By Brett Munster

Oh, the irony…

Last week, the U.S. Marshals Service (USMS), a division of the Department of Justice responsible for asset forfeiture, selected Coinbase as its partner to safeguard and trade the digital assets owned by the U.S. government. After conducting a thorough due diligence process that evaluated several companies, the USMS determined that Coinbase was best equipped due to its proven track record of providing institutional-grade crypto services at scale. Ironically, this decision comes at a time when the SEC is actively pursuing a lawsuit against Coinbase.

This means the U.S. government has chosen Coinbase as its custodian and exchange while simultaneously claiming that Coinbase broke the law by offering those very same services. This is yet another example that highlights the confusing regulatory environment in the U.S. regarding cryptoassets.

Welcome to the roller coaster

Back in March, when bitcoin first surged to new all-time highs, we highlighted how that milestone has historically marked an increase in volatility over the following 12-18 months. We noted how bitcoin has experienced double-digit price corrections 10 or more times during each of its last three cycles before ultimately leading to triple digit gains (or more). Last week, history repeated itself once again as bitcoin’s price fell to $53,500 and then recovered. Given we have entered into a new phase in this market cycle just as we predicted, it’s worth examining the dynamics that have caused bitcoin’s price to fall since the Halving, the unfounded fears that triggered last week’s sharp drop, and why these fluctuations are a normal part of the larger crypto market cycle.

The Mt Gox Misconception

Let’s start with last week’s price drop. In 2014, Mt. Gox, then the largest crypto exchange, suffered a notorious hack, losing approximately 850,000 bitcoins valued at around $450 million at the time and subsequently filed for bankruptcy. After a decade-long bankruptcy proceeding, the defunct exchange announced in June that it would start distributing up to 142,000 BTC (worth over $8 billion at today’s prices) to creditors beginning the first week of July 2024.

At approximately 5:30 pm PT on July 4th, Mt. Gox transferred 47,229 BTC (worth approximately $2.7 billion) out of their wallet in preparation for repayment. This on-chain movement immediately caused bitcoin’s price to plummet below $54,000, 25% below its all-time high, not because creditors had received any bitcoin, but because the market anticipated that repayments would lead to a surge in sell pressure. Many believed that early investors, who will receive assets valued significantly higher than their initial investments before 2013, would be inclined to sell part or all of their holdings.

However, as we explained in a Forbes article in June, these fears are vastly overstated. First, the Mt. Gox distributions will be phased over several years, with only about half of the total amount being sent to creditors over the next few months. It will likely take years to fully unwind the Mt. Gox estate and distribute all 142,000 bitcoins. So, the actual sell pressure is at most half of what the market anticipates.

In actuality, the true sell pressure from the Mt. Gox distribution is far less than that. The prevailing market narrative is based on the misconception that these bitcoins are being distributed back to the original retail customers. In reality, a vibrant secondary market for Mt. Gox claims have emerged over the past several years, with institutional investors acquiring a substantial portion of these claims. Consequently, fewer bitcoins will be returned to retail investors than commonly assumed, with more going to sophisticated, long-term investors who are less likely to liquidate immediately.

Additionally, retail investors who still hold claims have had ample opportunities to sell over the past decade, often rejecting attractive offers. Those still holding their Mt. Gox claims are more likely to be long-term believers in bitcoin than the average retail investor. In addition, those that do receive any bitcoin from Mt. Gox face significant capital gains tax liabilities, given that bitcoin’s value has increased 140-fold since the bankruptcy, which may further minimize sell pressure in the market.

Hence, we believe the fears surrounding the Mt. Gox announcement are widely overstated, and the impact from the Mt. Gox distribution will be far less than the prevailing narrative suggests.

Miner capitulation is suppressing bitcoin’s price

After surging past $60,000 and peaking at $73,000 in March, bitcoin had remained range-bound between these price levels until last week. The primary factor preventing bitcoin from breaking out in recent months is the selling pressure from bitcoin miners.

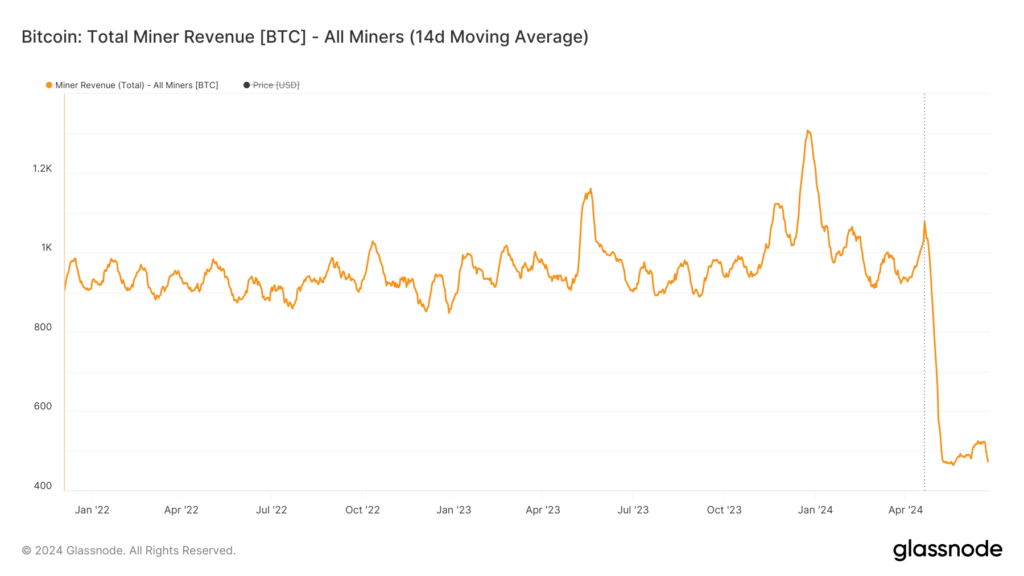

Following the April halving, the block subsidy was cut by 50%. With bitcoin’s price largely stagnant, miners’ revenue has effectively been halved. This sharp decline in total miner revenue (block subsidy + fees) is evident in the on-chain data.

Unfortunately for miners, their operational costs have remained unchanged. While those with access to cheap electricity might manage, miners with higher costs or less operational efficiency are now operating at a loss. These miners have resorted to selling bitcoin to fund their operations, hoping to survive until bitcoin’s price increases sufficiently. In June, miners offloaded $2 billion worth of BTC to stay afloat, marking the fastest sell-off in over a year. This selling pressure has countered demand from ETFs and kept bitcoin’s price within its current range.

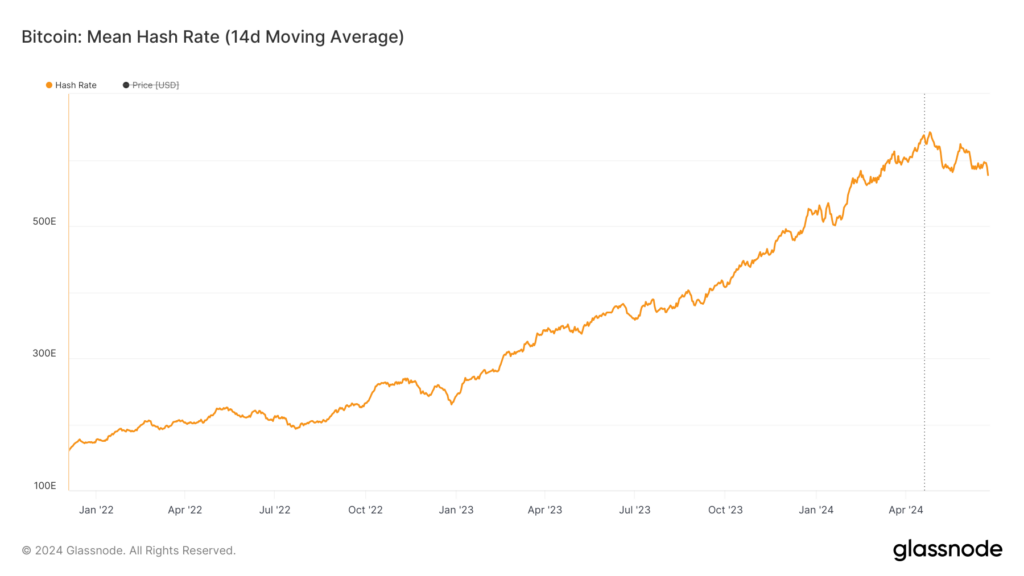

However, this selling pressure may now be starting to ease as some miners have likely exhausted their reserve bitcoin or opted to halt their operations. This is indicated by a significant decline in the network’s Hash Rate, which measures the total computational power on the Bitcoin network. The 14-day moving average for Hash Rate has decreased by about 10% since its peak on April 25th, suggesting that miners are shutting down operations—a sign of capitulation.

Miner capitulation can also be tracked using a metric known as Hash Ribbons, which compares the 30-day and 60-day averages of Hash Rate. This metric helps identify when miners are unplugging their machines due to unprofitability. When the 30-day average falls below the 60-day average, it indicates that miners are exiting the network rapidly (i.e., miner capitulation). These periods are shown in light red in the chart below and have been the case for the past two months. When the 30-day average of the Hash Rate crosses back above the 60-day moving average (switch from light red to dark red areas in the graph below), it historically indicates that the worst of the miner capitulation is over.

Currently, we are likely witnessing the weakest miners being flushed out of the market, a common occurrence post-halving. Following the 2016 Halving, bitcoin’s price traded sideways for about 182 days, and after the 2020 Halving, it moved sideways for approximately 161 days. As of today, it has been 81 days since the Halving in April. We are right in line with previous cycles, and once this sell-off phase concludes, I expect bitcoin’s price to start recovering.

It’s worth reiterating that bitcoin bull markets are filled with drawdowns of equal or greater magnitude than the one we saw last week that was caused by the market’s misconceptions around Mt. Gox. The miner capitulation that has suppressed bitcoin’s price since the Halving in April is normal and expected. These periods of time can be unsettling for newer, less experienced market participants who have not seen these patterns play out before. Back in March, we wrote, “the best thing anyone can do is to not get sucked into the day-to-day madness of crypto’s price movements and remember bitcoin has historically rewarded those who hold for the long term.” Those words are as true now as they were then. I fully expect that by the end of 2024, bitcoin will have reached new all-time highs, and those with conviction and patience will be rewarded as they always have been.

The Chevron Doctrine runs out of gas

On June 28th, the Supreme Court struck down the Chevron Doctrine in a 6-3 opinion, marking a significant shift in the balance of power between the judiciary and federal agencies. This ruling has major implications for various industries, especially the crypto industry. To understand the controversy and its impact on the crypto industry, it’s essential to first grasp what the Chevron Doctrine entails.

The Chevron Doctrine was established by the U.S. Supreme Court in the 1984 case Chevron U.S.A., Inc. v. Natural Resources Defense Council, Inc. In this case, the Supreme Court set forth the principle that when laws are ambiguous, courts should defer to the federal agencies responsible for enforcing those statutes, provided the agency’s interpretation is reasonable. This doctrine is founded on the notion that agencies possess expertise in their specific areas and are better equipped than courts to make policy decisions within their regulatory domains.

Critics argue that deference to federal agencies under Chevron can lead to an expansion of the agency’s regulatory reach beyond what Congress originally intended, potentially allowing the agency to impose broad and impactful regulations with limited oversight. Additionally, agencies have shown a propensity to reinterpret laws with each new administration, effectively changing the rules every few years. The debate over Chevron and the Supreme Court’s recent ruling is fueled by differing views on the appropriate role of administrative agencies in the separation of powers—some see strong agency authority as necessary for effective regulation, while others view it as overreach.

It’s worth recognizing that striking down 40 years of legal precedent that impacts just about every industry in the U.S. is not without its pros and cons. To be clear, I have no expertise in constitutional law nor am I an authority on the numerous industries impacted by the Chevron Doctrine. My intent with this article is not to opine on whether the Supreme Court’s ruling is correct or incorrect, nor to assess its implications for other industries. It’s merely to attempt to explain what a potentially profound impact this ruling might have on the crypto industry who has had to endure years of broad overreach and novel legal theories from the SEC in the absence of any congressional legislation.

Because the U.S. lacks clear legislation with regards to digital assets, cryptoassets and the businesses in this industry do not fit neatly into existing laws. Over the years, the SEC has exploited this legal ambiguity to expand its power and authority over the industry. This is why Gary Gensler has repeatedly claimed that all cryptoassets, except bitcoin, are securities, despite the absence of explicit laws or congressional authority to make such determinations.

As of June 28th, courts are no longer required to defer to the SEC’s interpretation of ambiguities in securities statutes. This development is a significant win for the crypto industry because judges now have more power to interpret the law independently, thereby limiting the SEC’s authority over the industry.

For instance, the SEC’s cases against Coinbase, Kraken, Binance, Consensys and others have likely been significantly weakened. The judges in these cases are no longer obligated to defer to the SEC’s novel interpretation of the Howey Test and can rule based solely on the letter of the law. This could be a substantial setback for the SEC, which has been trying to classify digital assets as securities by expanding the definition of investment contract to include “ecosystems” in addition to common enterprises. If the SEC cannot use the Howey Test to claim that crypto assets are securities, their entire case could collapse.

This ruling has significant implications for SAB 121, which was overturned by a bipartisan majority in both the House and the Senate, only to be vetoed by the president. It was determined by the Governance Accountability Office that the SEC violated the Administrative Procedure Act and Congressional Review Act when they issued SAB 121. The agency also overstepped their authority by ruling on an accounting issue despite lacking legal authority over accounting laws, a responsibility that falls to the Financial Accounting Standards Board (FASB). By exceeding their Congressional mandate, the SEC has opened the door for numerous lawsuits, especially now that the Chevron Doctrine is no longer in effect. It is highly likely that someone will sue the SEC over SAB 121 and win in court.

The Chevron Doctrine is a key reason why Gary Gensler has publicly stated that he believes no new laws are needed specifically for crypto. This doctrine is what has given the SEC the legal leeway to enact its regulation by enforcement campaign on the crypto industry in absence of clear laws. It’s no surprise that the SEC has repeatedly lobbied against any proposed crypto market structure bills. Such legislation would clarify the regulatory landscape in the U.S., compelling the SEC to follow clear directives from Congress rather than relying on its own interpretations. This shift would significantly reduce the SEC’s authority over the crypto industry.

The overturning of Chevron does not strip the SEC of its ability to bring enforcement actions. The SEC can still present its belief that certain activities violate securities laws to a judge, who will then interpret the existing law to make a decision. However, now the SEC, CFTC, and banking regulators must adhere strictly to the laws as written, not as they interpret them. This means the SEC’s claim of full jurisdiction over crypto matters less today than it did before June 28th, raising questions about whether Congress has granted the SEC authority to regulate crypto based on whether or not it’s a security.

The Supreme Court’s ruling also places the responsibility on Congress to pass comprehensive crypto market structure legislation, such as FIT21. If agencies like the SEC and the CFTC cannot properly regulate the industries they oversee due to outdated or nonexistent laws (current securities laws date back to the 1940s), then new legislation from Congress is essential. Congress can no longer defer to these agencies to address issues independently; they must take proactive steps. Hopefully, without the Chevron Doctrine to lean on, Congress may feel an increased urgency to update current legislation. In the long run, this ruling should be beneficial for the crypto space, providing greater judicial and legal certainty.

In Other News

VanEck files for a Solana ETF.

Bitcoin ETFs saw $130M of inflows on the first day of July.

Coinbase filed a lawsuit against the SEC and FDIC, alleging that the regulators didn’t comply with Coinbase’s FOIA requests that the exchange believes would shed light on the coordinated efforts by regulators to deny crypto companies access to the banking system.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS