By Brett Munster

This past month, Blockforce Capital was awarded Best Sustained Risk Adjusted Performance over the past 36 months for digital assets by Hedgeweek. We have won numerous awards over the years but most of those are for monthly or annual performance. What makes this award so meaningful to the team is the recognition of our sustained performance over a longer period of time. We fundamentally believe crypto is a multi-decade long trend that is just starting to play out and we have built the firm with that long-term mindset and focus. We are not here to capitalize on the flavor of the month token or over-leverage into a position simply out of FOMO. Our intent is to build a lasting business that takes advantage of the value appreciation we believe crypto will experience over the next couple of decades and deliver superior risk adjusted returns during that span. This award is nice validation of our long-term focus.

Congress wants answers from the SEC

It was a busy week last week for crypto on Capitol Hill. On March 7th, the Senate Committee on Environment and Public Works hosted a hearing on crypto mining. I particularly enjoyed this exchange from Senator Cynthia Lummis who continues to prove she is one of the most well-educated politicians and first principle thinkers within Washington when it comes to crypto.

That same day also kicked off oral arguments in Grayscale’s lawsuit against the SEC. Last July, we covered the history of GBTC and why Grayscale decided to sue the agency that regulates them. As a quick recap, Grayscale is arguing that the SEC’s decision to deny the $14 billion trust’s conversion to an ETF was “arbitrary,” given the regulator’s prior approval of a futures-based bitcoin ETF back in 2021. The data shows that the SEC’s alleged concerns about manipulation of bitcoin’s price are inconsistent and possibly in violation of the Administrative Procedure Act.

The SEC’s defense didn’t seem to go over very well as judges questioned the agency’s logic in drawing a distinction between bitcoin spot and futures market prices. During SEC senior counsel Emily Parise’s argument, Judge Neomi Rao interrupted Parise saying the SEC needs to better explain the difference the agency sees between bitcoin futures and the spot price of bitcoin. “It seems to me…one is essentially a derivative of the other,” the judge said. “They move together 99.9% of the time, so where’s the gap in the commission’s view?” Judge Rao also said that the SEC had unfairly placed the burden on Grayscale to disprove the chance of fraud in spot markets. Though judgment isn’t expected until Q3, the market reacted positively to the development as shares in GBTC climbed in the hours following the end of the hearing.

Then on March 9th, the newly formed House Digital Assets Subcommittee, which we highlighted in our January 31st issue, held its first hearing titled “Coincidence or Coordinated? The Administration’s Attack on the Digital Asset Ecosystem.” Last issue we analyzed a number of the recent actions by regulatory bodies against several crypto companies and highlighted why some of these actions are problematic. It seems that Congress is also noticing the issues these actions are causing and held a hearing specifically to address U.S. regulators’ policing of crypto companies. Even prior to the hearing, several committee members had publicly criticized the SEC for being heavy-handed. In a recent interview, Gary Gensler claimed that under the Howey test, a Supreme Court case often used to define a security, he believes every token other than bitcoin is a security. However, in January of this year the committee suggested the near 80-year-old standard was not fit for purpose and new definitions were needed for cryptoassets. Then, just weeks before the hearing, two U.S. lawmakers sent a letter to the Federal Reserve and other U.S. banking agencies criticizing the SEC’s accounting policy arguing that it will deny millions of Americans access to safe and secure custodial arrangements for digital assets. Then on March 9th, another group of 4 republican senators sent a letter criticizing a number of regulatory actions against the crypto industry, saying the increasing regulatory crackdown on crypto banking is “punishing an entire industry.”

During the hearing, the committee made a point of expressing that they considered many of the recent actions to be an overreach of jurisdictional authority. There were also a lot of questions regarding the risk of pushing the digital asset ecosystem overseas. “This administration is weaponizing the banking sector to debank legal crypto activity here in the U.S., using scare tactics to run an entire industry out of the country,” said Tom Emmer. “And the collapse of FTX should warn us of the vulnerable position we are putting American consumers in when we don’t compete to keep crypto firms onshore.” While the SEC is regulating by enforcement and driving talent and capital overseas, the UAE, Brazil, Switzerland, Singapore, Hong Kong, the UK and European Union already have or are in the process of creating clear rules for companies.

There was also testimony from BitGo co-founder and CEO Mike Belshe and Coinbase chief legal officer Paul Grewal. Mike Belshe made a poignant argument about the predicament crypto-related companies find themselves in within the US at the moment: “Regulators can either declare that digital assets are regulated in the same way as other assets, and thereby apply the same rules, or regulators can say that they are different, and create new rules. But what regulators cannot be allowed to do is to claim that assets are different, and also claim that the rules are already understood.”

No Silver Lining

Over the last couple of weeks, the largest crypto-friendly bank has crumbled under a mix of regulatory and market pressure. If you have ever bought or sold tokens on an exchange or engaged in the crypto ecosystem, it’s likely you have indirectly interfaced with Silvergate Bank even if you did not know it.

Over the past decade, Silvergate grew from a small regional bank to over $14.7 billion in assets largely due to the fact that it was one of only a handful of banks willing to do business with crypto companies. In addition to simply providing access to standard banking services which many larger US banks were unwilling to do, crypto companies flocked to Silvergate because the bank had also built the Silvergate Exchange Network, known as SEN. SEN enabled instant settlement between cryptocurrency exchanges and allowed users to send USD and euros 24/7 without delay. This network solved a key challenge of easily converting fiat dollars into the crypto ecosystem and vice versa which had long been a sticking point for many crypto related businesses.

During the crypto boom, Silvergate’s business soared as it became the de facto bank for most of the crypto industry. The company went public in 2019 at $12 a share. By 2021, the share price was over $200 and SEN was doing over $400 billion of volume. Silvergate’s clients included crypto’s biggest companies like Coinbase, Gemini, Kraken, Circle, Galaxy, Paxos, FTX, BlockFi and more. Over time, 90% of the bank’s deposits came from the crypto sector alone.

Then 2022 happened. As a result of the market’s substantial decline, crypto investors took their money off exchanges which in turn took it back from Silvergate. The collapse of FTX, which held its bank accounts at Silvergate, further exacerbated the problem to the point where the bank suffered an $8 billion drawdown over the course of the year as its assets fell to $3.8 billion. In order to cover those customer withdrawals, Silvergate sold a large portion of its bond portfolio. Unfortunately, those bonds were worth less than what Silvergate paid for them because interest rates have gone up substantially over the previous year which resulted in a $1 billion in losses in Q4.

The tough financial situation got worse in March of this year when Silvergate announced it had to delay filing its annual 10-K form citing the need for more time to assess its finances. In response to both regulatory uncertainty and concerns around Silvergate’s financials, several of the biggest names in crypto announced plans to reduce or end their relationship with Silvergate. Coinbase, Galaxy Digital, Gemini and Circle made public statements that they had cut ties with the bank.

It’s worth noting that Silvergate collapsed for very different reasons than what we saw last year. Silvergate did not make risky, overleveraged loans like Celsius or commit fraud like FTX nor did any customer lose any money from Silvergate as all deposits will be returned in full. Silvergate’s implosion is due to their customers withdrawing their money because they are worried about Silvergate’s financial position and the recent scrutiny the bank is receiving from regulators. As Matt Levine wrote, Silvergate “lost money, not by making dumb Bitcoin loans — the Bitcoin loans are fine — but by doing the normal business of banking, borrowing short (taking deposits from crypto firms) to lend long (buying Treasuries and munis). Silvergate’s assets are real boring normal stuff, and if its depositors had kept their money at Silvergate, its bonds would have matured with plenty of money to pay them back. Instead, the depositors demanded their money back all at once, and Silvergate had to dump its long-term assets at big losses to repay them.”

As it turns out, the crisis of confidence in the bank was too much for Silvergate to withstand. Last Wednesday, Silvergate began winding down in an orderly manner and making depositors whole. The core problem wasn’t in its banking practices, it was that it lacked diversification in its deposit base and interest rates rose so quickly. The lack of diversification was caused, in part, by the fact that the regulatory environment in the US has scared off many traditional banks from engaging with the crypto industry which resulted in a very small number of options for crypto related businesses. Because larger banks have been structurally discouraged from engaging with crypto from regulators, we naturally end up with a concentration of deposits in a small number of boutique banks. Cutting the banking system off from the crypto industry, as some agencies have argued we should do, increases the risk for US consumers, it doesn’t reduce it. Silvergate was the first major US bank to provide regulated, ubiquitous onramps for USD into crypto and its closing is a real loss for the crypto industry and the US economy at large.

The second problem of holding bonds that are underwater isn’t a crypto specific issue. The day after Silvergate announced it would liquidate, Silicon Valley Bank experienced its own bank run. SVB is 20 times larger than Silvergate but it was forced to realize an $1.8 billion loss from selling bonds which created concern over the bank’s financials which in turn led to many customers withdrawing their funds. As a result, Silicon Valley Bank was forced to shut down in what is one of the largest bank failures in US history. On Sunday, the FDIC announced it would backstop all deposits so no SVB customers would lose any money (for what it’s worth, Silvergate was already making all customers whole without the need for the FDIC to step in). Silicon Valley Bank succumbed to the same pressures as Silvergate, not because of its exposure to crypto, but rather its concentrated customer base of venture capital funded startups.

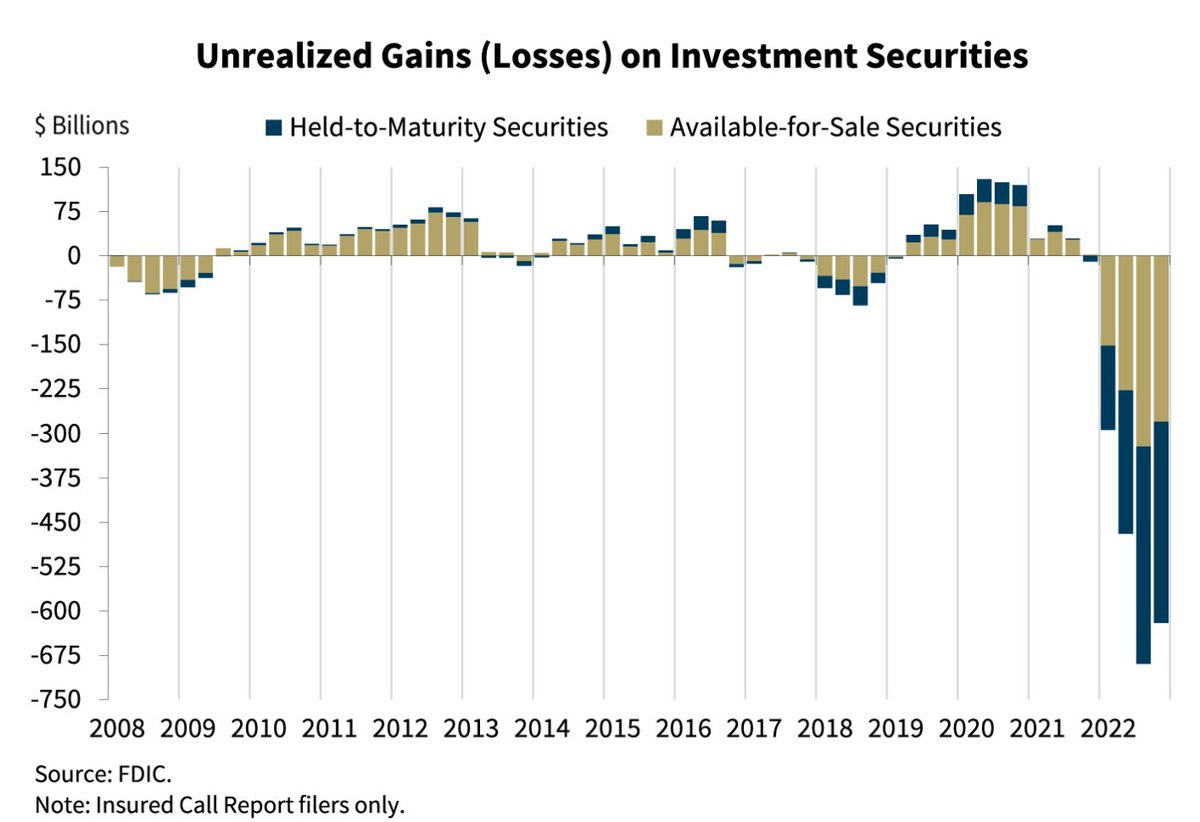

To be fair, the situation with Silvergate and Silicon Valley Bank is not exclusive to them. The problem throughout the banking system comes from the fact that a large portion of banks’ holdings of bonds and T-bills purchased during an environment of near-zero interest rates have traded down in value because the Fed has been increasing interest rates aggressively over the last 12 months. As a result, the banks are technically underwater on their investments. FDIC’s recent quarterly report shows that banks have a few hundred billion in unrealized losses on securities (see chart below). Should consumers start pulling their deposits out, many banks would be forced to sell at a loss just like Silvergate and SVB did. This isn’t just a crypto issue; this is potentially an issue for many US banks.

For months, some politicians and banking agencies like the Treasury Department and FDIC have been vilifying the crypto industry as a threat to the U.S. financial system. While it’s true that both Silvergate and SVB were impacted by market cycles, the bigger issue, as the Wall Street Journal recently wrote, is that most banks hold large amounts of treasuries as legally required collateral, meaning the same structural risk that hit Silvergate and Silicon Valley Bank applies to some degree to a whole lot of banks. Even the FDIC, the same organization that publicly stated that crypto was a risk to the banking system, gave a speech days before Silicon Valley Bank went under saying there is the potential for bank runs due to huge unrealized losses and how “complex & challenging” it was to operate a bank when “interest rates change to the extent they have.” It’s why not just Silvergate and SVB’s stock fell, but banking stocks across the across the board have tanked. The truth is crypto is nowhere near the biggest risk to the financial or banking system.

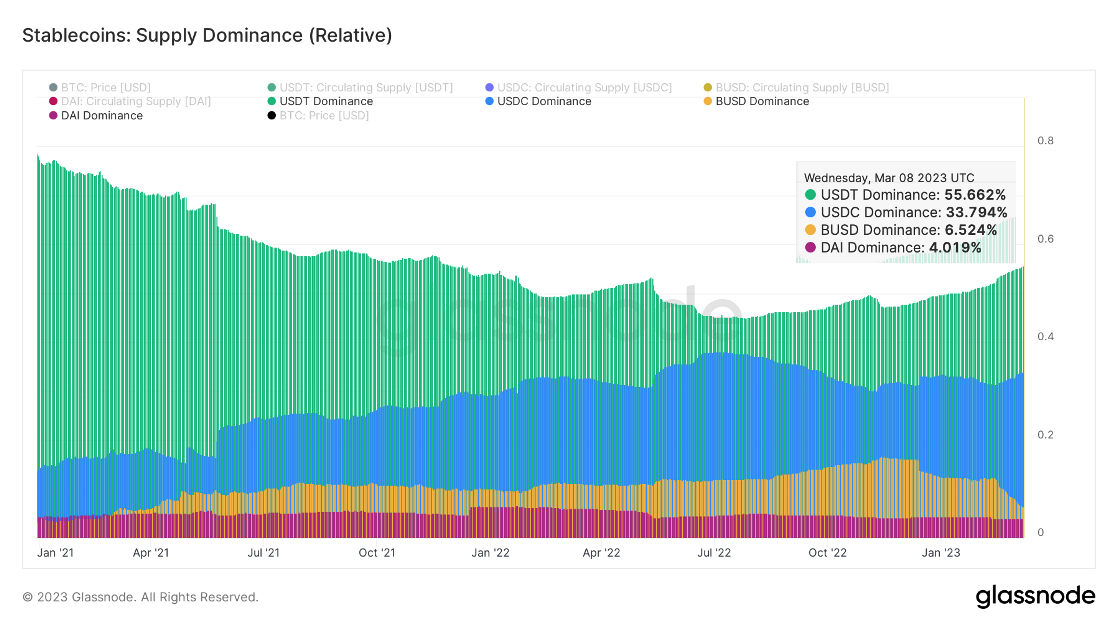

The critical question for the crypto industry moving forward becomes, who will replace the banking business that Silvergate occupied? The shuttering of both the bank and the SEN network removes the largest gateway investors and companies have historically used to move fiat capital in and out of the crypto ecosystem. The answer appears to once again be Tether.

With less access to crypto banking, it’s rational that companies and traders would turn to stablecoins instead. Rather than deposit your dollars with an exchange (who may now have a harder time converting fiat to crypto and vice versa), users can elect to deposit them with a stablecoin issuer, receive stablecoins, and then transfer those to an exchange. The problem is stablecoin issuers also need to be banked so US based solutions such as Circle (issuers of USDC) have less options and more uncertainty in light of the current environment. Rather than deal with the regulatory uncertainty in the US, investors are turning offshore to Tether (USDT).

Since the start of the year, of the four largest stablecoins, only Tether has increased its market share. According to data from Glassnode, BUSD’s market share is down roughly 10%, USDC and DAI have remained roughly unchanged while Tether’s market share has risen to fill the gap. Crypto data company Kaiko put out a research piece showing that the regulatory heat in the U.S. has sharply increased the dominance of USDT in bitcoin trading.

As we mentioned in our last newsletter, USDT is a stablecoin managed by iFinex which is a Hong Kong based company that also owns the crypto exchange Bitfinex. Without getting into details, let’s just say Tether and Bitfinex have a checkered history and are not necessarily known for their transparency regarding the collateralization of USDT. Between the SEC’s enforcement action on Paxos, regulators public comments regarding Silvergate, and the FDIC forcefully shutting down Signature Bank over the weekend, the US continues to incentivize people and businesses to move their money to offshore entities that are much more opaque, far less regulated and often times have less than a stellar track record.

Another potential beneficiary is Europe. The EU has been taking a proactive stance on adopting reasonable regulations regarding crypto as of late. The Markets in Crypto-Assets Act (MiCA), while not perfect, provides clarity for both crypto companies and banking institutions in the EU. Silvergate’s wind down could lead to firms looking overseas given the greater clarity. As Kaiko research noted, “volumes spiked for the BTC-EUR pair as the Silvergate troubles ensued. The BTC-Euro pair hit its highest level of market share vs. the Dollar ever last week, nearly tripling in market share in the space of a few weeks.”

I’ve said it before and I’ll say it again, no matter what the regulatory environment looks like in the US, the crypto industry as a whole will be fine. Stablecoins will still be used, people will still store value in bitcoin, and users will transact in Defi. There is nothing politicians or regulators can do to stop it. It’s a matter of where that activity occurs, not if. The recent string of unfriendly actions and a general lack of support from financial regulators have made it extremely difficult for US based banks to serve crypto related businesses. The only thing the current regulatory environment is accomplishing is hurting US businesses and consumers and putting the US behind the rest of the world.

Proof of Reserves

One of the benefits of crypto is that the blockchain is an immutable ledger of historical transactions that is publicly accessible. This means that anyone, at any time, can prove what assets they hold and how much. We can also verify what assets are held by anyone else so long as we know their public address. Thus, if two parties want to transact with each other, they can each verify the other has the requisite amount of assets to complete the transaction without having to know anything else about their counterparty or use a middleman. This is the core concept behind the meme “Don’t Trust, Verify.”

That’s all well and good if I already know who I want to transact with. However, there are many instances where its far more efficient to have a marketplace connecting millions of people. This is why DeFi, which allows users to maintain self-custody of their assets at all times, has so much potential. Because everything happens on-chain, there is extreme transparency into these services in near real time. It’s because of this open nature that none of the stalwart DeFi protocols went down, none created debt greater than their assets, and none defaulted on their users in 2022. Despite the market chaos caused by fraudulent off-chain activities, DeFi showcased the benefits of decentralization last year.

But not everyone is comfortable using decentralized services yet given the technical complexity that is often involved. In addition, many larger institutions have compliance standards that require them to use regulated third party custody services. As much as I believe in DeFi, I also recognize that centralized custodians, lenders, and exchanges have existed from the beginning of the crypto industry and will continue to be a useful and necessary part of the crypto ecosystem for years to come.

For centralized entities, the way they prove their solvency is by third party audits. Audits are extremely valuable, but they do have some disadvantages. For one, they are expensive. Second, audits are typically only done once per year and financials are released on a quarterly basis for public companies and potentially not at all for private companies. Third, audits still require users to trust that the auditor did their job thoroughly. Even if there isn’t any malicious intent, auditors are still human and make mistakes. Finally, this all assumes you are using a US regulated entity. Regulatory requirements vary from jurisdiction to jurisdiction meaning the quality of audits is not standard throughout the industry.

The ideal scenario would be to extend this principle of “don’t trust, verify” from the decentralized world into centralized services to take advantage of the transparency and benefits of blockchain without sacrificing the convenience of centralized services. Imagine if there was a process that allowed a custodial based service to prove, beyond a shadow of a doubt, that they are fully solvent on a daily basis. Fortunately, that’s possible and it’s called Proof of Reserves.

Proof of Reserves (PoR) is a process used by an organization to cryptographically demonstrate that it possesses an adequate reserve of assets to meet all customer liabilities. Thus, if a user wants to withdraw their assets, they know they will actually get them back. In the wake of the fraud committed by FTX, Celsius, and others, providing this level of transparency goes a long way to instilling confidence that a user’s assets are being safely held on her behalf.

The beauty of Proof of Reserves is that this is a truly novel feature of cryptoassets. Remember the first paragraph in which discussed how we can prove ownership of a digital asset to anyone at any time in a peer-to-peer manner? Well, you can’t do that with any other piece of financial or personal information without relying on a third party. Proof of Reserves is only possible with cryptoassets and allows for custodial services to transparently prove to customers that they hold full reserves and even allow customers or third parties to verify for themselves. And the best part, Proof of Reserves could be standardized over time so that PoR looks very similar across any jurisdiction. Thus, exchanges and other crypto custody-based services can be made more accountable than traditional financial services.

It’s possible that had Proof of Reserves been more widely implemented throughout the industry it could have prevented FTX in the first place, or at least significantly reduced the damage it caused. Proof of Reserves doesn’t stop a centralized exchange from illegally rehypothecating customer funds but the moment an exchange began operating on a fractional reserve basis, they would fail the PoR attestation. So PoR makes it virtually impossible to behave badly for any meaningful period of time. Had every exchange been issuing regular PoR attestations the last couple of years, one of two things would have happened in the case of FTX. The mismatch of assets and liabilities on FTX would have been much easier to discover much earlier on or FTX would have been unwilling to produce a PoR thus alerting the market much sooner.

The good news is that following the FTX collapse, more exchanges are beginning to implement Proof of Reserves today. Longtime PoR advocate Nic Carter surveyed the crypto landscape and found that eleven major exchanges have done at least one PoR attestation since November of last year covering $33 billion worth of assets. Five of those exchanges are doing PoR on a monthly basis or more frequently, including two producing attestations on a daily or bi-weekly basis.

Even more exciting is that we are still in the very early stages of unlocking what Proof of Reserves can do. According to Nic Carter, “I could see interlocking or recursive Proofs of Reserve allowing an ecology of custodians, exchanges, prime brokers, trading firms, and lenders to transact with each other with confidence. These proofs could allow counterparties to demonstrate the existence and nature of assets on their balance sheet (or facts about the assets, without revealing sensitive info). Imagine lenders able to demonstrate the solvency of their portfolio by pulling through balance sheet data provided by their borrowers. Borrowers could also demonstrate the exclusivity of pledged collateral to their lenders (eliminating Archegos or Three Arrows type problems). The design space is enormously large and has barely been explored. Exchange solvency is just the most pressing need, so that’s where this tech is being applied first.”

Unfortunately, PoR is often misunderstood by both proponents and critics. One of the biggest misconceptions is that PoR only covers assets and not liabilities. This comes from the fact that some exchanges did provide asset attestations without the corresponding liabilities following the collapse of FTX simply to ease short term fears. However, the intent of PoR has always been to provide transparency on both sides of the ledger by including ownership of assets as well as demonstrating outstanding liabilities owed to clients. We know this is possible because crypto exchanges Bitmex and Derebit do Proof of Reserves that include the entire liability set in addition to the assets.

A second objection that is often made has to do with privacy concerns in which PoR could potentially reveal private financial information such as account balances and how these balances change over time. However, modern methods for conducting PoR (such as those implemented by Bitmex), user information is anonymized, and account balances are split into multiple parts thus the distribution of account balances cannot be triangulated. The aggregate assets and liabilities are thus able to be reported without revealing specific user financial data. Furthermore, zero-knowledge proof tools are beginning to be developed which will further enhance an exchange’s ability to keep user data private. When combined, these innovations allow users to have a higher degree of confidence over the solvency of the exchange without sacrificing privacy.

And to be clear, no one is calling for Proof of Reserves to replace a traditional audit, but PoR is a highly complementary solution. A financial audit covers much more than just the solvency of an organization, it includes financial, operational and governance aspects of the business which Proof of Reserves does not address. However, audits are infrequent (typically once per year), take a long time to complete (typically months) and are expensive. In comparison, PoR can be performed as often as needed including daily, takes a matter of minutes not months, and is relatively cheap. Proof of Reserves is a tool that gives users and regulators confidence over the custody and solvency of a platform and should be incorporated with traditional measures such as annual audit.

Though there is no industry standard for a Proof of Reserve attestation yet, the good news is regulations are being put forth that should make Proof of Reserves more ubiquitous and standardized. The Texas legislature recently introduced a bill asking for segregated custody at exchanges alongside quarterly PoR attestations and Wyoming also included PoR in its 2021 Digital Asset Custody Framework. More recently, Senator Thom Tillis said that he is drafting legislation to require digital asset exchanges and custodians operating in the U.S. to provide an independently verified proof-of-reserves for their assets.

One inherent advantage digital assets have over legacy financial assets is the transparency and auditability they provide. We should be doing more to take advantage of these native characteristics to minimize bad actors and promote more trust in the industry.

In Other News

Asset tokenization is shaping up to be crypto’s theme of the year.

Crypto’s correlation with U.S. equities and macro events is weakening, according to Bernstein analysts.

Ukraine has collected roughly $70M in crypto donations since the beginning of the conflict with Russia.

Robinhood was issued a subpoena by the SEC in December regarding the company’s crypto listings and custody of assets.

Crypto exchange Coinbase announced that it would suspend trading of BUSD as of March 13.

Block has integrated its mobile payment processor Cash App into crypto tax and accounting software TaxBit to allow bitcoin holders to calculate and report their taxes.

Coinbase launches grassroots campaign to influence US lawmakers and regulators.

Offshoring crypto hurts the financial system and America’s geopolitical standing.

Coinbase acquires One River Digital Asset Management as it aims to move into the institutional asset management business.

Ethereum developers confirm ETH staking withdrawals will be pushed to April.

Amazon will reportedly launch its NFT marketplace in April with 15 NFT collections on launch day.

FTX has filed suit against Grayscale and DCG in order to seek injunctive relief to ”unlock” some $9 billion of value for all Grayscale shareholders, including around $250 million that now belongs to FTX creditors.

House Majority Whip Tom Emmer and the Chairman of the House Financial Services Committee, Patrick McHenry plan to reintroduce the Keep Innovation in America Act which is a bipartisan solution to change the reporting requirements for certain taxpayers involved in crypto transactions.

Missouri and Mississippi move closer to legally protecting crypto mining.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS