By Brett Munster

Ethereum is growing faster than most tech companies

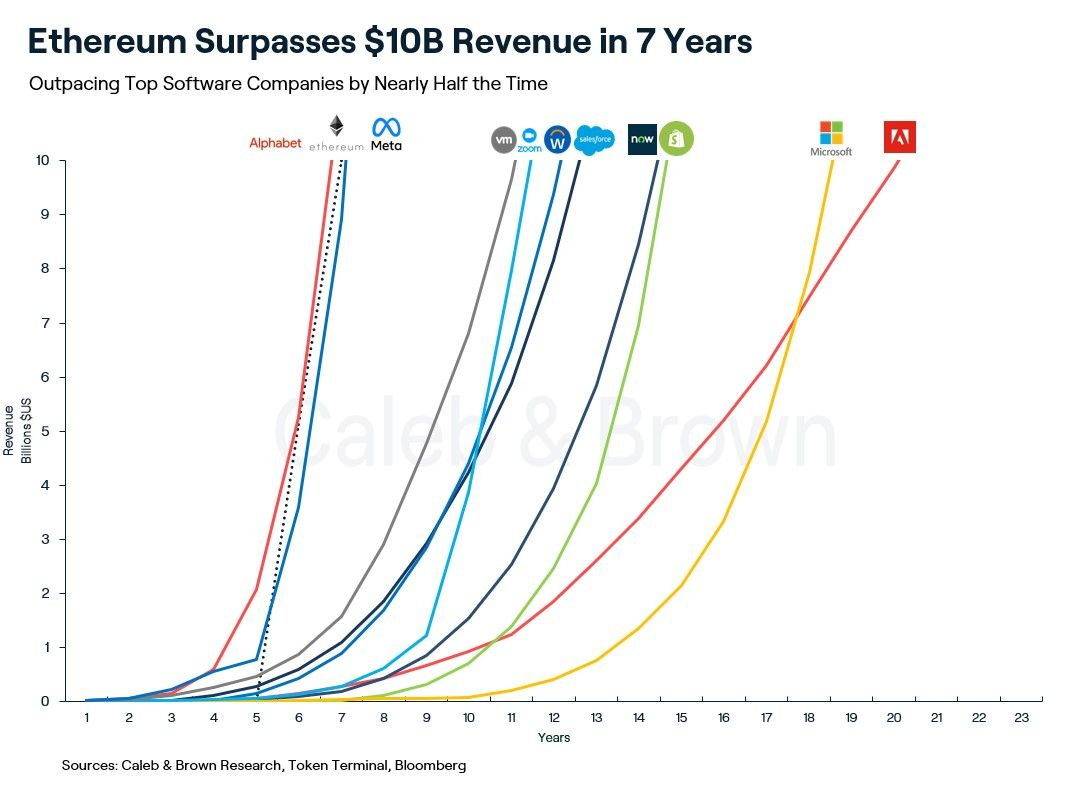

According to a recent report by Caleb & Brown, Ethereum just surpassed $10 billion in revenue over the course of its lifetime. I think that statement will come as a surprise to a lot of people.

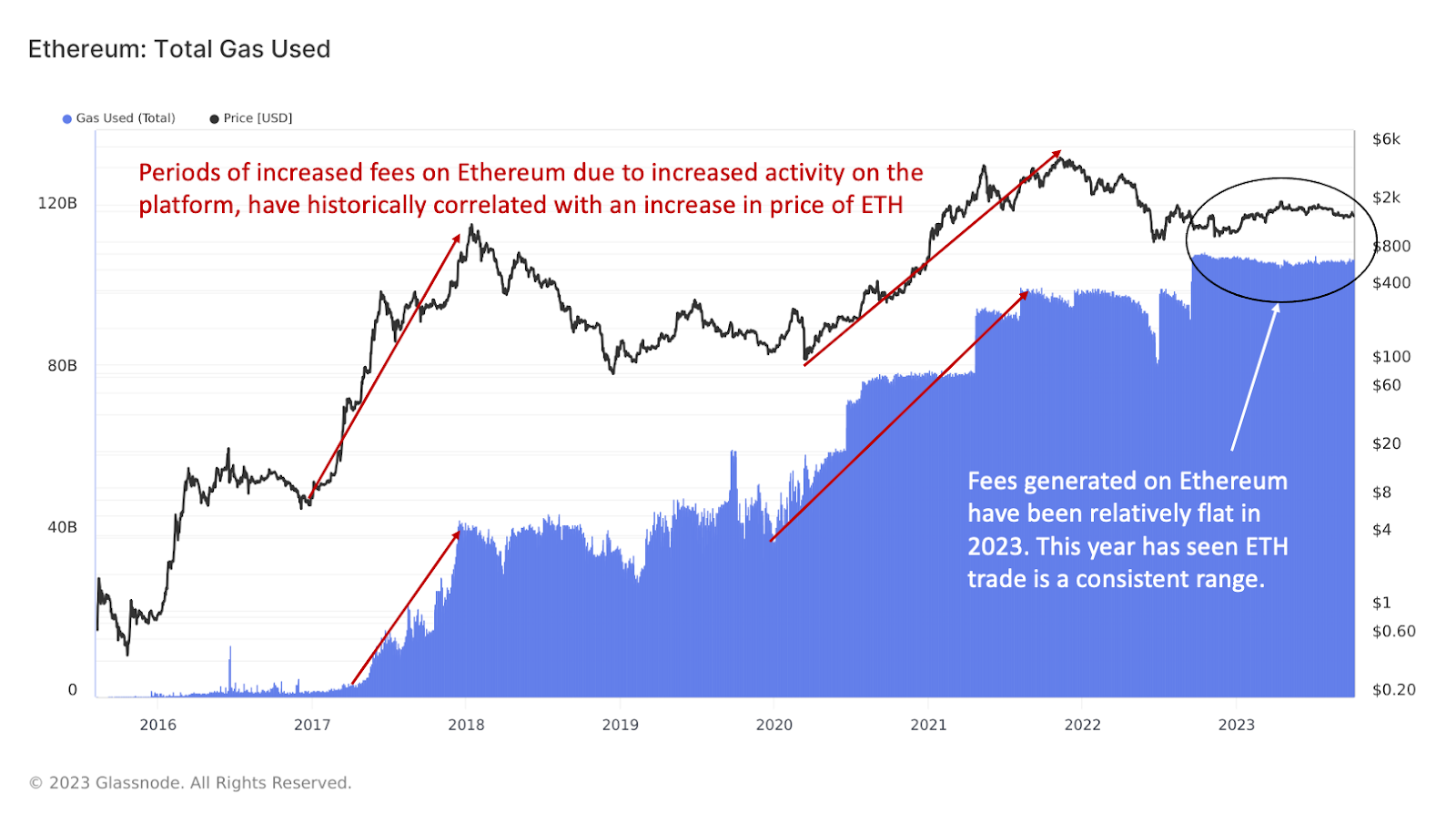

Outside of those who spend the majority of their time following the cryptoasset industry, most people are probably unaware that Ethereum produces revenue because it’s a decentralized network and not a company. But remember, Ethereum is a computing platform that developers use to build applications on top of. It’s a similar concept to Amazon Web Services (AWS) which provides the computing power (aka “the cloud”) that enables you to call an Uber, rent a home on AirBnB, check the scores of your favorite sports team on ESPN, watch a movie on Netflix, listen to music on Spotify, and use most of the apps on your phone. Ethereum serves a very similar function allowing a host of financial and non-financial applications to operate without the need for a middleman. Instead of Jeff Bezos having centralized control over its cloud network, Ethereum is decentralized which has a host of inherent benefits for app developers and end users that a centralized platform doesn’t. And much like your favorite mobile apps pay Amazon a monthly fee for using Amazon’s compute power, applications built on Ethereum pay a fee to the Ethereum network every time their product is used on the network.

So yes, Ethereum does produce revenue. That revenue is a direct result of usage of the platform. The more apps are built on Ethereum and the more people that use those apps, the more fees are generated and the more revenue Ethereum makes. The two biggest differences in using the Ethereum network versus Amazon are that fees are paid in ETH rather than dollars and instead of the revenue going to the coffers of a mega-corporation, it goes to the validators of the network (ie: those who own ETH and stake it to help operate the network). As a result, fees generated on the Ethereum network should be generally related to ETH’s price over the long term much like revenue growth is often related to the price of a stock.

And the craziest part of Ethereum reaching $10 billion in aggregate revenue is that it did so in only 7.5 years. To put that in perspective, that is faster than almost every major tech company. Faster than Apple, Facebook, Salesforce, Shopify, Zoom and many others. It took Microsoft 19 years to reach that milestone. In fact, the only company to get to $10 billion in revenue faster was Google.

Today, Amazon’s market cap is $1.3 trillion. Microsoft’s market cap is $2.3 trillion and Apple’s is $2.7 trillion. Ethereum’s market cap is only $200 billion but it’s growing faster than any of those companies. A recent report from VanEck Research projects Ethereum could potentially increase its annual revenue from $2.6 billion this year to $51 billion by 2030. Plus Ethereum doesn’t have the overhead such as payroll, office buildings, etc.. that a traditional company does which means the network has a much higher gross margin. If Ethereum does continue to grow faster than traditional tech companies and has better economics than those companies, it’s possible that Ethereum could eclipse the market cap of these companies over time.

Over the last two years, we have continued to stress the fact that the adoption and fundamentals of many crypto networks have strengthened even though prices are well below their all-time highs. This is yet another in a long line of reasons to be bullish on the long-term prospects of the crypto industry.

As always, the on-chain data is provided by Glassnode. If you would like to have access to the data yourself, you can sign up here:

FASB updates crypto’s accounting rules

The aggregate amount of cash and cash equivalents sitting on the balance sheet of all S&P 500 companies is currently $2.6 trillion. Why do I bring this up? Because the accounting rules for how crypto is valued on a corporate balance sheet are going to change, making it much more attractive for companies to hold bitcoin and other cryptoassets.

Back in May of last year, we detailed why the accounting rules for bitcoin and cryptoassets make no sense. By accounting standards, bitcoin does not meet the criteria to be considered a currency (mostly because it’s not issued by a government). As a result, it has historically fallen in the “intangible asset” category simply because accountants didn’t know how else to classify it. The problem with that classification is companies that hold bitcoin on their balance sheets are forced to mark down the value of their bitcoin holdings when the price drops but are forbidden from marking up the value when the price rises. This accounting method (or more accurately, the lack of a proper accounting method) leads to a company’s holdings being undervalued when reported, which could hurt its stock price. A lot of companies have shied away from adding bitcoin to their balance sheets not because they don’t see the value in it, but because the accounting rules could hurt how Wall Street values their business.

Currently 38 public companies hold bitcoin on their balance sheets totaling over $50 million. This group, along with other companies also interested in holding BTC on their balance sheets but have yet to do so due to the accounting rules, petitioned the Financial Accounting Services Board (aka FASB) to change the rules so that companies can report both their gains and losses from their crypto holdings in the income statement. To their credit, FASB agreed to evaluate the accounting rules and in September this year, officially amended the rules for cryptoassets with a unanimous vote.

Under the new rules, FASB will require companies to disclose their digital asset holdings at fair market value at the end of each fiscal period. This means that if bitcoin’s price goes up, companies can now recognize that gain in value thereby eliminating one of the largest impediments to corporate adoption of cryptoassets. The new requirements will apply to all cryptoassets including BTC, ETH and stablecoins though it’s worth noting that FASB excluded NFTs from this rule change. The new rules officially go into effect for all companies starting on December 15, 2024. However, earlier adoption of the new rules is also permitted meaning companies can start using fair-value accounting immediately if they want to.

Don’t expect trillions of dollars of corporate money to come flooding into bitcoin and crypto overnight. However, with the accounting rules changing, it makes it much easier for these companies to start dipping their toes into crypto for three reasons. The first has to do with who is holding most of that $2.6 trillion sitting on corporate balance sheets. It turns out the largest holders of that cash are tech companies such as Apple, Alphabet, Microsoft, and other tech giants who issue little to no dividends (ie: they are unlikely to give that cash to shareholders). It’s these same tech companies who are likely to be more comfortable adopting bitcoin as a treasury asset than companies in other industries. We have already seen tech companies such as Tesla, PayPal, and Block (formerly known as Square) add cryptoassets to their balance sheets and that was before the new accounting rules. Don’t be surprised to see an increase in the number of tech companies announcing they own bitcoin and other cryptoassets over the course of the next couple of years.

The second is inflation and monetary debasement. In past issues, we examined the structural issues with the U.S. government budget and barring any drastic legal reforms, why the U.S. government is guaranteed to operate at a loss for the foreseeable future. Even since writing that piece, interest payments for the U.S. government have exploded faster than projected. As of June of this year, the annualized interest rate payment for the U.S. government is higher than the annual defense budget. We as a country now spend more per month on interest payments on our debt than we do on the military. By the U.S. Treasury’s own projections, that wasn’t supposed to happen until 2029 so our interest rate problem is accelerating faster than most have anticipated.

In the not-too-distant future, interest payments will be the largest line item in the U.S. budget and mandatory spending (interest payments + budget items guaranteed by law) alone will exceed total tax revenue. That’s before any spending on the military, education, research, infrastructure, etc. Short of any major overhauls to Social Security, Medicare and Medicaid, the only way for the U.S. government to avoid defaulting will be to print tens of trillions of dollars in the coming years which will lead to further monetary debasement of the dollar. It’s simple, basic math.

And if you are a corporation sitting on a lot of cash and it’s being debased every year, the last thing you want to do is just let your money sit in your bank account and lose value. It makes sense to put some percentage, even if it’s a small percentage, of the total balance in an asset that has the exact opposite characteristics of fiat money.

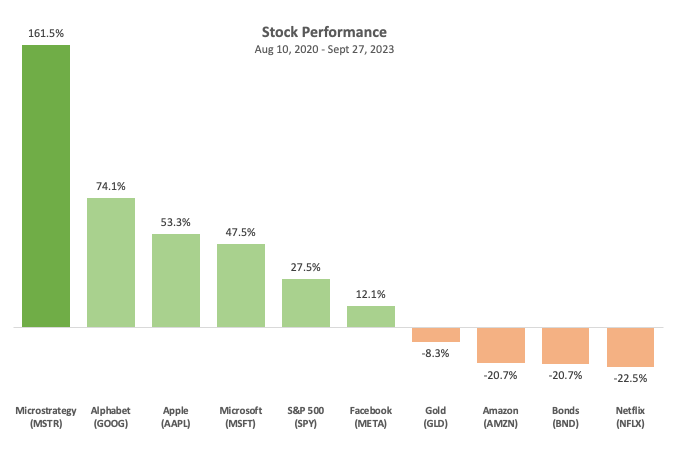

The third reason companies are likely to begin adding cryptoassets to their balance sheets has to do with stock performance. Microstrategy has been by far the leader with regards to public companies holding bitcoin in its corporate treasury. On Aug 10, 2020, Microstrategy adopted bitcoin as its primary treasury reserve asset, purchasing 21,454 BTC for $250m at roughly $11,653 per coin. Since then, the company has continued to repeatedly purchase more bitcoin and as of 9/24/23, holds 158,245 BTC at an average price of $29,582.

Since that initial purchase just over three years ago, Microstrategy’s stock has outperformed every benchmark and just about every major tech stock.

Put yourself in the shoes of a CEO or CFO of a Fortune 500 company who is currently sitting on a significant amount of cash (I know, I wish we all had such problems). You realize that it’s very likely that stockpile is going to lose significant value over time if it just sits there, so you need to do something with it. You could pay some out as a dividend, do a stock buyback, or buy short term treasuries and earn a modest yield. All of those would be sensible choices. But you also see what buying bitcoin has done for the stock performance of Microstrategy (not to mention the free PR the company continuously receives), and that was during a period in which it was disadvantageous from an accounting perspective to hold bitcoin on your balance sheet. Now, the accounting impediment is gone and it’s possible to recognize the gain in value should bitcoin’s price increase. Taking a small percentage of your corporate treasury and buying bitcoin now seems like a far more attractive option.

To reiterate, we don’t expect billions of corporate dollars to come flooding in overnight. However, the current market dynamics and this new rule change are creating the conditions to attract a new customer base that historically hasn’t been active in buying bitcoin. And that new customer base has a lot of dry powder it could deploy over the next several years. In the past, I have predicted that over the next decade or so, it’s not only going to become common for companies to hold bitcoin on their balance sheets, but it will eventually be considered best practice to do so. Given recent developments, the odds of that prediction becoming a reality have only increased.

Gensler gets grilled in senate hearing

On Wednesday September 27th, the House Financial Services Committee held a hearing entitled Oversight of the Securities Exchange Commission in which members of both parties had an opportunity to ask Gary Gensler about his actions during his tenure as SEC chair. It was kind of like a performance review at work, except instead of talking with HR, Gensler was testifying in front of Congress while being live streamed on the internet.

It’s worth noting that the hearing was not exclusively focused on crypto. For five hours Gensler did his best to dodge questions and provide vague responses as he was grilled by both Republicans and Democrats on a wide range of topics. It turns out, the current SEC Chair has seemingly aggravated a wide range of people from multiple industries. In fact, some of the criticism from other industries is beginning to sound a lot like the accusations made by those in the crypto industry, namely that Gensler is overstepping this authority at the expense of consumers.

However, this is a crypto newsletter, so we are going to cover the notable crypto related highlights from the hearing.

The Chairman of the House Financial Services Committee Patrick McHenry opened the hearing by reiterating the same concerns raised by Congress regarding the SEC several months ago. Those concerns include “reckless approach to rule making, lack of capital formation agenda, crusade against the digital asset ecosystem and unresponsiveness to Congress.” According to McHenry, Gary Gensler has done nothing to alleviate those bi-partisan concerns. More alarming, seven months ago the Committee requested documents be turned over by the SEC regarding the multiple meetings Gary Gensler had with Sam Bankman-Fried (former CEO of FTX) but the SEC has still yet to provide any of those documents to Congress. Just imagine ignoring a major request from your boss for seven months. McHenry went on to threaten Gensler with a Congressional subpoena if he doesn’t comply.

Other notable moments included Tom Emmer articulating why Gensler’s policies have disproportionately benefitted large, established financial institutions at the expense of consumers and start-ups. Warren Davidson highlighted how the courts have shown the SEC’s actions to be legally flawed and reiterated his desire to pass the SEC Stabilization Act which would fire Gensler and restructure the SEC to be more bi-partisan. Mike Flood questioned Gensler about the agency’s guidance that heavily dissuades banks from custodying cryptoassets despite it being out of the SEC’s jurisdiction to do so and without conferring with the proper agencies. Wiley Nickel questioned Gensler about why a bitcoin ETF has yet to be approved and Congressman Andy Barr called Gary Gensler the “Tanya Harding of securities regulation” due to his kneecapping of both the crypto and capital markets. You don’t see too many 1994 Winter Olympic references in Congressional meetings but hey, if the skate fits…

But the most insightful moment came from democrat Ritchie Torres’s exchange with Gary Gensler. Congressman Torres started by asking a few basic questions regarding the legal definition of an investment contract. This definition is what determines what is and isn’t a security and if an asset is not a security, it’s not under the SEC’s jurisdiction.

Torres’s line of questioning illustrated how the term “investment contract” has been interpreted too broadly by the SEC which has enabled the agency to classify anything it wants as a security. Gensler refused to provide a clear answer to Torres’s questions regarding whether an investment contract requires some form of contract to be considered a security. Such a requirement would likely protect many cryptoassets and digital collectibles from being classified as investment contracts. Gensler argued that existing law grants the agency broad authority even though he could not cite a single court case in which an investment contract lacked an actual contract.

It is pretty telling that Gensler purposefully avoided answering Torres’s questions because if he had answered the questions directly, the answers very likely would have contradicted his public statements and actions by the SEC over the last couple of years.

Frustrated by Gensler’s unwillingness to provide a direct answer, Torres then changed his approach and asked Gary two very simple questions:

Torres: “If I purchase a Pokemon card, is that a security transaction?”

Gensler: “That is not a security.”

Torres: “If I purchase a tokenized Pokemon card via a blockchain, is that a security transaction?

Gensler: “I’d have to know more.”

No Gary, you don’t have to know more. There is no difference from a securities perspective between a physical baseball card or a baseball card that exists on a blockchain. And therein lies the core legal fallacy behind many of the SEC’s actions with regards to the crypto industry. The SEC’s stance is binary. As Gensler has publicly said numerous times, every digital asset, other than bitcoin, is a security. Are there digital assets that should be classified as securities? Absolutely. Are there digital assets that should be classified as something else? Absolutely. No one in the crypto ecosystem is arguing that no cryptoassets are securities but it’s the SEC that is arguing that every cryptoasset is. And the courts have time and again ruled that the SEC is wrong. In fact, the SEC just lost again in court last week when its appeal of the Ripple ruling was rejected.

While the SEC is pursuing legally dubious lawsuits against Coinbase and other crypto companies, Congress is increasingly adopting a more pro-crypto stance. Politicians from both the Democratic and Republican camps are pushing back against Gensler. Now we just need Congress to do more than hold hearings, it’s time for them to pass the multiple proposed pieces of legislation they have in front of them.

In Other News

The Federal Reserve Board published a paper on tokenization stating that the potential benefits include lower barriers to entry for otherwise inaccessible investments, more competitive and liquid markets, and better price discovery.

Bitcoin gains legal recognition as a digital currency in Shanghai, China.

Four members of the House Financial Services Committee, two from each party, push Gensler to approve spot bitcoin ETF “Immediately.”

BlockFi gets court approval for restructure plan.

The surprising, simple answer to Africa’s rural energy problems – Bitcoin mining.

HSBC, one of the largest banks in the world, has recently started allowing its customers to pay their mortgage bills and loans with cryptocurrencies.

Fidelity’s Ethereum investment thesis.

UBS Asset Management initiated the first of several “live pilots” exploring various tokenized money market funds on the Ethereum blockchain.

Congress can’t let Gary Gensler regulate digital assets out of the United States.

The SEC loses another crypto court case, this time their appeal of the Ripple ruling was rejected.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS