By Brett Munster

Change at the SEC is here

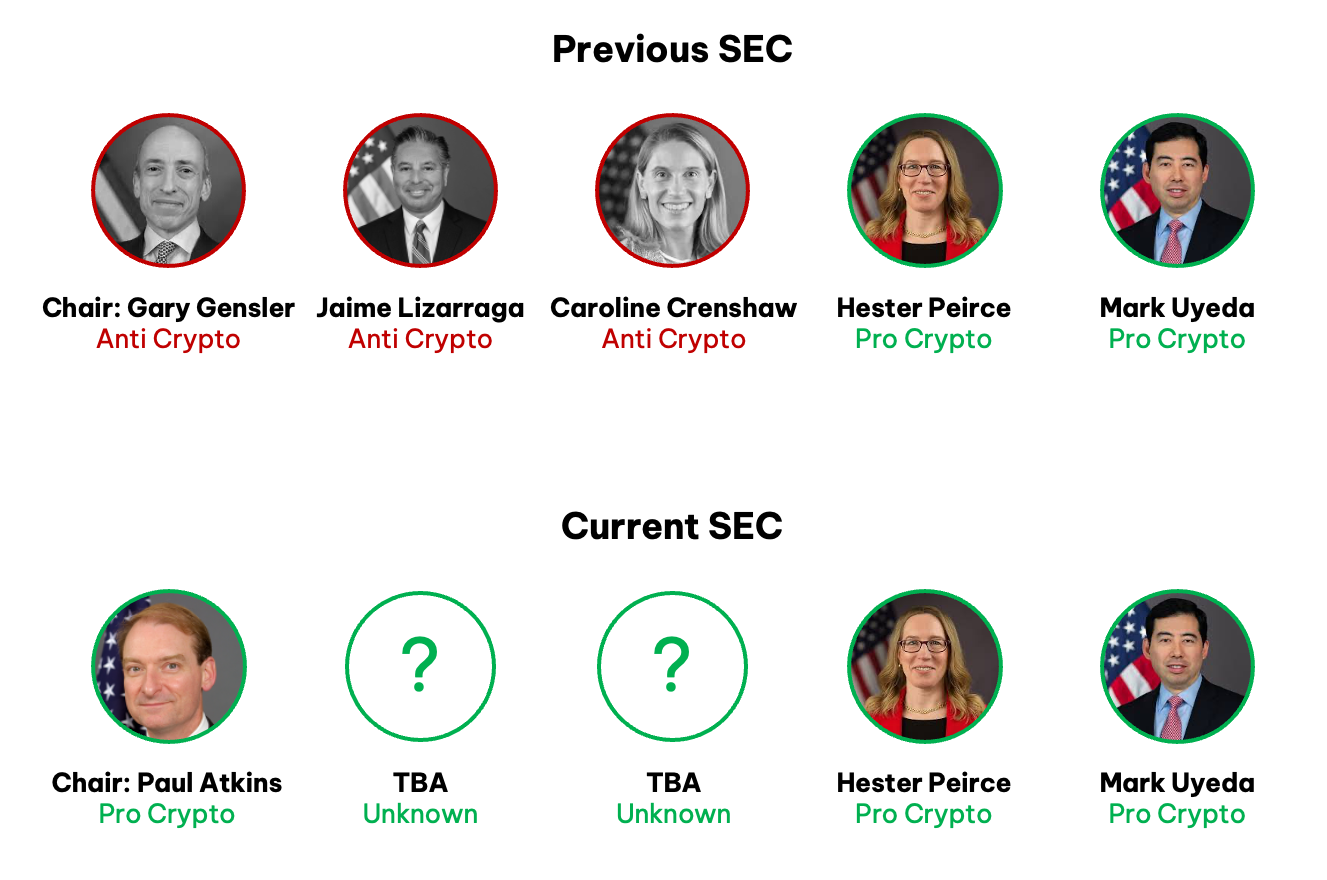

As we have written about countless times in this newsletter, the SEC, under Gary Gensler, was the main antagonist of the crypto industry over the past few years. Rather than providing clear guidance, it chose to regulate through enforcement, suing nearly every major crypto company. It even misled companies by inviting them to “come in and talk to us,” only to use the information from those meetings as the basis for lawsuits against them. Additionally, it prevented banks from custodying cryptoassets through the unlawful issuance of SAB 121, created new legal theories with no precedent, and even went so far as to fabricate evidence in the Debt Box case.

However, with Gensler resigning, Lizarraga stepping down for personal reasons, and Crenshaw not being confirmed, all three anti-crypto members of the SEC are now gone. This leaves the agency with a pro-crypto majority consisting of Peirce, Uyeda, and incoming Chairman Paul Atkins, with two more slots yet to be appointed. Given the current administration’s stance, it is highly likely that both positions will be filled with pro-crypto candidates.

The new SEC is wasting no time in undoing the damage caused under Gensler’s leadership. Within the first week of the new administration, the agency rescinded SAB 121, allowing banks to custody crypto. As a result, BNY Mellon, State Street, and Citi—the three largest custody banks in traditional finance—have all announced plans to launch crypto custody services.

Additionally, the SEC has formed a new task force dedicated to developing a comprehensive and transparent regulatory framework for crypto assets. This initiative is being led by Hester “Crypto Mom” Peirce, who has long opposed the SEC’s previous anti-crypto stance. Peirce is widely regarded as one of the most knowledgeable and fair-minded regulators in this space, making her an ideal choice to spearhead this effort.

The SEC has also voluntarily dismissed its appeal against the dealer rule introduced under Gensler. This rule threatened to stifle the growth of the digital asset industry by making it nearly impossible for DeFi applications to comply with regulations. By withdrawing its appeal, the SEC is signaling a much-needed shift away from its previous pattern of arbitrary and capricious decision-making.

Most importantly, the SEC has already begun dropping its biggest lawsuits. On February 13, the agency officially dismissed its case against Binance. A week later the SEC closed its investigation into NFT platform Opensea and crypto trading app Robinhood. But the biggest announcement was the complete withdrawal of its lawsuit against Coinbase. Notably, Coinbase will not face any monetary penalties or be required to alter its business operations. The case has been dismissed with prejudice, ensuring it cannot be refiled in the future.

It is rare to see a federal regulator capitulate so decisively, let alone three four times in just over a week. This pattern suggests the SEC may also drop its lawsuits against Kraken and Uniswap. While federal courts had already been leaning toward rulings that challenged the SEC’s expansive enforcement efforts, the agency’s voluntary withdrawal of these cases marks a striking departure from its previous hardline stance.

Recent changes at the SEC highlight the significant regulatory shift towards the crypto industry. Numerous regulatory actions have already reversed many of the previous administration’s restrictive policies. While it may take time for new legislation to pass through Congress and for federal agencies to establish official rules, the rapid elimination of existential threats to the industry in the U.S. is well underway. With a more balanced and constructive regulatory landscape emerging, the future of crypto in the U.S. appears brighter than ever.

Rising Global Liquidity

Last October, we published a research article analyzing the relationship between bitcoin and global liquidity. We argued that bitcoin operates with the exact opposite monetary policy of fiat currencies: while fiat has an unlimited supply, bitcoin’s supply is fixed; fiat issuance rates accelerate over time, whereas bitcoin’s issuance rate decreases; fiat’s monetary policy is subject to unpredictable changes, whereas bitcoin’s is immutable and entirely transparent. Because of these characteristics, bitcoin’s value proposition becomes more apparent whenever fiat currency supplies expand and purchasing power is diluted. Historical data supports this view—when the global money supply grows, bitcoin’s price tends to rise as investors seek scarce assets to preserve value.

In that piece, we highlighted the growth in global monetary supply and predicted that bitcoin’s price would follow suit. At the time of writing, bitcoin was trading below $70,000. Just two months later, it broke the $100,000 mark for the first time.

Now, we’re revisiting this thesis because a significant increase in global liquidity is all but inevitable in 2025. Three key factors are driving this trend:

A strong dollar is creating global debt stress

The strengthening U.S. dollar has intensified financial pressure on countries and corporations with dollar-denominated debt, making repayments more expensive in local currency terms. This issue is particularly acute in emerging markets, where weaker domestic currencies exacerbate debt burdens, leading to capital outflows and economic instability. As debt-servicing costs rise, governments and businesses are forced to cut spending or seek bailouts, further straining global growth. These growing pressures create strong incentives for policymakers and international institutions to weaken the dollar—whether through coordinated central bank interventions or policy shifts—to alleviate debt burdens and restore financial stability.

Domestic Incentives to Weaken the Dollar

The strong dollar also poses a challenge to President Trump’s economic agenda, as it undermines efforts to boost American manufacturing and sustain stock market growth. A more expensive dollar makes U.S. exports less competitive internationally, directly conflicting with policies aimed at reshoring industries and reducing trade deficits. Additionally, a strong dollar tightens financial conditions, making it harder to inject liquidity into markets. To counteract these effects, Trump is likely favor policies that weaken the dollar—whether through Federal Reserve pressure for lower interest rates, trade negotiations, or fiscal stimulus—to enhance U.S. export competitiveness and drive economic expansion.

Surging U.S. Deficits and Shift to Fiscal Dominance

With inflation showing no signs of returning to the 2% target and the labor market remaining resilient, the Federal Reserve is likely to maintain higher interest rates for longer. However, these elevated rates have significantly increased government borrowing costs. Since June 2023, the U.S. has added an average of $235 billion in debt per month—roughly $8 billion per day—putting the country on track to reach $57 trillion in total debt by the end of the decade, according to the Congressional Budget Office.

Source: Bank of America Global Research

Interest payments on the national debt are now the fastest-growing expense in the federal budget, surpassing defense spending and highlighting the mounting burden of servicing this enormous liability. According to the Congressional Budget Office (CBO), the U.S. ran an $838 billion deficit in just the first four months of fiscal year 2025, putting the country on track for a staggering $2.5 trillion shortfall by year’s end—a 36% increase from the previous year. At this rate, by 2028, the government will need to inject as much liquidity annually as it did during the COVID-19 stimulus era just to sustain basic operations.

With the Federal Reserve reluctant to cut interest rates due to persistent inflation, borrowing costs are surging, leading to an exponential rise in interest expenses. The result: ever-expanding deficits that will force the U.S. to resort to money printing simply to sustain the system. This marks a fundamental shift from an era of monetary dominance—where central banks steered the economy—to fiscal dominance, where the government’s relentless borrowing dictates policy and threatens long-term economic stability.

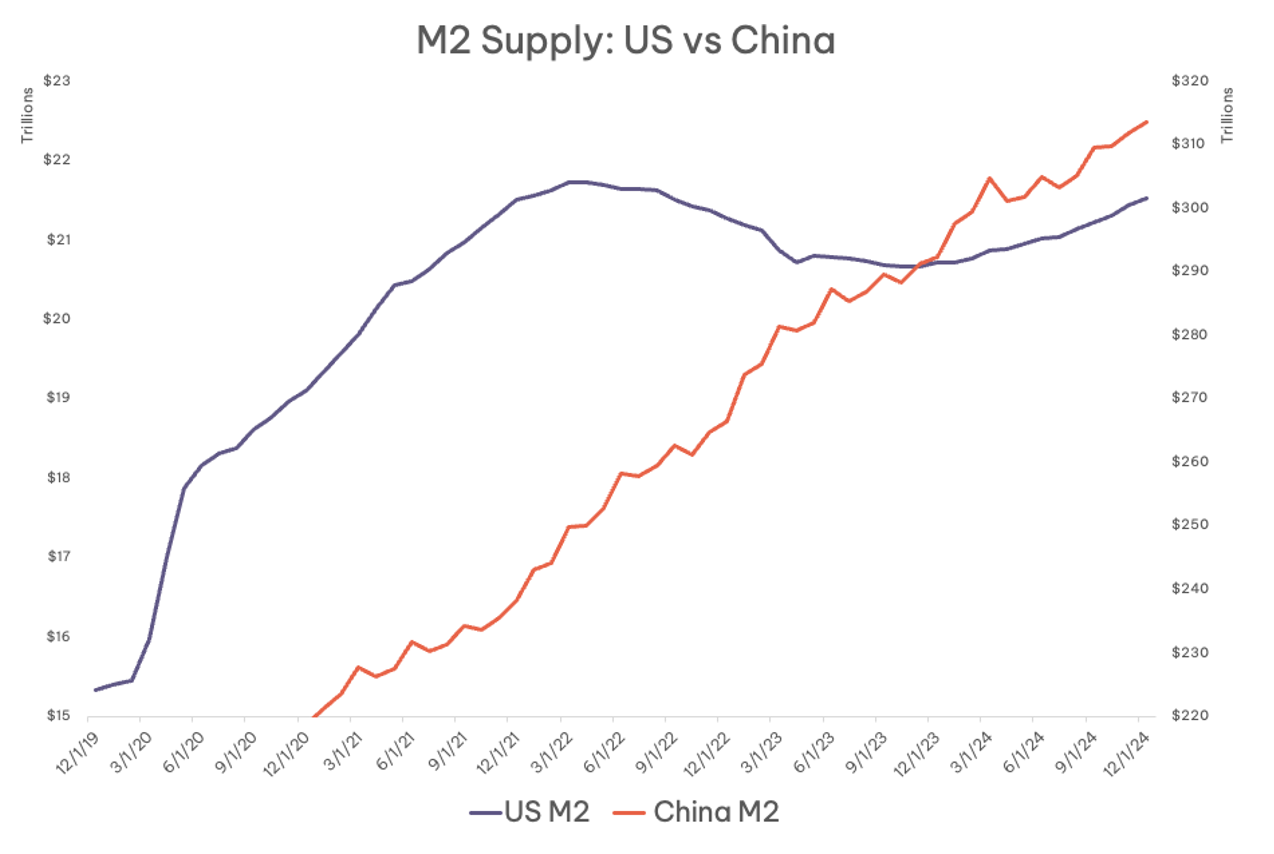

We are already seeing evidence of this liquidity expansion, driven primarily by the U.S. and China. After a period of quantitative tightening, U.S. dollar liquidity has begun rising again, with the money supply expanding in the latter half of 2024. Meanwhile, China’s M2 money supply has been steadily expanding for years as policymakers attempt to revive an economy weighed down by a property crisis, weak consumer demand, and sluggish global trade. The Chinese government has relied on aggressive credit expansion, state-directed lending, and stimulus measures to counteract deflationary pressures and maintain economic growth.

Source: FRED

With rising global liquidity and growing pressure to weaken the dollar, crypto—particularly bitcoin—is poised to be the biggest beneficiary. Its fixed supply and decentralized nature make it a natural hedge against fiat debasement, attracting investors seeking scarce assets to protect their wealth. As mounting debt, fiscal dominance, and currency devaluation drive continued monetary expansion in 2025, crypto stands to gain significantly, further solidifying its position as one of the decade’s most compelling asset classes.

In Other News

US endowments join crypto rush by building bitcoin portfolios.

Trump picks former CFTC commissioner and A16Z policy head Brian Quintenz to head up the CFTC.

US Senate confirms pro-crypto Howard Lutnick as Secretary of Commerce.

Abu Dhabi sovereign wealth fund bought $437 million of BlackRock’s spot Bitcoin ETF.

Trump’s crypto task force is likely prioritizing efforts to create a national Bitcoin reserve.

More than two years after the exchange’s collapse, FTX is sending out creditor repayments, starting with holders who had less than $50K in assets on the exchange.

SEC agrees to dismiss case against Coinbase.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS