By Brett Munster

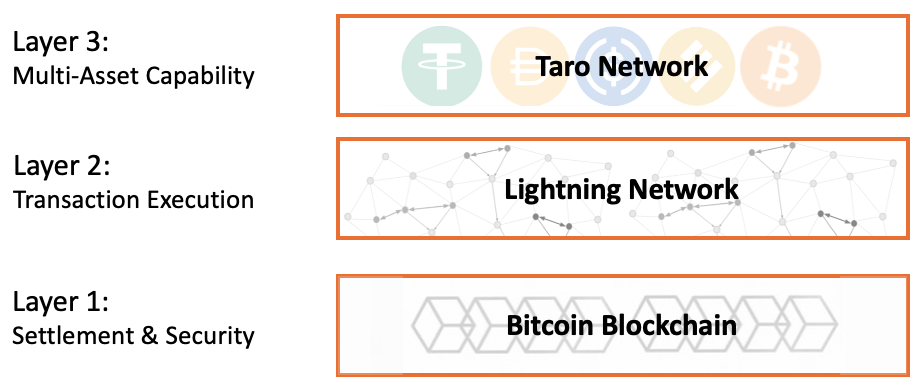

In the first ever edition of The Node Ahead, we discussed the Lightning Network and the rapid growth it was experiencing. As a quick refresher, Lightning is a network of payment channels built on top of Bitcoin’s base layer blockchain that enables instant, nearly-free bitcoin denominated payments to anyone in the world. Then, in November of last year, we covered the Taproot upgrade that went live on the Bitcoin network that improved the network’s privacy and programmability while making transactions faster and less expensive. The combination of those two developments has now led to a new protocol in the bitcoin ecosystem called Taro.

Taro is a new protocol made possible by the Taproot upgrade that allows developers to issue assets other than BTC on the Bitcoin blockchain. Taro also leverages the Lightning Network to transfer those assets instantly and with very low fees. In other words, it transforms Bitcoin’s blockchain from only being able to transact in one asset (BTC) to being able to transfer an unlimited number of assets over its network utilizing the security and stability of the Bitcoin network and the speed, scalability, and low fees of Lightning.

Incorporating other cryptoassets into the bitcoin and Lightning ecosystem should, in theory, bring in more users to the network thus expanding bitcoin’s reach and liquidity. The most obvious, and first use case for the Taro network will likely be stablecoins.

The stablecoin market has grown from $3 billion to over $150 billion in the last three years. Stablecoins have several of the same advantages of other cryptoassets such as being open, global, and accessible to anyone on the internet without the need for a bank account. The additional advantage stablecoins have is that they maintain a constant price (typically pegged to the dollar). Stablecoins are a good choice for sending money across borders without having to pay exchange fees and consumers can earn a much higher yield holding stablecoins compared to traditional savings accounts. Stablecoins also offer the ability for merchants to accept payments without paying the 3% fee that credit card companies charge on every transaction.

However, up until now, none of that has occurred on the Bitcoin blockchain. Most stablecoin activity happened on Ethereum and Tron, each of which has experienced its own set of challenges. Ethereum has experienced high transaction fees and Tron has had security issues in the past. Taro bridges this gap by providing the best of both worlds, the ability to issue assets like stablecoins on the most decentralized and secure blockchain (Bitcoin) and allowing users to transact on the fastest global payments network with the lowest fees (Lightning Network). Thus, Taro has the potential to make it more attractive to use the Bitcoin network for commerce, further increasing its use as a payment network and not just as a savings technology.

Even prior to Taro, we have seen an explosion of growth in the Lightning Network over the last year, especially in Latin America (El Salvador, Guatemala, Argentina, Brazil) and West Africa (Nigeria, Ghana). This is because users in emerging markets do not have access to the same level of financial services or access to the global economy that we are accustomed to in the United States. Bitcoin and the Lightning Network have started to increase that accessibility by enabling anyone with an internet connection to send, receive, and store value without the need for a bank.

Taro takes this a step further by enabling even more financial services to be built on the Bitcoin network. By bringing other assets to the Bitcoin network, users can engage in global commerce using more stable assets such as USDC. In the near future, it will likely be possible to take out a loan and have it entirely facilitated on chain without any middlemen. Credit worthiness and rates will be determined in real time by using on-chain data (collateral, transaction history, etc…) without the need to disclose personal information (name, address, social security, etc…) thus reducing the default rate and minimizing any inherent demographic biases. Don’t be surprised to see the Bitcoin network being used to take out loans for a car, a mortgage, or to start a business in the future. And anyone will have the ability to lend out their assets to earn a passive income. All of this and more will be done on the Bitcoin network using an app (or suite of apps) on a phone and without any bank or middlemen extracting fees.

In time, these financial services are likely to become a seamless experience because Taro enables users to hold BTC, USDC, dollars and any other asset in the same wallet. By enabling developers to provide users with a dollar denominated balance, a bitcoin denominated balance and any number of other assets in the same wallet, it will become trivial to send and receive different assets across the globe. This could potentially drastically increase financial access and innovation for these communities as financial services can be built without the need for banks or third parties. An interoperable ecosystem of assets where users can easily swap between them all could become the catalyst for the next billion or more people to adopt and use the Bitcoin network.

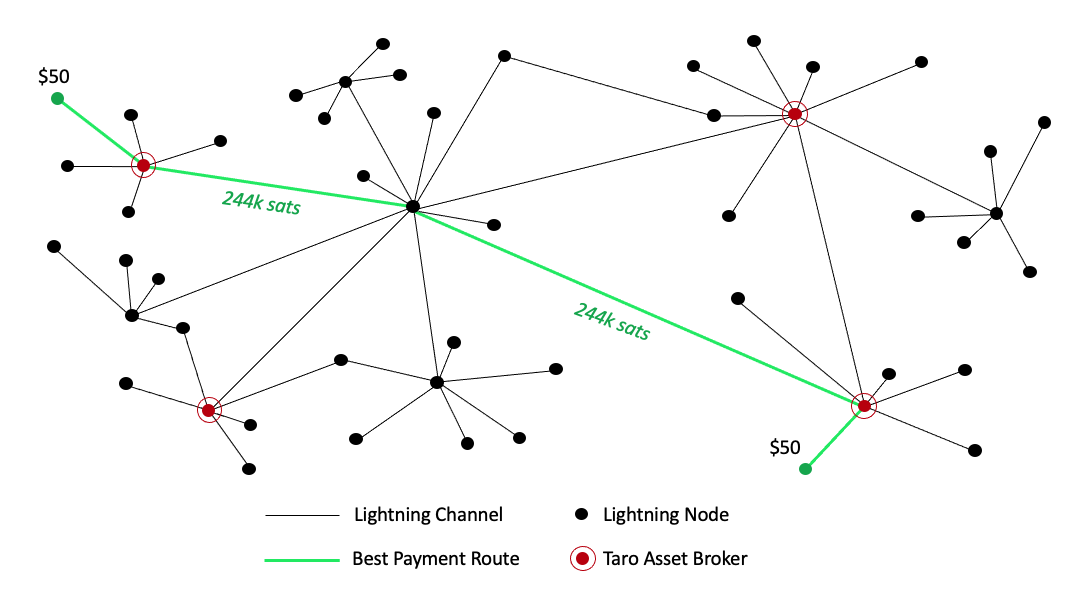

Furthermore, because the Lightning Network uses bitcoin liquidity to route transactions on the network, an increase in the use of Lightning Network due to Taro created assets will result in greater demand for bitcoin on the Lightning Network. In other words, anyone will have the ability to route all the world’s currencies through bitcoin and seamlessly switch between bitcoin, stablecoins, pesos, euros, or yen instantly. For example, it’s possible that in the near future, if I have Apple stock that someone in Europe wants to buy, I could put that Apple stock on Taro, send via the lightning network using BTC to facilitate the trade and receive back dollars even though the buyer paid in Euros. This would all be done with no middlemen, no counterparty risk, near instant settlement and for extremely low fees.

Because Taro uses BTC and Lightning Network as transmittal rails, any increase in demand for transactions across all assets on Taro will increase the liquidity on Bitcoin to facilitate those transactions. Should the Taro network prove to be successful, bitcoin could become the central liquidity pool that everything gets traded through. Rather than trying to incorporate bitcoin into the legacy financial system, Taro is aiming to bitcoinize the dollar (and every other currency for that matter).

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS