By Brett Munster

Crypto Week in Congress

Last week, Capitol Hill was abuzz with what was officially dubbed “Crypto Week,” a coordinated legislative effort that made one thing clear: digital asset regulation is a central priority for U.S. lawmakers. Led by the House Financial Services and Agriculture Committees, the weeklong series of hearings, markups, and votes signaled a bipartisan push to bring long-awaited clarity to how digital assets, particularly stablecoins and broader crypto market structure, will be regulated in the United States. Three major bills took center stage, with two passing the House with wide bipartisan support and a third advancing through procedural steps tied to this year’s defense budget.

At the top of the docket was the cleverly titled Guiding and Establishing National Innovation for U.S. Stablecoins of 2025, or the GENIUS Act. Seriously though, how do you get the job of naming these bills? It might be the only fun job in Washington. But behind the playful name lies a serious milestone: it establishes the first comprehensive federal regulatory regime for stablecoins. The Senate had already passed the bill earlier this year, and on Thursday, July 17, the House followed suit, approving the legislation by a decisive 308–122 vote. A day later, President Trump signed the GENIUS Act into law.

So what’s actually in the GENIUS Act? At its core, the bill requires all payment stablecoins to be fully backed 1:1 by U.S. dollars or short-term Treasury instruments. It formally defines compliant stablecoins as non-securities, placing them under the purview of banking and payment regulators rather than the Securities and Exchange Commission (SEC). That alone could resolve years of legal ambiguity and jurisdictional tug-of-war. The bill also introduces a dual federal-state chartering model, similar to how traditional banks operate. This approach gives issuers flexibility in how they obtain licensing—either through federal regulators or state authorities—balancing oversight with innovation.

While the bill is being branded as crypto legislation, in substance, it’s more about reinforcing dollar dominance in a digital age. Stablecoins have quickly emerged as an effective tool for extending the reach of U.S. dollars into regions with unstable currencies and limited financial infrastructure. They function as digital Eurodollars—providing frictionless, dollar-based transactions worldwide. The mechanics of this system carry deep implications for global finance. Major issuers like Circle and Tether now hold over $100 billion combined in short-duration Treasuries to back their tokens. This makes them significant, repeat buyers of U.S. government debt at a time when traditional foreign demand is showing signs of softening. In effect, stablecoins are emerging as both a strategic tool of U.S. financial influence and a growing source of demand for Treasury markets. The GENIUS Act seeks to lock in and expand that role by providing a clear, secure regulatory foundation—positioning the U.S. dollar to thrive in a digital, globally connected financial system.

The second major proposal on the table was the CLARITY Act, which tackles the much broader issue of digital asset market structure. This sweeping bill outlines legal definitions for different types of crypto assets, establishes guardrails for investor protection, and delineates jurisdictional boundaries between the SEC, Commodity Futures Trading Commission (CFTC), and other regulators. It also sets up a process for digital asset issuers to register new tokens and for exchanges and custodians to operate under clearly defined federal rules.

Unlike the GENIUS Act, which had already cleared the Senate, the CLARITY Act is still early in the legislative process. Nonetheless, it passed the House last week by a solid 294–134 vote, with 78 Democrats joining Republicans in voting “yes.” The Senate is expected to take up its own version of a market structure bill in the coming months, so it remains to be seen whether lawmakers will adopt the House version or merge the two. Either way, last week’s House vote builds momentum and raises the likelihood that a reconciled market structure framework could pass before year’s end.

For many in the digital asset space, the CLARITY Act is the real prize: a long-sought path out of regulatory limbo. Since the collapse of FTX and ongoing enforcement actions by the SEC, the industry has been clamoring for a clear, rules-based environment. With a framework like CLARITY, crypto companies and institutional investors alike could finally operate with the kind of legal certainty that’s standard in other financial markets.

Rounding out Crypto Week was a third piece of legislation: the Anti-CBDC Surveillance State Act. This bill seeks to amend the Federal Reserve Act to prohibit the issuance of a retail central bank digital currency (CBDC) by the Federal Reserve. The proposal is designed to address concerns around privacy and government access to transaction-level data in a retail CBDC system. This week, the bill advanced in the House as an amendment to the must-pass National Defense Authorization Act (NDAA) after a procedural agreement among lawmakers. On July 17, the House passed the amendment with a 219–210 vote, effectively incorporating the CBDC prohibition into the broader defense legislation. The NDAA, now including the Anti-CBDC language, moves to the Senate for further consideration.

Taken together, these three bills represent a turning point in the U.S. approach to digital assets. After years of uncertainty and often contradictory regulatory signals, Congress appears to be coalescing around a more structured, layered framework. Stablecoins are poised to emerge as core components of global payment rails. Market participants are inching closer to operating under unified, federally sanctioned rules. And the debate over digital dollars is now moving out of the abstract and into tangible legislative form.

Not long ago, crypto was dismissed as a passing fad—a speculative bubble destined to burst. Even as the technology matured, institutions kept their distance, first citing volatility, then regulatory uncertainty as reasons to stay on the sidelines. But one by one, those barriers are falling. With infrastructure improving, volatility dampening, and now, with Congress taking concrete steps toward a clear regulatory framework, the final excuse—regulatory uncertainty—is beginning to disappear. That’s what makes Crypto Week such a milestone. It signals that the era of ambiguity is ending and opens the door for large capital allocators, corporations and financial institutions to engage with digital assets at scale. For the first time, there’s a credible path to mainstream adoption—and the capital to match it.

Bitcoin is eating the bond market

For years, bitcoin has been described as “digital gold.” I’ve written extensively about why bitcoin is not only superior to gold but also poised to eventually surpass gold’s $22 trillion market cap. Yet even that label may be selling it short. Calling bitcoin “digital gold” is like calling the internet “digital yellow pages”—technically accurate, but profoundly inadequate. Because bitcoin isn’t just going after gold’s role in the financial system—it’s coming for bonds too.

At first glance, that might sound far-fetched. The bond market, after all, is enormous—valued at roughly $140 trillion globally—and has long served as the cornerstone of conservative investing. But to understand why bitcoin is increasingly relevant in discussions once dominated by fixed income, we need to examine why bonds became so dominant in the first place—and why, since 2022, they’ve been underperforming in a way that may be less cyclical and more structural.

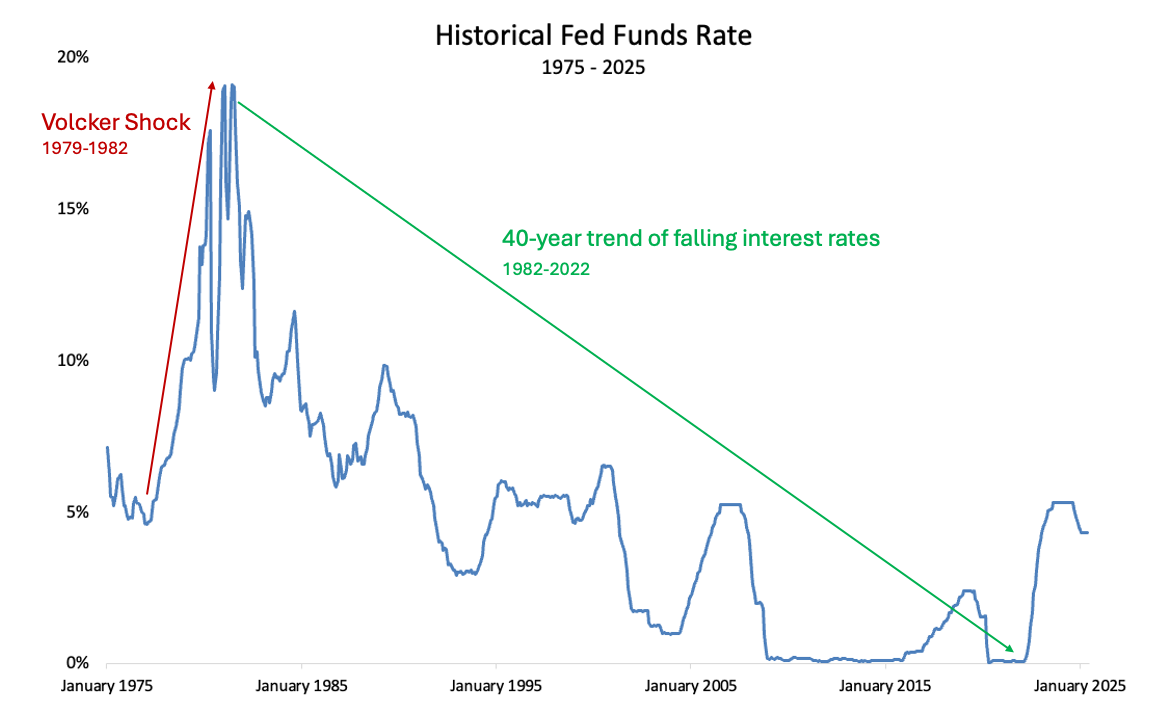

Our story begins in 1979, when the United States was battling double-digit inflation. Enter Paul Volcker, then the newly appointed Federal Reserve Chair, who launched a policy campaign—now known as the “Volcker shock”—that pushed interest rates to nearly 20% by 1981. Once inflation was tamed, the Fed began cutting rates in 1982, initiating one of the most powerful secular trends in financial history: a four-decade-long decline in interest rates. Despite intermittent rate-hiking cycles, the overall trajectory was lower. This culminated in the aftermath of the 2008 financial crisis and again during the COVID-19 pandemic in 2020, when rates were slashed to near-zero.

Because bond prices move inversely to interest rates, this environment created a 40-year bull market for bonds. For generations of investors—both institutional and retail—this was the only market regime they had ever experienced. The 60/40 portfolio (60% equities, 40% bonds) emerged as the gold standard for balanced investing, largely because it consistently worked.

But in 2022, that playbook broke down. When inflation surged, the Fed responded with its fastest rate-hiking cycle in modern history. Bond prices plummeted, and the Bloomberg U.S. Aggregate Bond Index suffered its worst calendar-year return on record. Inflation also eroded real returns, meaning that even as nominal rates rose, investors faced negative real yields. Perhaps most damaging was the failure of bonds to serve their traditional role as a diversifier. In 2022, both stocks and bonds declined in tandem, upending the core rationale behind the 60/40 model. Bonds weren’t just underperforming—they were failing to deliver on their foundational promise of stability.

Since 2022, bonds—particularly long-duration U.S. Treasuries—have continued to underperform. At the same time, the correlation between stocks and bonds has increased, weakening the traditional diversification benefits of fixed income. While some investors view this as a cyclical response to monetary tightening, there are growing indications of deeper structural forces at work. Rising fiscal deficits, heightened concerns about a potential sovereign debt spiral, and a broader shift toward fiscal dominance are challenging long-held assumptions about the safety and performance of government bonds. These dynamics are helping to keep long-term interest rates elevated, reducing the effectiveness of short-term Federal Reserve policy as a tool for influencing broader financial conditions.

This represents a significant departure from historical norms. Typically, when the Fed cuts short-term interest rates, long-term yields—such as the 10- and 30-year Treasury rates that influence mortgage costs—also decline, boosting bond prices. However, that pattern appears to be breaking down. For example, in recent rate cuts—such as the Fed lowering its benchmark rate from 5% to 4.5%—long-term yields have remained elevated or even increased. This isn’t an anomaly; it’s a reflection of a broader market reassessment.

Investors are no longer focused solely on the Fed’s policy stance. Instead, they’re increasingly pricing in long-term structural risks, particularly the growing U.S. national debt and chronic fiscal imbalances. In this new environment, investors are demanding higher yields not just to compensate for inflation, but also to reflect the increased perceived risk to the federal government’s long-term creditworthiness. As a result, we may now be in a regime where cutting short-term rates no longer brings long-term rates down—and could even push them higher, especially if markets believe that lower rates will exacerbate inflation or fiscal excesses.

This environment is defined by what economists call “fiscal dominance”— where government spending exerts greater influence than central bank policy. In such conditions, treasuries no longer serve as reliable hedges against deflation or equity drawdowns. Instead, they carry asymmetric downside risk: limited upside from capital appreciation, and significant exposure to inflation shocks and sovereign credit concerns.

In other words, the era of falling yields and rising bond prices is over. Bonds are structurally disadvantaged, and traditional models like the 60/40 portfolio are less relevant in a world where fixed income no longer behaves as a ballast.

And this brings us to bitcoin.

As bonds falter, investors are looking for alternatives that offer store-of-value characteristics without the built-in erosion of purchasing power. Bitcoin fits this need uniquely well. It is scarce, decentralized, transparent, and immune to debasement. In the current environment, bitcoin is evolving from a speculative asset into the escape valve for a world that’s waking up to the limitations of traditional fixed income.

We’re already seeing early signs of capital rotation. U.S. Treasuries are no longer viewed as sacrosanct safe-haven assets; they’re increasingly treated like risk assets with ballooning liabilities behind them. Even for the institutions that still want to hold bonds, there’s growing talk that new issuances might include a bitcoin “kicker”—a portion of the funds raised used to buy bitcoin, sweetening the pot and helping lower borrowing costs. In this context, bitcoin is starting to appear not just as “digital gold,” but as digital collateral—something that can underpin entirely new kinds of fixed-income instruments.

Enter Strategy, a pioneer in this emerging landscape. With 601,550 BTC—worth roughly $70 billion—on its balance sheet, Strategy is the largest “bitcoin treasury company” in existence. But what’s most notable isn’t just the quantity of bitcoin it holds—it’s how it’s financing those holdings.

Strategy has issued about $8.2 billion in debt, along with another $3 billion in preferred equity. While technically classified as equity, the structure of those preferred shares (fixed dividends, limited upside, and perpetual terms) means they behave economically much like debt. For simplicity, let’s just call it $11 billion of obligations.

That might sound like a lot—until you realize Strategy has nearly than seven times that amount in bitcoin backing it. With a debt-to-asset ratio of just 16%, the company is far less leveraged than most publicly traded firms, which typically fall between 30–60%. Even if bitcoin’s price were to drop by 50%, Strategy’s balance sheet would still be healthier than most of the S&P 500. And for those whispering about liquidation risk—run the math. Bitcoin would have to fall below $13,000 (an 89% drop), stay there for an extended period of time because most of Strategy’s debt won’t mature for several years, and the company would have to be unable to raise any additional capital for the company to face serious liquidity concerns. That combination of events is increasingly implausible given growing institutional adoption and structural tailwinds for bitcoin.

More importantly, Strategy’s approach flips the conventional bond model on its head.

Unlike traditional corporations that raise debt to fund operations or pursue speculative growth, Strategy uses debt to acquire a highly liquid, appreciating asset: bitcoin. Its obligations are overcollateralized—not backed by uncertain future cash flows or operational risk, but by an asset that it already holds on its balance sheet. The genius of Strategy’s model is that it isn’t selling its bitcoin—it’s leveraging it as collateral. This approach flips the conventional corporate finance playbook on its head, and the results speak for themselves: Strategy’s bonds have consistently ranked among the top-performing corporate debt instruments in the market.

In today’s fixed income landscape, that makes Strategy’s debt offerings remarkably unique, combining some of the lowest credit risk with some of the highest returns. It’s no surprise that their bond issuances are routinely oversubscribed, with demand far outpacing supply. There is simply no other fixed income product that offers this blend of asset backing, yield potential, and downside protection.

And here’s the kicker: these bonds remain unrated. That technicality excludes over 90% of fixed income investors—such as pension funds, insurers, and mutual funds—who are often mandated to invest only in rated debt. But that may soon change. Strategy is reportedly working to secure official ratings for its bonds. If successful, it could unlock a tidal wave of institutional capital. Bitcoin has a market cap of just over $2 trillion but the global corporate bond market is $35 trillion. If even a sliver of that pool reallocates into bitcoin-linked instruments, it could significantly move bitcoin’s price.

This creates a powerful flywheel. The more debt Strategy issues, the more bitcoin it can acquire. As bitcoin’s price rises, Strategy’s balance sheet strengthens, lowering credit risk and making its debt even more attractive. Traditional issuers—like Boeing or Nike, which rely on operational cash flows to meet debt obligations—suddenly look less appealing. Why lend to a company that has to earn the money to pay you back when you can lend to one that already holds nearly 7x the capital in reserves?

We are witnessing the early stages of a massive shift in capital markets. The bond bull market, built on the back of ever-declining rates and fiat stability, is deflating. What rises in its place may not be more of the same—but rather, a new class of financial instruments backed by hard, transparent, and digitally native assets.

Bitcoin-backed bonds, ETFs, and treasury strategies are likely to proliferate as investors seek assets that offer both resilience and yield in an era where traditional fixed income increasingly falls short. How big could this shift be? If bitcoin were to merely match gold’s $22 trillion valuation, it would imply a price of over $1 million per BTC. But the global bond market is more than seven times larger. Like gold, bonds are primarily held for capital preservation and risk management—functions that bitcoin is increasingly positioned to fulfill. While bonds also offer yield, in today’s macro environment that yield often fails to keep pace with the rate of dollar debasement.

Bitcoin is not just digital gold. It’s digital collateral and digital monetary infrastructure. As capital markets adapt to a world where traditional safe assets are no longer risk-free, bitcoin’s neutrality, transparency, and scarcity may position it as a cornerstone of the next era in global finance.

In Other News

Strategy is expecting to report a Q2 gain of over $14 billion on its BTC holdings.

SEC’s Hester ‘Crypto Mom’ Peirce says tokenized stocks are securities.

Spot bitcoin ETFs surpass $50 billion in cumulative net inflows amid institutional demand surge

Bitcoin hits new all-time high above $117,000, spot BTC ETFs see nearly $1.2 billion in daily inflows amid “increased institutional appetite.”

Bitcoin surpasses Amazon to become the fifth largest asset by market cap with recent new all-time highs.

Coinbase stock soars to new all-time high following stablecoin GENIUS vote, Base App rebrand

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS