By Brett Munster

Good Morning!

Last newsletter we did a look back and highlighted the top stories of 2022. This week we wanted to give a glimpse of the trends we will be watching in 2023.

Bitcoin

Let’s start with the oldest and largest cryptoasset. Despite the price falling 75% since its all-time high in November 2021, adoption continued to grow throughout 2022. In our last newsletter we highlighted numerous examples of citizens, corporations, governments, and financial institutions embracing crypto throughout last year. We expect 2023 to be very similar in this regard.

For a significant portion of the world’s population, bitcoin offers a better form of saving, means of transacting, and increased access to financial services. Because we in the US often take our financial system for granted, many view crypto’s only use case as speculation, but for much of the world, bitcoin is providing tangible life improving benefits. We expect to see adoption accelerate in locations experiencing hyperinflation and currency devaluation. Bitcoin proved itself indispensable for humanitarian aid in Ukraine in 2022. Don’t be surprised when other parts of the world that are also experiencing conflict turn to bitcoin as a financial tool in the coming years. Bitcoin is also offering an escape from authoritarian governments. In China, trading activity began to pick up towards the end of 2022 despite some of the world’s strongest government bans. Even mining, which saw a huge drop off following the ban in 2021, has made a comeback in China.

Talk all you want about price and volatility, the value proposition of a permissionless, transparent monetary system that can’t be controlled or confiscated by a central authority has only strengthened as sovereign currencies around the world have shown signs of stress. So long as we continue to see monetary debasement from currencies around the globe, strict capital controls imposed by authoritarian governments, and financial corruption throughout the world, bitcoin’s adoption will continue to increase regardless of what price it is trading at.

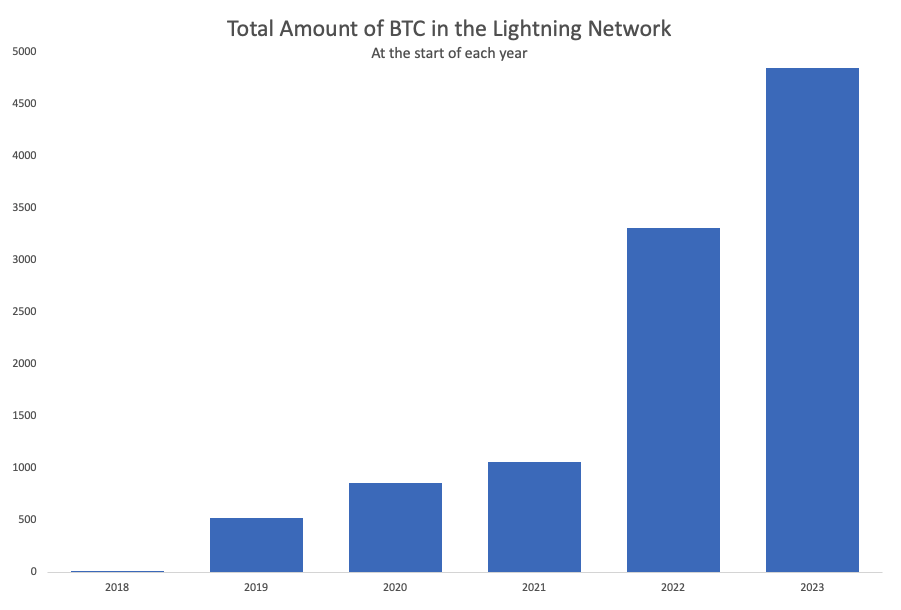

And that’s before you consider the impact of the Lightning Network. The Lightning Network is a network of payment channels built on top of Bitcoin’s base layer blockchain that enables instant, nearly-free bitcoin denominated payments to anyone in the world. The adoption and use of the Lightning Network (and thus the usage of bitcoin) has been growing exponentially over the last couple of years as citizens in Latin America, the Middle East and North Africa use the Lightning Network to buy groceries and other everyday items. Channel capacity is continually setting all-time highs and preeminent industry leaders in finance and technology are beginning to incorporate the Lightning Network. Furthermore, there are a number of important Lightning-enabled protocols being developed (such as Taro), that have the potential to expand the utility of the Bitcoin network beyond a store of value. The Lightning Network is poised to become the largest interconnected global payment system ever created. Lightning Network’s growth isn’t slowing down anytime soon which is why we expect adoption of bitcoin to accelerate in 2023.

Data Source: Glassnode

Which ultimately brings us back to the topic everyone wants to talk about, price. Because bitcoin has a capped supply, so long as demand continues to grow, price will continue to rise over a long enough time frame. This is why our conviction regarding bitcoin’s price appreciation over the next decade remains extremely high. That doesn’t mean it will be a straight line, there undoubtedly will be volatility but there is reason to believe the worst is now behind us. Many on-chain metrics, market structure, and investor behavior patterns resemble past bear market floors. It’s a matter of when bitcoin will once again reach new all-time highs, not if. The biggest unknown at this point is the duration of this current down market. History would suggest there may be several months still ahead before a full recovery. Our best guess is that we likely won’t see a v-shaped recovery, but rather, we could experience sideways action for some time before moving back up. However, when the next bull run hits, bitcoin’s price is likely to rise faster and higher than most people expect.

Ethereum, Staking and Layer 2 Networks

Of all the smart contract platforms, Ethereum is still the market leader by a wide margin. ETH consists of 62% of the market cap for all smart contract platforms in existence. The next largest, Binance Smart Chain (BNB), holds 16.7%. Ethereum is the underlying technology for the most successful DeFi apps, the largest NFT market, and represents nearly 60% of total value locked (TVL). And that’s before Ethereum’s merge to Proof-of-Stake has really had a chance to make an impact on the ecosystem.

The Merge marked a fundamental shift in the economic model of Ethereum. It reduced new token issuance by 90% and eliminated nearly $500 million of monthly sell pressure from miners. As a result, we expect ETH to become net deflationary in 2023 meaning more ETH will be burned (destroyed) than created over the course of the year.

The Merge also created the ability for holders of ETH to earn a yield on their assets through “staking.” Staking simply means depositing ETH onto the network to operate and validate transactions. In return, stakers earn a fee. Currently, while it’s possible to stake ETH, it’s impossible to un-stake. Think Hotel California; you can check in, but you can never leave. This lack of liquidity increases the risk of staking today. However, Ethereum developers are targeting March for the new Shanghai Fork (fancy way of saying update to the network) which will give users the ability to withdraw their staked Ether. We expect the ability to stake and unstake at any time to increase investor willingness to stake ETH. According to Glassnode, about 13.2% of all ETH is currently staked. We expect that percentage to rise considerably over the course of the year.

The combination of total supply decreasing and an increased amount of supply tied up in staking should drastically decrease the amount of ETH available to be traded on the open market. In theory, this should put upward pressure on the price of ETH over time.

Lastly, we can’t talk about the Ethereum ecosystem without discussing Layer 2 networks. Last July, we published our Layer 2 thesis and thus far, we seem to have hit the nail on the head. As a quick refresher, Layer 2 networks improve blockchain scalability and reduce fees for users by executing transactions on separate blockchains, then posting compressed transaction data to the base layer Ethereum blockchain.

Layer 2 networks quietly had a breakout year in 2022, with extraordinary growth and numerous milestones at both the infrastructure and application layers. According to L2Beat, over the course of November and December, the Ethereum ecosystem was able to process 2.4x more transactions with Layer 2 networks than the Ethereum base blockchain would have done on its own. That means more transactions occurred on Layer 2 networks than on Ethereum in the last two months. In addition, the share of total Ethereum gas used by Layer 2s tripled in 2022 which is a clear indication of increased usage. We expect this trend to continue and believe that transaction count on Layer 2s will easily exceed (maybe even double) transaction volume on Ethereum in 2023 as more and more activity migrates to Layer 2 networks.

DeFi

For every collapse of a centralized company in 2022 there was a perfect substitute in DeFi that not only survived the turmoil of this past year but worked as intended without interruption. While centralized crypto lenders Celsius, Blockfi and Voyager went bankrupt, DeFi protocols such as Aave and Compound were the first to get paid back. Following the collapse of FTX, Uniswap, the leading decentralized exchange, saw a significant spike in volume due to users taking their assets off centralized exchanges and moving to self-custody. None of the stalwart DeFi protocols went down, none created debt greater than their assets, and none defaulted on their users in 2022. Despite the market chaos caused by fraudulent off-chain activities, DeFi showcased the benefits of decentralization. Other than a drop in Total Value Locked (TVL), these DeFi protocols remain fully collateralized and healthy heading into 2023. The back half of last year was a perfect illustration of the benefits and safety decentralized smart contracts have over centralized services.

We expect to see a greater push away from centralized services starting in 2023 and continuing in the coming years as more users, developers, and even regulators realize the value of eliminating middlemen. That trend, along with the continued buildout and strengthening of the current DeFi landscape bodes well for this sector of the crypto industry. Perhaps no one laid out the argument for DeFi’s potential upside better than Ryan Selkis in his 2023 annual report:

“The entire universe of free-floating DeFi tokens currently trades at less than $15 billion. That doesn’t even crack the top 100 banks by market cap. DeFi’s market share of global financial services is a measly 0.2%. Meanwhile, Total Value Locked (“TVL,” a measure of user assets deposited into a protocol’s smart contracts) in DeFi is just $40 billion, barely good enough to crack the top 50 US banks by assets…but positive regulatory developments, improvements in contract security and development best practices, and lower transaction fees thanks to scaling breakthroughs could make DeFi one of the best risk reward sectors of crypto for years to come. The global financial services industry is valued at nearly $23 trillion. So, a $15 billion DeFi sector doesn’t seem frothy to me.”

Decentralized Infrastructure

The biggest economic disruptions happen when a technological innovation is coupled with a business model innovation. Apple not only made the iPod and iPhone (tech innovations) they pioneered iTunes and later the app store (business model innovation) that disrupted the music and phone industry. Though Google wasn’t the first search engine, Larry and Sergei did build a more scalable method of cataloging the web (tech innovation) and layered in a bidding system known as AdWords (business model innovation). Facebook created a better way for people from around the world to connect and share pictures (tech innovation), but it was the creation of the News Feed that made advertisements seamlessly integrated into other content rather than using annoying banner ads that propelled its revenue growth (business model innovation). Netflix leveraged streaming (tech innovation) to get into 220 million homes but was initially built on a subscription service that eliminated late fees (business model innovation). The cloud enabled much better scaling (tech innovation) but also ushered in subscription as a service (business model innovation) which lowered costs and better aligned incentives between buyers and sellers.

Which brings us to decentralized infrastructure because blockchain networks are both a technological and business model innovation. The technological innovation is the digital scarcity and immutable records of transactions without the need for middlemen. However, it’s the token associated with that blockchain that provides the business model innovation because the token allows the users of the product to also participate in the economic value creation. Thus, the cost to build the infrastructure can be distributed over a large network of supporters rather than borne by one company.

Decentralized infrastructure is a small, but emerging category of the crypto landscape both in terms of size and importance. Services such as file storage, wireless access, and cloud computing require lots of operational expertise and capital expenditure to build the physical infrastructure needed to operate at scale. This is why we have entrenched corporations with little competition such as Amazon or Microsoft for hosting and Google for searching. Rather than compete directly, tokens have proven effective at catalyzing the development of user-owned networks from the bottom up rather than requiring a ton of upfront capital.

Capacity and utilization for decentralized cloud storage networks Filecoin and Arweave have steadily and consistently grown over the past 18 months. Helium, a decentralized wireless network, has nearly a million individually owned hotspots in over 180 countries worldwide. Chainlink continues to see consistent active user growth as it provides real world data to various blockchains and DeFi protocols throughout the ecosystem. The Graph, which builds and publishes open APIs that make on-chain data easily accessible, has seen an explosion of growth over the past six months.

These are just some of the first examples of decentralized blockchains actively disrupting legacy software and physical infrastructure. Properly implemented tokenomics allows independent network participants to easily coordinate economic activity required to build a global network while also allowing participants to directly benefit from its success. Though early, we expect to see blockchain based networks take on infrastructure incumbents in more markets over the coming years.

The tokenization of everything

In our October 18th edition of this newsletter, we wrote about how tokenized assets represent digital shares that allow for increased access and liquidity, near-instantaneous transaction settlement, and regulatory compliant ownership of any real world or virtual asset. Tokenizing real-world assets can create liquid markets for previously illiquid assets and in doing so, unlock new markets that were never before possible. In addition, it’s possible to create tokenized assets that come pre-packaged with a regulatory-compliant governance system which could allow regulators to be proactive, rather than reactive, in their enforcement of laws, thereby significantly minimizing the burden on enforcement agencies to monitor and enforce securities law.

In 2022, we saw the very beginnings of this trend start to come to fruition. KKR, one of the world’s largest investment firms, tokenized its healthcare fund and in doing so, increased access to the fund by simplifying the onboarding and compliance processes, lowering investment minimums, and increasing liquidity. Hamilton Lane, once only accessible to financial institutions, will now be available to qualified US-based investors after it announced it tokenized three of its funds. Goldman Sachs launched its own Digital Asset Platform in which it can tokenize traditional financial products in order to increase efficiency and liquidity. For example, in November, the platform was able to reduce the typical bond issuance settlement time for the European Investment Bank (EIB) from five days to sub-60 seconds. Recently, a group of 12 banks (including Bank of America, Citi, BNY Mellon and Wells Fargo), conducted a pilot program to tokenize various projects in order to reduce the time it takes to settle transactions from 2 – 3 days down to same day settlement.

In time, it won’t just be BTC and ETH traded on blockchains. Real estate, government and corporate bonds, private equity funds, carbon credits, insurance, commodities, art, collectibles, and more will be tokenized and traded on blockchains. We are in the very early stages of this transition, but we expect to see more organizations experimenting with tokenization in 2023.

Regulation

The crypto industry is full of the unexpected but the one thing you can take to the bank is that 2023 will be a busy year on the regulatory front. The challenge with the current regulatory regime in the US isn’t anti-crypto policies (in fact the vast majority of bills that have actually passed have historically been very pro-crypto), it’s been a lack of clarity on a number of key topics. However, at the start of 2022, we highlighted how a growing number of politicians were embracing the crypto industry and fortunately, many of them got elected in November. The new House majority whip, Tom Emmer, is a staunch crypto advocate and one of the most knowledgeable individuals in Washington on the industry. So, the need for crypto regulation is already gaining steam. The collapse of LUNA, Celsius, Blockfi and especially FTX only further catalyzed the desire within Washington to finally act.

So, what does that mean for 2023? Well, the one thing all regulators seem to agree on is the need for greater consumer protection and preventing money laundering or other illicit financial activity. What parts of the crypto ecosystem get regulated and how those laws are constructed however, is up for debate.

Let’s start with bitcoin. The mainstream view in DC, among a majority of both Republicans and Democrats, is that there really isn’t much to worry about with regards to bitcoin specifically. Many in Washington have started to understand the benefits of bitcoin (the rest of the crypto industry is a different story) and are increasingly taking the view that bitcoin aligns with many American ideals. In fact, it’s rather hard to argue for consumer protection and at the same time argue against the ability for users to retain full control over their assets (aka self-custody) rather than depositing money onto exchanges such as FTX. It’s also hard to argue for policies protecting against illicit financial transactions and also be anti-bitcoin because every transaction on the bitcoin blockchain is recorded and publicly viewable. In fact, far less illicit finance happens in bitcoin than regular cash on both a total amount and percent basis. Other than the perceived environmental impact of mining, which the data is already beginning to change many people’s mind about, bitcoin is largely not a threat in most politician’s eyes. The bottom line is that policymakers and regulators believe there are much bigger risks within the crypto industry than bitcoin.

Which brings us to exchanges and stablecoins. The same desire for consumer protection does mean the primary focus right now is regulating centralized exchanges and stablecoins.

Crypto’s market cap and trading volumes center around bitcoin, stablecoins and decentralized smart contract platforms (such as Ethereum) that any regulator would be hard pressed to argue are investment contracts or securities. Thus, the prevailing view on Capitol Hill is that the CFTC is the most appropriate regulator for most crypto activity today. Expect legislation to be passed sometime in 2023 that officially gives the CFTC oversight of exchanges and custodians. This would be a massively positive development because it would bring much more clarity to the industry and likely investor confidence because although the CFTC has teeth, they are not outright hostile to the industry as the SEC has been under Gary Gensler.

With a record $7 trillion settled in 2022, stablecoins have demonstrated clear product-market fit. USDC, USDT and BUSD are being used heavily within DeFi applications, for international commerce, and as a convenient medium of exchange. As a result, regulations surrounding stablecoins have been increasing in urgency among policymakers, but nothing has officially been passed yet. Expect that to change in 2023 as stablecoin issuers will likely face new oversight requirements. It will be interesting to see what the reserve requirements will be, what licensing will be required, how algorithmic stablecoins will be treated and any other rules stablecoin issuers will need to follow in order to be in compliance with US law.

While exchanges and stablecoins are the two most likely areas of regulation, DeFi will be a wild card to watch in 2023. Maybe the most divisive crypto topic currently being discussed in Washington, the DCCPA bill (which would have created a lot more barriers for DeFi protocols to operate within the US and was bankrolled by Sam Bankman-Fried because it would have given FTX regulatory advantages) seems to now be dead in the water. The fact that SBF was championing such rules against DeFi and that DeFi protocols held up so well throughout the turmoil is causing a lot of politicians to reconsider their stance on DeFi. At the very least, many politicians want to distance themselves from the topic, not that many understand it in the first place, so it will be very interesting to see if any regulation regarding DeFi passes in 2023 or if its largely left alone.

In Other News

$5 billion has been recovered thus far in FTX bankruptcy.

Bitcoin miners return enough power to heat 1.5 million homes during Texas winter storm.

Seven reasons to believe in crypto after 2022 implosion.

Reasons to remain bullish after a year in crypto hell.

Blackrock adds bitcoin to its Global Allocation Fund.

The U.S. District Court of the Southern District of New York released Caroline Ellison’s confession, in which she told the court she worked with Sam Bankman-Fried to deceive lenders and fake the hedge fund’s financials.

Sam Bankman-Fried pleaded not guilty to eight counts of fraud, conspiracy, money laundering, and illegal campaign contributions, requesting to keep the identities of two people who will help secure his bail confidential.

FTX customers file class action suit to have their payments prioritized.

The Securities Commission of The Bahamas says it seized $3.5 billion worth of cryptocurrency from FTX and added that the funds were moved into its own digital wallets “for safekeeping.”

Coinbase reached a $100M settlement with the New York State Department of Financial Services for concerns over its anti-money laundering and know-your-customer practices

New York Attorney General Letitia James is suing former Celsius CEO Alex Mashinsky for defrauding customers of billions of dollars’ worth of crypto.

Genesis Global Capital and Gemini Trust, have both been charged with selling unregistered securities by the SEC.

Amazon Web Services users can now launch Avalanche blockchain nodes.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS