Good Morning!

Before we jump into the events of the past couple of weeks, I thought I would highlight a fun fact about bitcoin’s price:

In October 2011, bitcoin’s price crashed below $3

In January 2015, bitcoin’s price crashed below $300

In December 2018, bitcoin’s price crashed below $3,000

In June 2022, bitcoin’s price crashed below $30,000

I know seeing prices fall is never fun and can be nerve wrecking. However, price corrections have historically been a poor indicator of the long term value of bitcoin. The truth is despite the price action, which is currently being driven by macro conditions, many of the underlying fundamental metrics (which we have covered in previous newsletters) are near or at all-time high levels. The network is healthy and adoption is growing. Should the trend hold, I look forward to bitcoin’s price “crashing” to $300,000 in the future.

Comprehensive Crypto Legislation

In our March 22nd and April 5th editions of this newsletter we previewed the highly anticipated, bi-partisan digital asset bill that Senators Cynthia Lummis and Kirsten Gillibrand were working on. Last week, that bill was officially released in a blog post by the two senators. The full text of the bill can be found here.

This bill is by far the most comprehensive and collaborative crypto legislation proposed to date. If passed, the Responsible Financial Innovation Act would be the first federal regulatory framework for digital assets and provide some much-needed legal clarity and regulatory certainty for the industry. This latest version features mostly the same provisions we covered previously including stablecoin requirements, legal and tax framework for DAOs, reporting requirements for early-stage token projects, and tax guidelines including making staking revenue non-taxable until you sell it and allowing for $200 purchases tax free with the uses of cryptocurrency.

The biggest update to the bill appears to be language outlining which digital assets would fall under the jurisdiction of the Commodity Futures Trading Commission (CFTC) vs the Securities and Exchange Commission (SEC). The new legislation provides a framework for classifying cryptoassets as either securities or commodities, with bitcoin, ether and many other cryptoassets falling under the definition of “ancillary assets” overseen by the CFTC. As the announcement emphasizes, “Digital assets that meet the definition of a commodity, such as bitcoin or ether, which comprise more than half of digital asset market capitalization, will be regulated by the CFTC.”

The bill appears to already have bi-partisan support as Lummis is a Republican and Gillibrand is a democrat. Furthermore, the two apparently had months of discussion with fellow senators, including Republicans Mitch McConnell and Pat Toomey, as well as Democrats like Ron Wyden.

Senator Lummis is one of, if not the most, well-educated politicians on crypto. Her home state of Wyoming has been a leader in proposing and passing crypto regulations. She has been an advocate for the industry for years and the work of Lummis, Gillibrand, and their staffs should be applauded. Though this bill will likely serve as a conversation starter for all future crypto policy debates in the US, it has undoubtedly earned Senator Lummis a prominent role in the shaping of that legislation and is a big step in the right direction.

Bitcoin and Human Rights

A couple weeks ago, Norway hosted the annual Oslo Freedom Forum, a global gathering of human rights and pro-democracy activists. The conference is organized by the Human Rights Foundation (HRF) whose Chief Strategy Officer Alex Gladstein is an avid proponent of bitcoin as a tool for ensuring financial rights and freedoms. Alex has written some amazing pieces chronicling real life stories of how bitcoin is protecting human rights around the world which you can read here, here, here, here and here.

The conference’s 13 talks, panels, and workshops illustrated how bitcoin and stablecoins are currently being used by people living under authoritarian governments and countries experiencing hyperinflation. One of the most notable panels was titled “The Quest for Financial Freedom” whose panelists spoke about how they have personally experienced the financial impact of repressive regimes in their respective countries and how they used Bitcoin to protect their savings.

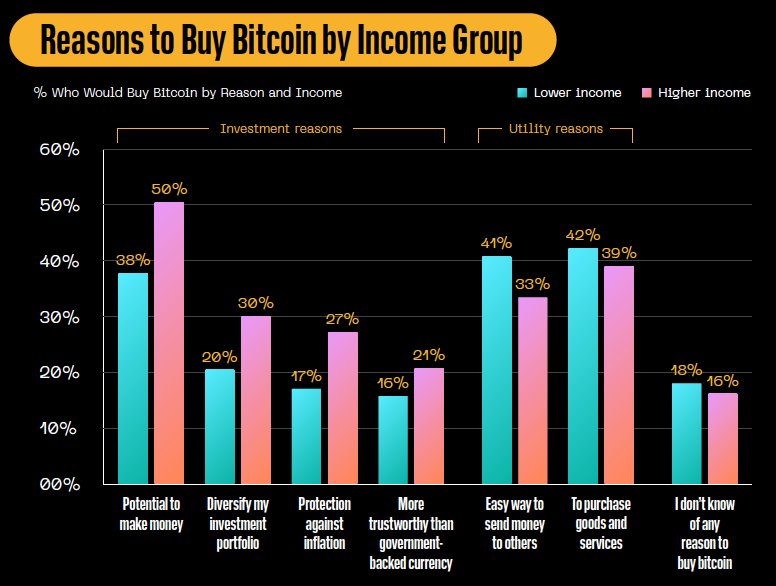

In developed countries, particularly here in the US, where our financial infrastructure works relatively well (albeit inefficiently at times), the primary use case for crypto has been investing. What most people in the US fail to realize is that in many parts of the world, bitcoin is being adopted precisely because it’s a far superior financial system to the status quo . For citizens who do not have access to bank accounts, live under oppressive regimes, or have countries experiencing hyperinflation, bitcoin provides a way to transact safely and store their wealth securely.

This is why 18 of the top 20 countries with the highest crypto adoption are developing nations. In fact, a recent report by Block found that people with below-average income more frequently use bitcoin to send money and buy goods and services than people with above-average income.

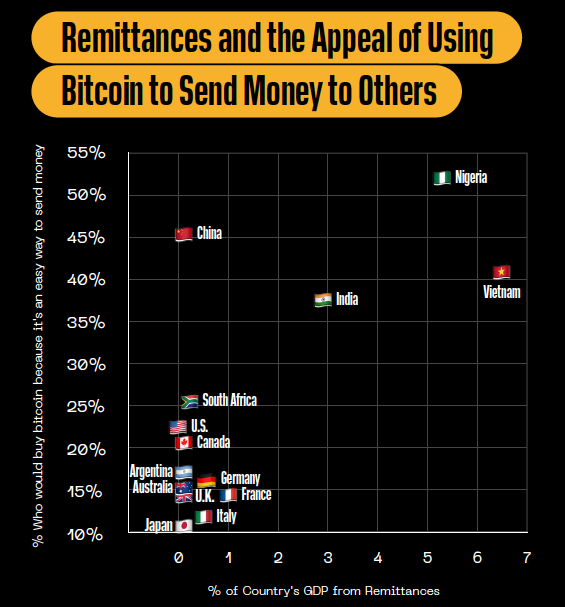

This trend not only holds between income groups but also on a country-by-country basis. Countries with lower per-capita GDP and higher shares of income from remittances have greater rates of people using bitcoin to send and receive money.

Additionally, if we look at the share of people who say that “protection against inflation” is a good reason to buy bitcoin, we see that it is strongly correlated with inflation rates by country, with Argentina leading the pack.

It’s exactly these reasons why human rights activists aren’t just meeting in Norway, but are actively petitioning Congress to learn about bitcoin and its use in nations suffering conflict and hyperinflation. A group of 20 human rights leaders from 20 countries penned an open letter to the congress which stated:

“Bitcoin and stablecoins offer ungated access to the global economy for people in countries like Nigeria, Turkey, or Argentina, where local currencies are collapsing, broken, or cut off from the outside world. When currency catastrophes struck Cuba, Afghanistan, and Venezuela, bitcoin gave our compatriots refuge. When crackdowns on civil liberties befell Nigeria, Belarus, and Hong Kong, bitcoin helped keep the fight against authoritarianism afloat. After Russia invaded Ukraine, these technologies (which the critics allege are “not built for purpose”) played a role in sustaining democratic resistance — especially in the first few days, when legacy financial systems faltered. To claim that the practical value and future potential of cryptocurrencies “does not exist” denies the lived experience of millions of people like us and our colleagues who have depended on bitcoin and stablecoins in times of crisis and autocracy.”

Bitcoin is the first and only globally interoperable financial network. It allows anyone with an internet connection to transfer money faster, cheaper, and more securely without the need of a third-party intermediary including banks. Its monetary policy is transparent, constant and cannot be altered by any single party including government entities. The implications of bitcoin’s technology go far beyond a speculative investment asset, many of which we are only just beginning to see.

NY doubles down

The majority of digital asset regulations passed in the United States have been very pro-crypto. In past issues we have covered how Wyoming, Texas, California, Florida, Colorado, Ohio and many more states have all passed favorable initiatives that have led to economic growth. The most noticeable (and possibly only) exception to this list is the state of New York, which instituted a “BitLicense” in 2015 which required all cryptoasset businesses that wanted to operate in the state to obtain a burdensome license. By all measures, the New York BitLicense has been an utter failure. It’s been widely criticized for crippling New York’s capacity to participate in the crypto sector’s boom and incentivizing companies, talent, and capital to relocate to other jurisdictions effectively limiting job creation and foregoing any tax revenue the state could have garnered. Apparently, the state of New York did not learn any lessons over the past several years.

On June 3rd, the New York state senate passed a bill that establishes a two-year moratorium on the creation of any new crypto mining operations that mine tokens that use a proof-of-work consensus model (aka bitcoin). Unless a company that mines bitcoin uses 100% renewable energy, it would not be allowed to expand or renew permits, and new entrants would not be allowed to come online. The measure now sits at the desk of Governor Kathy Hochul, who could sign it into law or veto it. If Hochul signs the bill, it would make New York the first state in the country to impose restrictions on blockchain technology infrastructure.

The measure was marketed as a way to help curb the state’s carbon footprint. However, the measures passed not only do not reduce carbon emissions, but it actively works against the stated goal.

Those who voted for the bill are making the argument that “bitcoin mining consumes a lot of electricity” and therefore it means more electricity production is needed to power the mining operations which in turn creates more CO2. Again, as we have covered in the past, the data proves that this narrative is false. Global bitcoin mining consumes less electricity than clothes dryers worldwide. If energy consumption is a concern for the state of New York, where is the ban on clothes dryers that do not run on 100% clean and renewable electricity? Bitcoin also uses a fraction of the energy our current financial system does. As we move more economic activity away from the traditional financial structure into digital assets, that will ultimately mean a reduction in the amount of energy consumed.

Furthermore, a significant portion of bitcoin mining relies on excess capacity because that is where miners can find the cheapest source of electricity. It’s difficult for energy producers to increase or decrease their production. Thus, all power plants produce a constant base load of energy regardless of whether that electricity is used. So even if you ban bitcoin mining in New York, that does not lower the energy production and thus does not lower the CO2 emissions.

But the argument against the bill is stronger than that. Because bitcoin miners can be turned on and off at a moment’s notice, bitcoin miners can purchase this excess energy thereby guaranteeing the power plant always has buyers. This is great for two reasons. One, having a persistent buyer allows grid operators to forecast more confidently which results in cheaper energy prices for all. Two, energy sources such as wind and solar have less predictable outputs and bitcoin mining allows renewable energy providers to sell all their power when production is at its highest rather than letting it go to waste. The reality is, bitcoin mining improves the economic model for clean and renewable energy providers!

The irony of this bill is that bitcoin mining is an incredibly great tool to move the grid towards a more climate friendly future. It’s the reason that Todd Kaminsky, the chair of the Senate Environmental Conservation Committee and the author of New York’s “Climate Leadership and Community Protection Act” which requires the state to get to net-zero carbon emissions by 2040, opposed the recently passed bill. Even labor unions are against the bill as it is likely to lead to an exodus of crypto mining companies to friendlier states such as Texas, thereby resulting in loss of high paying jobs and tax dollars moving out of state.

The bill was so unpopular among the constituents that the state senate had to resort to some rather dubious tactics to get it passed. First, they reassigned the bill to get around the Environmental Conservation Committee which as I previously mentioned, was against passing this bill. The senate then reintroduced the bill to the Senate Energy and Telecommunications Committee where one of the bill’s sponsors (Kevin Parker) also happens to be the chairman of the committee. The bill made it to the senate floor in the final hour of the final day of the legislative session thus limiting any chance of opposition.

Beyond simply hurting New York’s economy and chances of achieving their carbon goals, the bill also potentially sets a dangerous precedent. By passing this bill, the New York state senate is claiming that they have the right to dictate to businesses and individuals what is and is not a valid use of the electricity generated within the state. It would be ridiculous to dictate to Amazon or Facebook that they can’t use electricity in New York to run their servers, but that’s exactly what they are doing to bitcoin mining companies who have legally purchased this electricity. Even though those computers are performing similar actions and using the same energy, New York is trying to assert that they can dictate which industries are justified in using electricity and which aren’t.

While nearly every other state in the US is looking to embrace crypto, the center of the traditional financial world seems to be doing everything in its power to limit adoption among its citizens. Though the bill does not prevent any existing miners from continuing to operate, it further establishes New York as a jurisdiction that is much more hostile to the industry than virtually every other state in the US. Talent is already leaving traditional financial jobs and moving to crypto. With these additional onerous regulations, it’s possible that much of the talent and companies that are still located in New York are not likely to stay much longer.

In Other News

Over 400 million PayPal users can now send supported tokens — bitcoin, ether, bitcoin cash and litecoin — to external addresses, including those linked to exchange accounts and hardware wallets.

Deloitte’s “Merchants Getting Ready For Crypto” report reveals that 75% of retailers plan to accept crypto or stablecoin payments within the next two years.

The Fed recently published a paper exploring the impact of issuing a CBDC would have on monetary policy. Part of the findings included the Federal Reserve needing to buy more Treasuries and having a permanently bigger balance sheet.

FTX surpassed Coinbase as the second-biggest centralized crypto exchange in May.

Citadel Securities and Virtu Financial are building a crypto trading platform.

Solana blockchain suffers new network outage.

Kenya’s energy production company KenGen wants to offer bitcoin mining companies its surplus geothermal power.

El Salvador received 521,000 tourists in Q1 who spent more than $352.7 million.

Following President Biden’s crypto executive order in March, the White House Office of Science and Technology Policy (OSTP) is aiming to put out a report on cryptocurrency mining and its environmental impact this summer.

The SEC is examining whether Binance’s initial coin offering of its Binance coin (BNB) token in 2017 was an unregistered security offering.

Grayscale Investments LLC has strengthened its legal team with the addition of Donald B. Verrilli Jr. as the digital asset firm continues its mission to convert its Grayscale Bitcoin Trust (GBTC) into a spot bitcoin exchange-traded fund.

A conceptual framework for examining bitcoin adoption through the context of past disruptive technology adoption cycles in the hopes of more accurately forecasting future growth rates.

Ethereum Ropsten testnet successfully merged to Proof-of-stake.

American Express confirmed that it would be offering crypto rewards credit cards.

Over $135 million in crypto had been raised by Ukrainian funds by mid-May.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS