By Brett Munster

Wyoming & PayPal will issue their own stablecoins

Wyoming and PayPal are putting themselves in the middle of a larger debate over the federal government’s role in the U.S. financial system. To understand why, we first must have a baseline understanding of the current regulatory environment surrounding stablecoins.

There are two pieces of crypto legislation that, if passed, would go a long way in closing the regulatory gaps, provide clarity to the market, and put the U.S. on par with the rest of the world. The first is a market structure bill. Currently, there are two market structure bills making their way through Congress. One is the Financial Innovation and Technology for the 21st Century Act (aka Fit21) originating from the House and the second is the Lummis-Gillibrand bill coming from the Senate. We have covered both these bills in depth in previous newsletters.

The second piece of regulation that would be extremely beneficial to the U.S. market would be a stablecoin bill. Back in April we laid out the economic and national security reasons as to why the U.S. should embrace stablecoins. However, recent actions from regulators have benefited offshore issuers (such as Tether who operates USDT) at the expense of U.S. based companies (namely Circle who operates USDC). Thankfully, Congress has finally decided to act and in June, proposed the Clarity for Payment Stablecoins Act which would establish the first U.S. regulatory framework for stablecoins.

At the end of July, the bill passed through the House Financial Services Committee with bi-partisan support and now advances to the House floor. The good news is there is a lot of agreement from both sides of the aisle on the basic structure of the bill. However, there is one particular sticking point that could prevent this bill from becoming law. The bill, as currently drafted, would have the U.S. Federal Reserve write the requirements for issuing stablecoins but squarely puts most of the power in the hands of the states allowing them to license stablecoin issuers. This is a similar structure to our current banking system where there are both federal and state-chartered banks.

However, opponents to the bill want stablecoin licenses to be issued only to banks that are federally chartered. As a result, this approach would most likely benefit large banks who already have a federal charter at the expense of smaller banks or startups because a federal license is very difficult and expensive to acquire. If this approach were to win out, it would likely severely limit who could and couldn’t become a stablecoin issuer thereby stifling competition.

Which makes what Wyoming and PayPal are doing so interesting.

Let’s start with the state of Wyoming. Wyoming has been way ahead of the curve with regards to crypto regulation having passed over 30 pieces of crypto specific legislation. The most recent piece of legislation that was passed is called The Wyoming Stable Token Act and makes it legal for the state to issue a dollar backed stablecoin through a trust account. The state of Wyoming will take dollar deposits, issue stablecoins, and invest those deposits exclusively in 3-month treasury bills. The legislation requires constant proof of reserves reports to ensure 102% backing of all stablecoins issued. This way, users of the Wyoming stablecoin will have confidence that they will always be able to redeem their tokens for dollars.

According to Wyoming state senator Chris Rothfuss one reason Wyoming is looking to pass this bill is because they want to enable businesses to accept cryptoassets as payments as well as allow citizens to pay taxes in crypto. For those businesses who want to convert some or all of the payment into a more stable currency, stablecoins is an ideal solution. Rather than having to convert to dollars, it would be simpler, faster and cheaper to convert to a stablecoin that is still in the crypto ecosystem but not subject to the volatility of other cryptoassets.

But there are bigger implications to this bill beyond just collecting taxes. If Wyoming can successfully launch a state run stablecoin on a public blockchain (which they plan on launching by the end of the year) it will be a huge narrative violation for those arguing that the Fed needs complete oversight and control of granting licenses. The dual banking system we have in the U.S. is supposed to recognize the sovereignty of states to operate and participate in the national financial system. The mission of the federal reserve is to facilitate that involvement, not control the states. Thus, the fight over who can issue stablecoins is not just about stablecoins per se, but potentially a constitutional issue surrounding the role of the federal government in our financial system. It is fascinating to see state’s rights becoming a focal point in the cryptoasset industry and Wyoming is putting itself right in the middle of that debate.

Then there is PayPal. On August 7th, PayPal announced it is launching its own stablecoin pegged to the dollar called PayPal USD or PYUSD for short (why they didn’t go with PayUSD when it was sitting right there for the taking, I’ll never know). PYUSD is built on Ethereum and will be fully backed by dollar deposits, short-term U.S. Treasuries and similar cash equivalents. This will mark the first time a major U.S. financial company is issuing their own stablecoin. It also means that PayPal, with its 435 million accounts, is launching a stablecoin without a federal charter. Similar to the state of Wyoming, PayPal is challenging the notion that only federally charted banks should be able to launch a stablecoin.

Why would PayPal want to launch a stablecoin in the first place? Three reasons come to mind. First, the release of FedNow in July could signal the commoditization of money transfers. It’s possible that in response, PayPal sees stablecoins as a way to make payments and cross-border remittances within PayPal more competitive. PYUSD will also be able to be used to buy crypto on PayPal thereby enabling the company to diversify into higher-margin business lines. Don’t be surprised if more service providers start adopting stablecoins (either existing stablecoins or launching their own) as their services become commoditized.

Second, cost savings. Right now, every time PayPal facilitates a transaction using Visa or Mastercard, the company is subject to processing fees of 2-3%. Conducting those same transactions using a stablecoin could be done practically for free thus circumventing those credit card fees. PayPal could let those savings fall straight to their bottom line or they could use those savings to offer incentives to their customers and large network of merchants in order to drive adoption of PYUSD.

Third, stablecoins could be a new revenue stream for the company. The beauty of running a stablecoin business right now is that you take in dollars and issue stablecoins 1-to-1. The holder of those dollars can then take those deposits, buy short term treasuries (which currently yield roughly 5%) without having to pay out any of that interest to users. It’s an extremely high margin, lucrative business (so long as the reserves are managed appropriately) and the more PYUSD there is in existence, the more yield PayPal makes on all those deposits they are holding.

In fact, it’s the same for the state of Wyoming. Why not issue a Wyoming stablecoin that local businesses can use to bypass the credit card transaction fee and at the same time, earn the state government a 5% yield? It’s an easy way to increase state revenue without increasing taxes! The revenue derived from Wyoming’s stablecoin will be deposited to the Wyoming Permanent Fund, a sovereign wealth fund that is used to support K-12 education in the state.

And if you are now wondering, how much money could PayPal or Wyoming really make? Well, let’s look at Tether, the largest stablecoin on the market today at around $80 billion in circulation. Tether’s most recent attestation report showed that the company made $1 billion in revenue last quarter alone. Not last year, last quarter. All with about only 60 employees making Tether one of the most efficient profit-per-capita companies not just in crypto, but in any industry.

Tether’s success in popularizing U.S. dollar-backed stablecoins is somewhat ironic given it’s not a U.S. based company. One reason why Tether has become the industry leader is that recent regulatory enforcement actions have made it difficult for U.S. based companies to operate. The leading American stablecoin issuer Circle (who issues USDC) is currently losing market share to Tether because the rest of the world sees the U.S. regulatory regime as too risky. In fact, since the SEC started ramping up their enforcement actions, the percentage of dollar backed stablecoins issued by offshore companies has increased from roughly 50% to 75%. Nearly three quarters of all dollar backed stablecoins are issued by organizations outside the U.S. The U.S. could be and should be the leader in this emerging market, but we aren’t because regulators and politicians have been holding U.S. companies back. Which brings us full circle (no pun intended) back to the Stablecoin Bill in the House which if passed, could alleviate many of the current roadblocks put up by the SEC and OCC.

Given the current lack of regulatory clarity in the U.S. surrounding stablecoins and the SEC’s enforcement actions in 2023, it’s easy to understand why this Stablecoin Bill could be so impactful. The longer it takes for this bill to pass, the more overseas competitors continue to gain ground over U.S. companies. And it’s not just economic implications, there are geopolitical considerations as well. Fun fact, Tether now owns $72.5 billion worth of U.S. Treasuries. If Tether was a country, it would be the 24th largest foreign holder of U.S. treasury securities in the world, more than Australia, the UAE, and Mexico.

The recent actions by Wyoming and PayPal, neither of which are federally chartered, are important developments because the prospect of hundreds of millions of users soon having easy access to stablecoin transactions could be the accelerant lawmakers in D.C. need to reach a compromise on a regulatory framework for stablecoins. Hopefully the bill gets passed relatively soon and remains as currently drafted, with federal oversight but states retaining the right to issue licenses. That way, we continue to allow for innovation rather than just handing this market over to the big banks. Regardless of what happens, it’s going to be very interesting to watch how this space develops over the next 12 months.

Bitcoin drops to the bottom of its trading range

Since March of this year, bitcoin has been pretty much flat, trading between $25,000 and $31,000 with historically low volatility. More recently, bitcoin had been hovering on the higher end of that range leading many to think we were on the cusp of breaking out. However, on August 17, bitcoin unexpectedly fell roughly 12% back down to $25,000 representing the largest single day sell-off thus far in 2023.

That fall coincided with a Wall Street Journal piece about SpaceX’s finances. The article was mostly about the company’s revenues and research costs but also included a comment that SpaceX had “written down the value of bitcoin it owns by a total of $373 million last year and has sold the cryptocurrency.” This led many to speculate that SpaceX’s sale of its bitcoin was the catalyst for bitcoin’s drop. However, it’s very unlikely SpaceX was the cause of the price drop given we do not know when SpaceX sold its bitcoin or over what period. SpaceX is a private company meaning the sale could have happened anytime over the past year. It’s also very likely SpaceX sold its position over a period of time and in multiple transactions. Even if the company did sell all at once, the value of their holdings is about 0.07% of the total value of bitcoin’s market cap so it’s unlikely that SpaceX alone could have moved the market that dramatically.

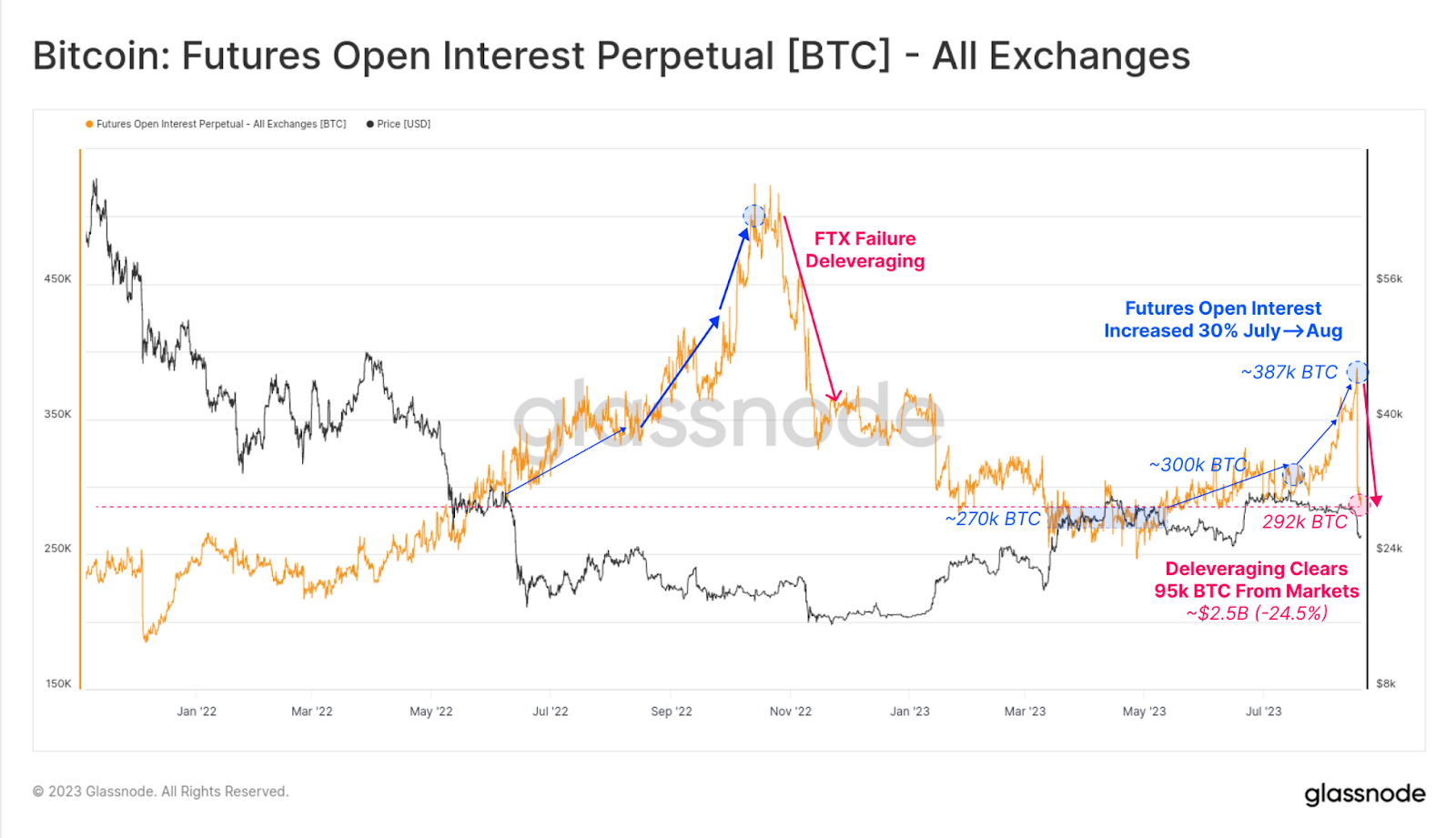

So, what caused bitcoin’s price to plunge? A leverage flush out in the derivatives market. Derivative markets are used to make bets about the future price of bitcoin and are especially popular with traders and hedge funds because it’s easy to add leverage. The dollar amount of futures open interest had been steadily rising since March most likely because many were expecting the volatility to eventually pick back up. The longer bitcoin traded in a tight range, the more likely it is we would see a breakout in the future (at least that’s the theory). The data suggests most of the positions were longs, meaning most traders were anticipating bitcoin’s price to rise in the near future (perhaps in anticipation of a ruling in the Grayscale vs SEC case).

However, bitcoin’s price started to drop. It’s unclear exactly why but there are a number of theories. For one, the Federal Reserve’s July meeting hinted at the possibility of another increase in interest rates later this year which typically is bad news for stocks and crypto. There were reports about China Evergrande, China’s second-largest property developer, recently filing for bankruptcy leading many to speculate if this had a domino effect on the price of bitcoin in the Chinese markets. There was also the SpaceX article which many may have misinterpreted.

Regardless of why bitcoin’s price dipped, once it did, it triggered margin calls on some of those long derivative positions. This forced some market participants to sell which further lowered the price and thus triggered even more margin calls. In fact, as prices kept falling, it triggered over $1 billion worth of liquidations in the open interest market in just a couple hours. For context, that was more liquidations in a single day period than when FTX collapsed.

After events such as August 17, it’s always worth stepping back and taking a look at the bigger picture. With regards to bitcoin’s price, it’s still trading in the same range it has for most of the year, further reinforcing the strong support at $25,000. The dip in price had nothing to do with fundamental growth metrics or adoption rates. In fact, bitcoin recently hit new all-time highs in daily transactions proving the adoption and usage continues to grow. What we saw happen was an unwind of all the leverage that was built up through the last few months, and although painful in the short term, actually puts the market in a healthier position moving forward. Taking all that into account, it’s likely that this is a short-term pull-back in price within a much larger uptrend for the crypto markets.

In Other News

A number of legal briefs have been filed in support of Coinbase putting more pressure on the SEC.

Crypto custodian Prime Trust files for bankruptcy in Delaware.

Europe’s first spot bitcoin ETF lists in Amsterdam.

The FIT Act is the most comprehensive crypto regulation ever voted on by Congress.

Securitize deal to access RIA market latest step of tokenization growth journey.

Coinbase is acquiring a minority stake in Circle as the two solidify their stablecoin partnership amidst growing competition and regulatory developments.

Bitcoin mining startup raises $13 million to turn trash into BTC.

E-commerce giant Shopify has added Solana Pay to its pool of options for payment, allowing millions of merchants to use the platform to accept crypto transactions.

Tokenization could improve bond market efficiency.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS