablecoins are open, global, and accessible to anyone with an internet connection, eliminating the need for a traditional bank account. However, they offer a distinct advantage over volatile cryptocurrencies like BTC and ETH by maintaining price stability. This has fueled the rapid rise in their adoption. In 2020, the total market capitalization of stablecoins stood at just $5 billion; today, it is nearing $170 billion. This explosive growth highlights not only the rise in crypto trading but also the expanding use of stablecoins in the broader economy. Monthly stablecoin transfers have surged, now exceeding $1 trillion—on par with global payment giants like Visa. Over 120 million blockchain addresses hold stablecoins, with 20 million addresses actively transacting each month.

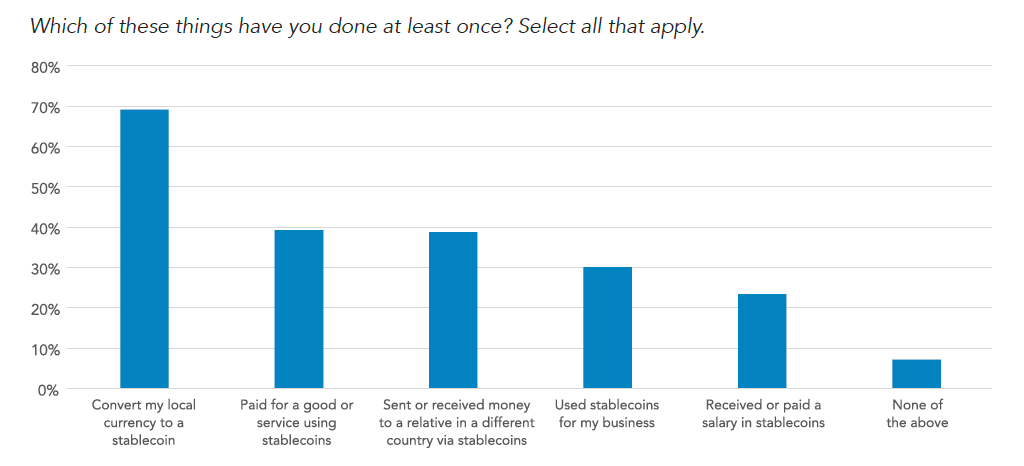

Critics often argue that stablecoins are primarily used for speculative activities within the crypto ecosystem, such as converting fiat to crypto for NFT purchases or trading memecoins. However, the data tells a different story. The remarkable growth of stablecoins is increasingly driven by their utility outside of crypto-native applications. Stablecoins are proving to be valuable digital alternatives to traditional fiat currencies, offering speed, low transaction fees, and accessibility that legacy financial systems cannot match. Consequently, stablecoins are gaining traction in industries far removed from the world of crypto speculation.

One of the most transformative applications of stablecoins is in the realm of cross-border payments and remittances. Traditionally, these transactions have been plagued by slow processing times, high fees, and cumbersome intermediary systems. According to the World Bank, the average global remittance fee stands at 6.4%, leading to an astounding $54 billion in fees annually. Stablecoins, in contrast, enable 24/7 transfers of funds (outside of traditional finance business hours), can be transferred across borders nearly instantaneously and at a fraction of the cost, bypassing traditional banking systems entirely. Payment giants like PayPal and Stripe have integrated stablecoins such as USD Coin (USDC) into their services, facilitating cross-border payments in over 160 countries without transaction fees.

In the e-commerce sector, stablecoins offer merchants a way to accept payments without incurring the 2-3% fees typically charged by credit card companies. This is particularly attractive to small businesses and those operating in regions with underdeveloped banking infrastructure. Stablecoins settle almost instantaneously, allowing merchants to receive payments faster and avoid the delays and fees associated with credit card processing. The transparency and auditability of blockchain technology further enhance this value proposition by providing businesses greater control over their finances. In response to this growing demand, major payment networks like Visa and Mastercard have launched their own stablecoin initiatives to streamline their systems and reduce transaction costs.

Innovative stablecoin issuers are further enhancing the value proposition by experimenting with yield-sharing models, either programmatically on-chain or through third-party arrangements. These models allow stablecoin holders to earn returns, often by passing along the yields from U.S. Treasury bills. This has made stablecoins an attractive option for individuals and institutions that lack easy access to traditional dollar-based money market funds. Institutional-grade offerings, such as BlackRock’s BUIDL tokenized money market fund, even provide 24/7 liquidity through stablecoins, underscoring the growing role of these assets in mainstream financial markets.

Stablecoins are especially valuable in countries experiencing high inflation or with limited access to stable banking systems. A recent study focusing on Brazil, India, Indonesia, Nigeria, and Turkey revealed that stablecoins are increasingly used as alternatives to volatile local currencies and as substitutes for dollar-based bank accounts. Stablecoins offer individuals a way to preserve their wealth in more stable currencies, protect savings from inflation, and bypass government-imposed capital controls. Self-custody of these digital dollars also offers a form of property rights protection, reducing the risk of confiscation or devaluation by local governments.

Stablecoins not only benefit individuals and businesses but also serve critical U.S. government interests. The first benefit lies in their impact on U.S. Treasury bond demand. With rising debt and deficits, the U.S. Treasury has faced challenges in finding sufficient buyers for its debt. Stablecoin issuers like Tether (USDT) and Circle (USDC) have stepped in, purchasing U.S. Treasuries to back their stablecoins. Today, stablecoin issuers are the 18th largest holders of U.S. debt, holding more Treasury bonds than countries like Germany, Australia, and South Korea. This growing demand for U.S. debt provides the Treasury with a new, consistent buyer at a time when global appetite for U.S. Treasuries is waning.

The second benefit is the role stablecoins play in bolstering the global dominance of the U.S. dollar. With de-dollarization trends emerging globally, the U.S. dollar’s share of global central bank reserves has fallen from 73% in 2000 to around 59% today. We are starting to see large countries including Brazil and Argentina enter into bilateral agreements with China to use the yuan and their local currencies for trade settlement. Last year, Saudi Arabia is open to settling oil trades in currencies other than dollars and BRIC nations have openly announced their intention to settle trades in their local currencies in the near future. The asset freeze on dollar holdings in Russia’s central bank imposed after Russia invaded Ukraine, while understandable politically, sent a clear message to the rest of the world who realized for the first time that the dollar may not be the safe store of value it once was. The bottom line is that there is a global push to “de-dollarization” which could threaten the dollar’s reserve currency status.

However, over 99% of stablecoins are currently pegged to the U.S. dollar, meaning the global adoption of stablecoins inherently boosts the demand for dollars. This is particularly important in regions where access to physical dollars is difficult due to capital controls or underdeveloped banking systems. In countries like Venezuela, Argentina, Turkey, and Nigeria, stablecoins have become a vital tool for bypassing local restrictions, offering an accessible and digital way to transact in dollars and offering a form of financial independence. Stablecoins have the potential to give billions of citizens globally direct access to digital dollars that they may not have had before independent of (and perhaps contrary to) their governments’ political decisions. The more stablecoins become a critical part of the global economy, the more entrenched the dollar becomes as the world reserve currency.

By enabling open, global, and instantaneous transfers of value in a fully sovereign manner, stablecoins are driving the modernization of the financial system. Whether it’s remittances, cross-border trade, payroll, e-commerce, or access to U.S. Treasuries, stablecoins are being deployed for a wide range of use cases that have nothing to do with cryptocurrency speculation. Instead, they are reshaping how money moves around the world, making financial services more accessible, efficient, and transparent especially in regions where access to banking is limited or unreliable. With their rapid rise in transaction volumes, user adoption, and integration into traditional payment systems, stablecoins are poised to become a cornerstone of the future financial system, driving the digitalization of global finance.

In Other News

Tokenized treasury funds surpass $2 billion with Blackrock’s BUIDL leading the way.

NFT marketplace Opensea received a Wells Notice from the SEC.

U.S. House Committee plans for several crypto hearings in September.

Ripple CEO predicts SEC Chair Gary Gensler’s exit regardless of who wins the election.

Uniswap settles with the CFTC.

SEC lawsuit against crypto exchange Kraken will proceed to trial but judge ruled that none of the tokens trading on Kraken are securities.

Standard Chartered predicts Bitcoin could hit $125K if Trump wins, $75K if Harris wins, and record highs regardless of US election outcome.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS