Brett Munster

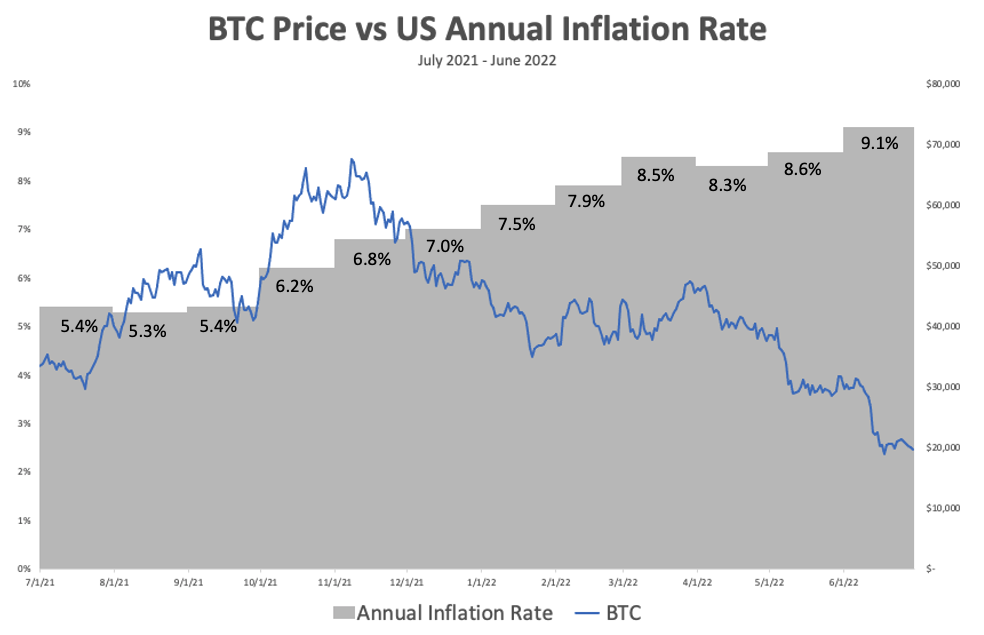

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by consumers for a basket of goods. It is also the most common metric for measuring inflation. Since the start of the year, CPI has risen to 9.1% as of June, which is the highest it’s been in over 40 years. During that same time span, bitcoin’s price has fallen roughly 51% causing many to question the narrative of bitcoin as a viable hedge against inflation.

Before we can analyze whether bitcoin is a viable inflation hedge, we need to start with why the narrative exists in the first place. The short answer is that bitcoin’s monetary policy is the exact opposite of every government backed fiat currency that exists, including the dollar. Whereas the US government can print an “unlimited” amount of dollars, bitcoin has a capped supply of 21 million coins. Whereas the amount of newly created dollars has been increasing over time, bitcoin’s supply issuance gets cut in half every four years. Furthermore, because bitcoin’s supply issuance is programmatic, we know with a high degree of accuracy when every new bitcoin will be issued between now and the year 2140 (the year the last new bitcoin will be released). Compare that to the dollar where we do not have clarity over the next 12 months let alone the next 100+ years. Whereas a small group of unelected officials decide behind closed doors how many dollars to print and when, bitcoin’s supply issuance decision is written in code and transparent for all to see. But most importantly, whereas the US government can change its monetary policy whenever it likes (and does so frequently), bitcoin’s monetary policy is constant and cannot be changed by a single entity.

It’s clear that bitcoin’s monetary policy is in direct contrast to that of fiat currency. Hence, it stands to reason that it should act as a hedge against fiat debasement.

And that’s the key, bitcoin is an excellent hedge against the debasement of the dollar (or any other fiat currency). However, the definition of the term “inflation” has expanded from currency debasement to include any price increase that impacts consumers or businesses. While printing more money does cause purchasing power to decrease, it’s not the only thing that can cause price increases.

Let’s return to the often-used inflation metric we highlighted at the start. CPI is simply a measurement in the change in price for consumer goods. Anything that causes prices of consumer goods to rise will be reflected in CPI. But here is the thing, price increases can be caused by either an increase in demand or a decrease in supply of consumer goods and bitcoin is only a hedge against one of those causes.

Let’s start with demand driven inflation. As a government prints more money, more cash is available to spend on goods and services within an economy. If, however, the output of those goods and services doesn’t also increase, then demand will outpace supply and prices will rise. Hence, if the money supply increases at a faster rate than the economic output, the result is inflation due to an increase in demand. This is what people typically refer to when they claim “bitcoin is an inflation hedge” even though what they really mean is “bitcoin is a hedge against monetary expansion.”

However, prices could also rise due to a decrease in the aggregate supply of goods and services. If the supply of raw materials experiences a sudden decrease (ie: severe weather conditions wiping out crops) or production of a good decreases (ie: lockdowns due to a global pandemic), then the cost of those raw materials will rise. In turn, the production cost of the final product will also rise and very often those costs will be passed onto the consumer resulting in inflation. A famous example is the oil crisis in the 1970s where OPEC increased the price of oil while demand for oil remained constant. The result was the price of finished goods also increased.

While bitcoin acts as a hedge against inflation caused by loose monetary policy, nothing about bitcoin is a hedge against the supply of raw goods dropping or production decreasing. Hence, bitcoin is not a hedge against supply driven inflation forces.

Which brings us to today. The increase in CPI over the last year or so has likely been caused by a combination of both monetary expansion and supply issues. I will leave it to people much smarter and more well versed in macroeconomics than I to debate which factor has had a greater impact on the recent rise in CPI. But the truth is today’s inflation is likely due to a mix of both factors. On the demand driven side, the Fed printed a record amount of money in a short period of time. It’s also true that the supply side has contributed to the inflation we are currently experiencing. The shutdown due to COVID resulted in less production of goods. In addition, the Russia / Ukraine war has disrupted the supply of raw materials such as oil (Russia is the 3rd largest oil producer in the world), wheat (Russia is the 3rd largest wheat producer in the world and Ukraine is the 8th), corn (Russia and Ukraine combine for 17% of the worlds corn production), fertilizer (Ukraine is Europe’s largest supplier of ammonia which is a key component of fertilizer) and more. The ongoing war has caused a drastic reduction in a number of key raw materials in the global economy leading to price increases (have you been to the gas pump recently?).

As we just described, bitcoin would be a hedge to only the money printing part of the equation, not the supply driven issues. In theory, this explains why bitcoin can still be a reliable hedge against currency debasement even though bitcoin’s price has fallen while CPI has risen.

Now, that’s all well and good in theory, but we need to test this hypothesis and see what the data says. If our theory is true, bitcoin’s price should increase when the Fed decides to print money and fall when it starts to tighten. And in fact, that’s exactly what the data shows.

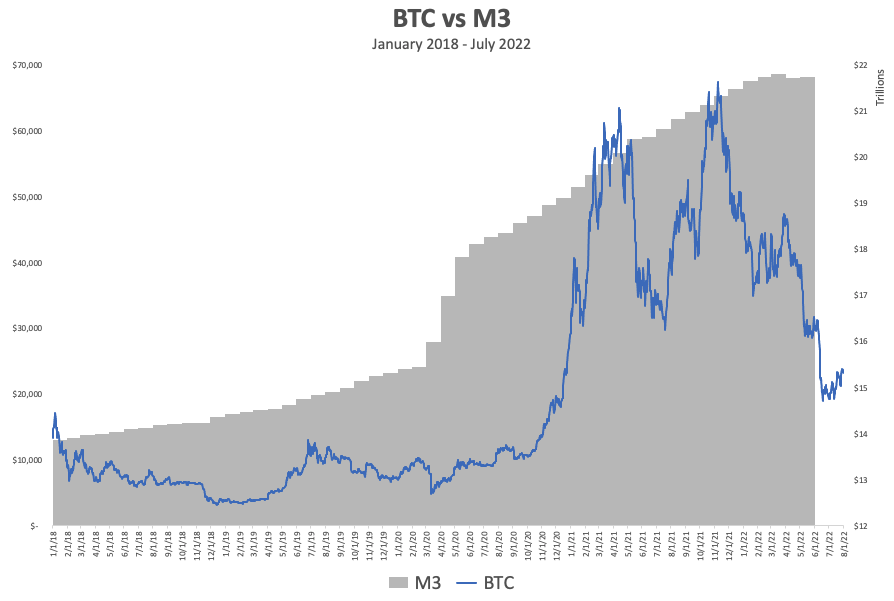

In a recent post, economist Jan Wustenfeld compared bitcoin’s price to M3 rather than CPI in order to determine if bitcoin is in fact a hedge against monetary inflation. M3 is a measure of the money supply in an economy. Thus, by using M3 as our comparison, we can focus solely on how bitcoin reacts to monetary inflation rather than using CPI which has other factors embedded in it that could distort our findings.

In early 2020, M3 shot up as a result of the stimulus response to the pandemic. Not long after, bitcoin’s price also exploded upwards. In mid 2021, M3 started to flatten out for a short period of time and that corresponded with bitcoin’s fall in price. When M3 started to grow again in the back half of 2021, bitcoin rebounded in price. Similarly, when the Fed tightened its policy earlier this year and M3 began to decrease, bitcoin once again fell in price.

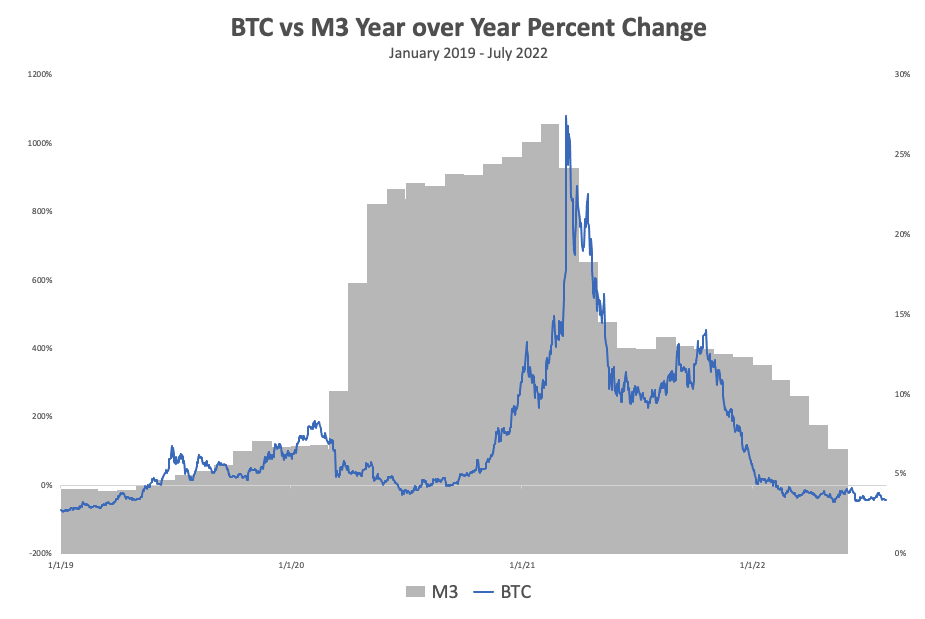

Jan then took his analysis a step further by highlighting the percentage change from the previous year in which the correlation is much more prevalent. As we can see in the chart below, as the year over year change in M3 grew, bitcoin’s price followed shortly thereafter. The percent change in M3 peaked in February 2021 and in March, bitcoin’s percent change peaked as well. As the growth of M3 declined in the back half of 2021, bitcoin’s price followed suit. Recently, as the Fed has tightened its monetary policy, and hence M3’s growth has precipitously declined, so too has bitcoin’s price.

Whereas bitcoin’s price doesn’t appear to be correlated with CPI, it does appear to have a fair amount of correlation with M3. The data suggests that bitcoin is in fact a good hedge against monetary debasement. The reason bitcoin isn’t necessarily a hedge against CPI is because CPI is reflective of more than just monetary expansion, it includes other factors that contribute to price increases that bitcoin may not be a hedge against.

If this is true, it should also be reflected in bitcoin’s performance. For that we need to go back to March 2020 when Congress passed the CARES act injecting $2.2 trillion of economic stimulus into the economy.

Since that time, bitcoin is up 254%. That’s after the craziness of this year and includes the 70% drawdown bitcoin has experienced since its all-time high in November. The bottom line is bitcoin has outperformed every other asset class since the COVID policy response in March 2020. According to the data and bitcoin’s performance during periods of loose monetary policy, it’s hard to argue against bitcoin being a hedge against inflation caused by monetary debasement.

There is one other important factor to take into consideration with regards to CPI and that is time. It takes time for newly created money to make its way into the economy and have an impact. Hence, CPI is a lagging indicator. In comparison, BTC trades 24/7 and reacts to the Fed’s expansion and tightening of monetary policy much faster. Because of this, bitcoin price had already risen before inflation started showing up in the CPI numbers. In other words, bitcoin tends to front run CPI. As CPI started to climb higher, the Fed’s policy changed and predictably, bitcoin’s price fell even though CPI was still rising. Again, there will be some time lag between the Fed’s recent actions and the impact it will have on CPI but bitcoin will react far quicker. Though it’s impossible to know the future, there is good reason to believe that if the Fed changes course later this year or next year and resumes quantitative easing measures, bitcoin will likely react positively to that news before the impact is reflected in CPI.

Bitcoin’s absolute scarcity and predictable supply issuance is the best hedge against monetary expansion of the US dollar and every other central bank-issued currency. However, it is not necessarily a hedge against inflation caused by supply shortages. Between the time lag of CPI and the fact that recent price increases have been caused by a mix of monetary expansion and supply shortages, many people have drawn the wrong conclusion as of late. However, as soon as you understand why bitcoin is such a good hedge and analyze the data, the conclusion becomes much more obvious.

Which leads us to one final thought. If you believe that central banks will continue tightening and the Fed will decrease its balance sheet over the course of the next few decades, then owning bitcoin probably doesn’t make sense. However, if you believe that this recent tightening is a short-term trend and that central banks will revert to their continued policy of monetary expansion (like they have been doing ever since we went off the gold standard in 1971), then bitcoin is likely to do extremely well in the coming years and decades.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS