By Brett Munster

Bitcoin derives its value from several groundbreaking features that set it apart from traditional assets and currencies. The ability for individuals to self-custody their wealth eliminates counterparty risk, offering a unique financial solution for people living under authoritarian regimes who seek to engage in global commerce without government interference. Its seizure-resistant and borderless nature makes bitcoin an ideal tool for humanitarian aid and cross-border remittances, empowering users worldwide. Bitcoin mining operates as a persistent buyer of unused energy, providing a critical demand response mechanism that stabilizes power grids, reduces energy costs for consumers, and accelerates the development of renewable energy technologies. Moreover, its economic value is supported by the largest computing network in existence, surpassing the combined scale of Amazon AWS, Google Cloud, and Microsoft Azure by several times. Yet perhaps bitcoin’s most transformative feature is its monetary policy, which offers a fixed supply and a predictable issuance schedule that is immune to manipulation, standing in stark contrast to fiat currencies that can be printed at will.

Bitcoin’s supply is capped at 21 million, establishing a fixed limit that guarantees absolute scarcity, unlike fiat currencies, which can be printed without restriction. This unlimited printing creates perpetual inflationary pressure in fiat systems, as new money is continually introduced to manage debt and stimulate the economy. In contrast, bitcoin’s supply not only remains limited, but its issuance rate decreases over time through scheduled “halving” events. This built-in disinflationary mechanism is the inverse of fiat currencies like the U.S. dollar, which have seen accelerated issuance over time.

The predictability of bitcoin’s monetary policy further distinguishes it from traditional fiat currencies. With its decentralized network, bitcoin is immune to manipulation by governments or central banks, ensuring its supply and issuance remain free from political influence. In contrast, fiat currencies are subject to the decisions of small groups of central bankers and policymakers, whose decisions are often made behind closed doors and influenced by political considerations. As a result, the monetary policy surrounding fiat currencies lacks transparency, and markets are left speculating on the direction of interest rates and liquidity based on cryptic signals from central banks. Bitcoin, by comparison, operates with a high degree of certainty—its issuance schedule is fixed, unchangeable, and fully predictable. In essence, bitcoin’s monetary policy is the exact opposite of the U.S. dollar and all other fiat currencies.

Given this, it stands to reason that bitcoin’s value proposition should become more apparent whenever fiat currency supplies expand and purchasing power is diluted. The data supports this correlation: when the money supply grows, bitcoin’s price tends to rise in response, as investors seek a scarce asset to preserve value.

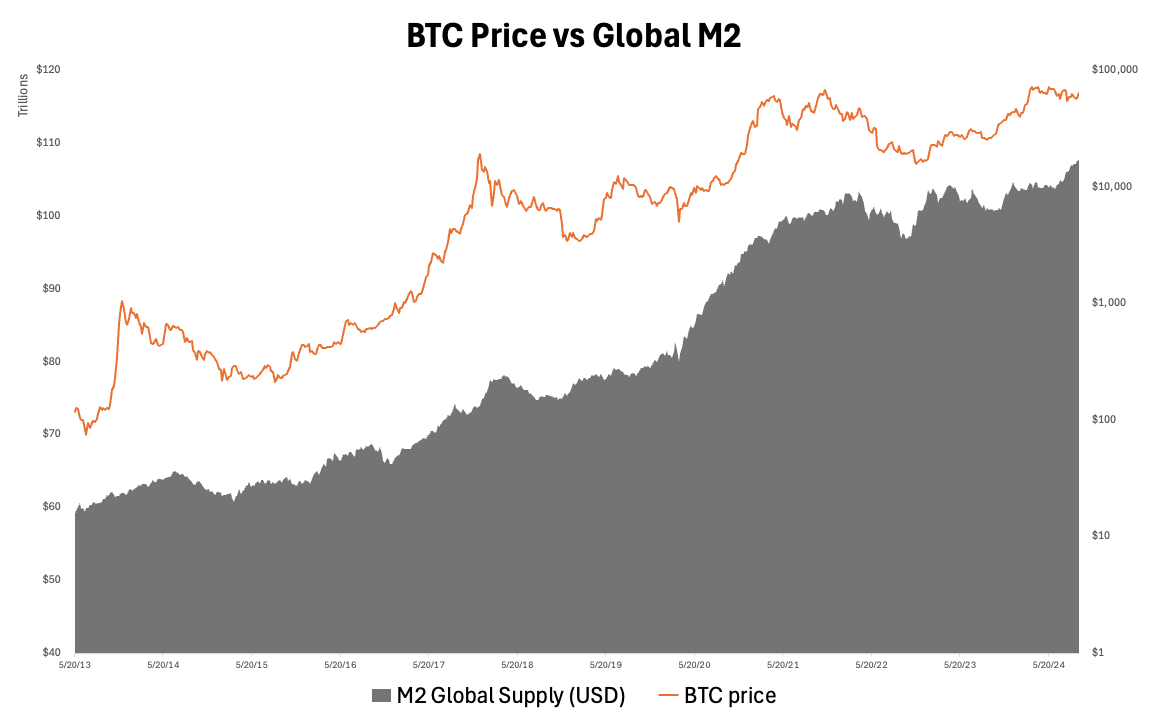

One key metric for assessing liquidity is M2, which measures the total money available for spending or investment in an economy. When M2 data from the world’s largest central banks is aggregated, it provides a snapshot of global liquidity, a crucial factor since bitcoin is a globally accessible asset. Global M2 effectively measures the extent of credit creation and central bank money printing (monetary debasement) happening worldwide.

Historically, bitcoin has shown a strong correlation with Global M2. As global liquidity expands, bitcoin’s price tends to rise, which makes sense given that when currencies become more abundant and their value depreciates, investors seek out scarce assets that are better positioned to preserve value—bitcoin being the prime example.

Taking the analysis further, we can examine the year-over-year percentage changes in both bitcoin and global liquidity. This comparison not only underscores how closely the two tend to move in sync, but also reveals how sharply bitcoin’s price reacts to increases in global liquidity. Historically, linear changes in global M2 have led to exponential price movements in bitcoin—a unique phenomenon driven by its absolute scarcity, around-the-clock trading, and monetary policy that starkly contrasts with that of fiat currencies.

Research by Lyn Alden underscores this relationship, showing that bitcoin consistently exhibits the highest correlation with global liquidity over any 12-month period, more so than traditional asset classes like stocks, bonds, or commodities. Alden notes that “Bitcoin moves in the direction of global liquidity 83% of the time in any given 12-month period, making it a strong barometer of liquidity conditions.” Traditional assets, by contrast, are influenced by factors beyond liquidity, such as corporate earnings or geopolitical risks, which weakens their correlation with liquidity.

Gold, for example, benefits from rising liquidity and a weakening dollar, but its performance is also influenced by its role as a “safe haven asset”, meaning its price can hold up well even when liquidity contracts. Stocks, meanwhile, are driven not only by liquidity but also by company fundamentals like earnings and dividends. As a result, neither gold nor stocks reflect global liquidity conditions as purely as bitcoin does. As Lyn puts it, “One can think of bitcoin as a mirror reflecting the rate of global money creation.”

Macro strategist Raoul Pal has extensively studied the relationship between global liquidity and asset performance. His research highlights that modern economies—particularly in developed nations—are heavily reliant on debt and central bank interventions. The widespread use of quantitative easing (QE) to inject liquidity into the system has made asset prices increasingly dependent on central bank policies. However, most traditional assets struggle to keep pace with the rate of monetary debasement. According to Pal’s analysis, global liquidity, which he measures using more advanced techniques than simply Global M2, has grown at an annualized rate of 8% since 2008. Even using a simplified Global M2 measurement, the world’s money supply has increased at a compounded annual rate of 7.2%.

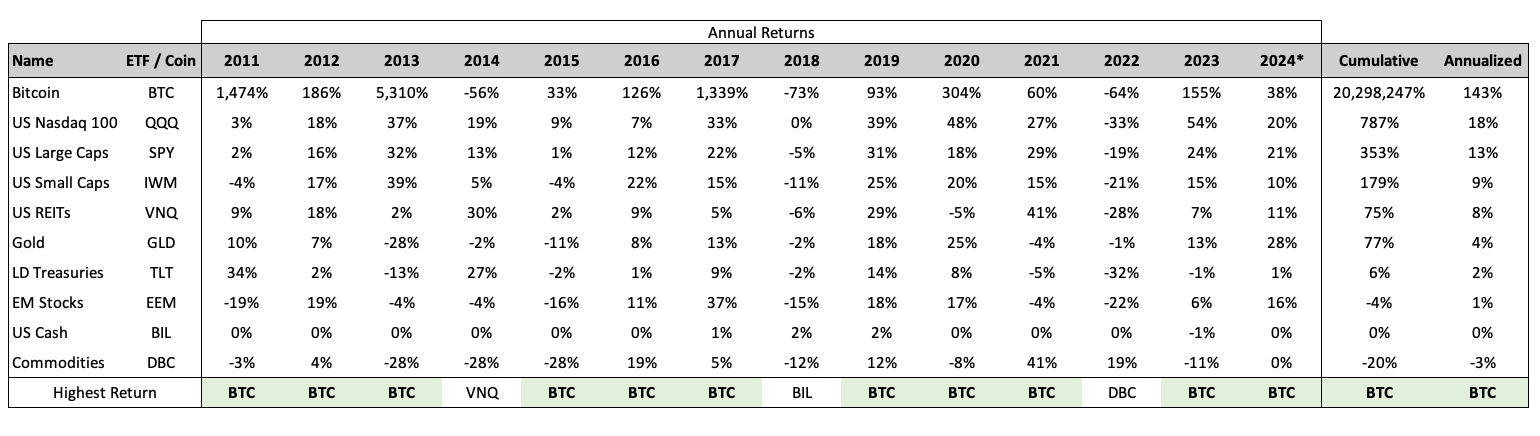

When looking specifically at the U.S. dollar, the average annual growth of its supply has been roughly 7% since 1960—a figure notably higher than the inflation rates reported by the Federal Reserve. The reason for this discrepancy lies in the shortcomings of the Consumer Price Index (CPI), which is a flawed and manipulated metric. If CPI were calculated using the same methodology from the 1980s, before numerous revisions, inflation would more accurately reflect rates closer to 8-10%, aligning more closely with the pace of global liquidity growth. This gap highlights the importance of using liquidity expansion as a more reliable indicator of purchasing power. As Raoul Pal points out, most traditional assets have failed to keep up with the rapid pace of global liquidity growth, resulting in negative real returns. Over time, only the Nasdaq 100 and U.S. Large Cap stocks have managed to outpace monetary debasement, and even then, just by a slim margin.

Bitcoin, on the other hand, has vastly outperformed other assets during this period of aggressive money printing. Unlike stocks, bonds, or real estate, bitcoin’s absolute scarcity and its inverse monetary policy to that of fiat currencies make it uniquely positioned to respond to rising global liquidity with exponential price increases.

Given this framework, the logical conclusion is that if global liquidity continues to rise, bitcoin remains the best expression of this trend. This conclusion is particularly relevant now, as global liquidity is increasing again after a period of contraction.

From March 2022 to September 2024, financial conditions tightened sharply as central banks—led by the U.S. Federal Reserve—pursued aggressive monetary policy to curb runaway inflation. The Fed raised its benchmark interest rate from near zero to over 5% by mid-2023, marking one of the fastest rate hikes in decades. In parallel, the Fed embarked on quantitative tightening, shrinking its balance sheet by nearly $2 trillion as maturing bonds were allowed to roll off without reinvestment. The broader contraction in liquidity was further highlighted by a 5% decline in M2 money supply, according to data from the Federal Reserve Bank of St. Louis.

However, such aggressive tightening measures were unsustainable given the U.S. government’s growing debt burden. As we’ve argued before, the structural reality of the U.S. debt spiral essentially guarantees continuous money printing, leading to currency debasement over time. Rising interest rates have caused an exponential increase interest payments on U.S. government debt, which inevitably forced the Fed to reverse course. This shift from a tightening cycle to looser monetary policy began in September 2024 when the Fed cut interest rates by 50 basis points and signaled that further cuts are likely by year-end. While the M2 money supply hasn’t yet returned to its early 2022 peak, it is back on an upward trajectory and is projected to reach new highs by next year.

But there’s even more liquidity poised to enter the system. In response to rising rates in 2022, capital flowed into yield-bearing assets such as U.S. money market funds, which swelled to a record $6.5 trillion. These low-risk, highly liquid investments became an attractive alternative to cash by investing in instruments like Treasuries. However, as interest rates come down, the yields on these funds will diminish, pushing this massive sum of money to seek more attractive opportunities. A substantial portion of this capital will likely seek higher returns, some of which will flow into bitcoin.

And it’s not just the U.S. reversing course. Central banks worldwide are loosening financial conditions in tandem. The European Central Bank recently cut rates for the second time in three months, the Bank of England cut rates in August, and the Bank of Canada has slashed rates three times since June. Similar rate cuts have been enacted by the Swiss National Bank, Sweden’s Riksbank, and South Africa’s central bank. In fact, September saw the highest number of global rate cuts since April 2020.

China is also playing a key role in this global liquidity surge. Facing significant economic challenges, the People’s Bank of China (PBOC) has initiated its largest monetary stimulus since the COVID-19 pandemic. This includes the largest interest rate cut since 2016, a reduction in banks’ reserve requirements to inject $142 billion into the financial system, and a $113 billion “stock stabilization fund” to boost market liquidity. Additionally, further rate cuts and liquidity measures are expected from China in the near future.

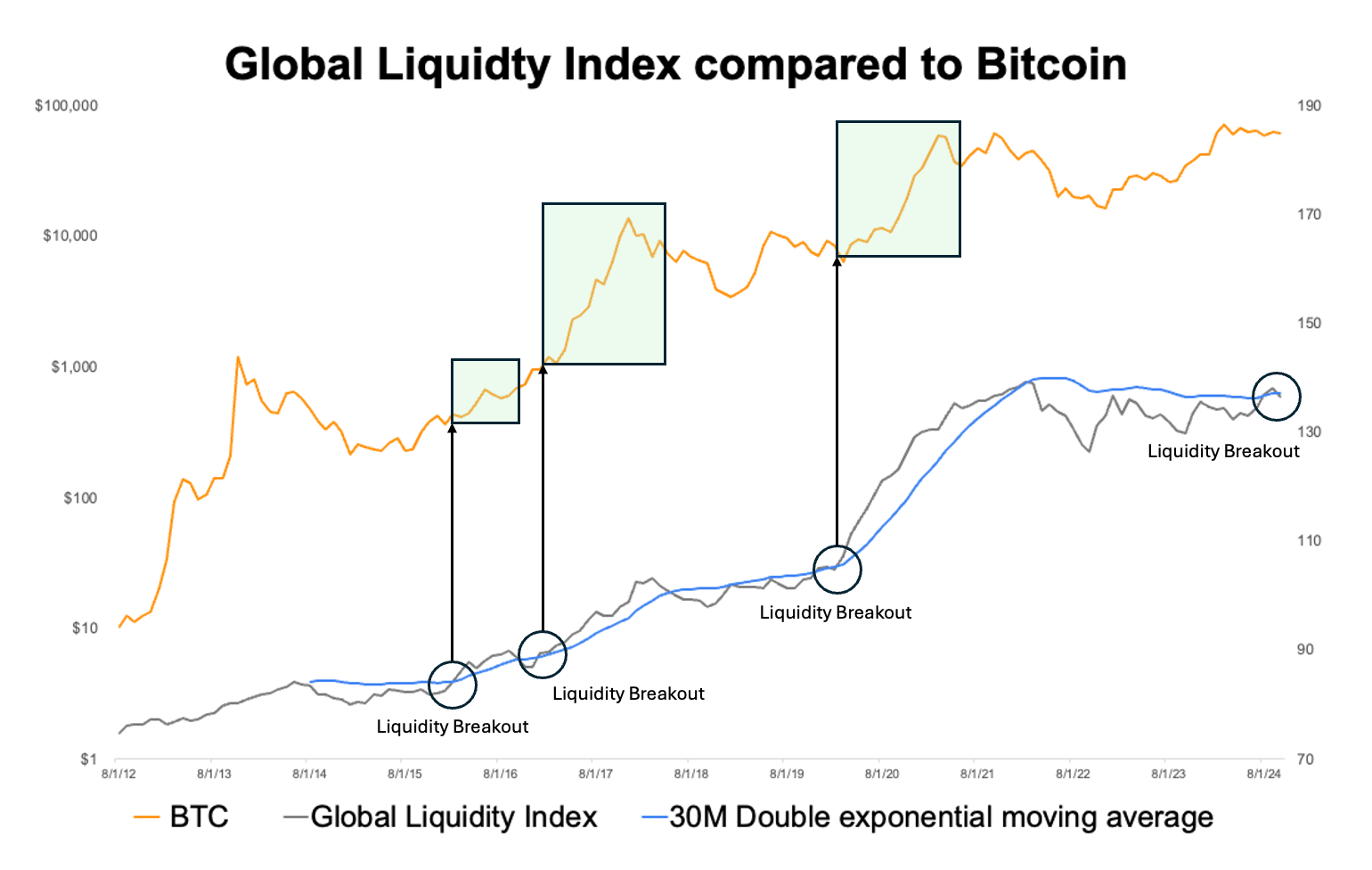

Global liquidity is on the rise again, with central banks across the world injecting cheap capital into their economies. As shown in the graph below, when global liquidity has exceeded its moving average in the past, it has often coincided with significant upward movements in the price of Bitcoin. Notably, global liquidity has recently crossed back above its moving average, signaling a potential shift in market dynamics. This influx of liquidity will continue to debase fiat currencies, as evidenced by global M2 already reaching new all-time highs, with more growth expected over the next year. Bitcoin, which is highly sensitive to shifts in liquidity, is positioned for a potentially explosive move as fresh capital floods the system. Even BlackRock has quietly indicated it’s preparing for a Federal Reserve-driven dollar crisis by leaning into bitcoin as a key hedge against currency debasement. After six months of price consolidation this year, the stage is set for a perfect storm in favor of bitcoin and other crypto assets.

In Other News

Ohio Senator introduces bill to allow bitcoin, crypto payments for state taxes.

Representative Ro Khanna became the first Democrat to publicly support the idea of the United States building a strategic reserve of bitcoin.

Crypto.com sues SEC after receiving Wells Notice.

Regulators are limiting banks serving crypto clients.

The SEC’s retraction exposes the lie behind “crypto asset securities.”

Uniswap Labs unveils its own layer-2 network, Unichain, built on Optimism tech.

Fidelity plans first fund using blockchains.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS