By Brett Munster

It feels like there is never a dull moment in crypto and the first quarter of this year has been no exception. Unfortunately, a number of actions taken by regulatory agencies in the US (some of which we cover in the newsletter below) over the past two months have been outright hostile to the crypto industry. Despite all the drama in Q1, it’s worth remembering bitcoin is up 70% year to date and the industry as a whole is up about 50% since the start of the year. Even Citigroup, which has been skeptical of crypto in the past, recently authored a report in which it claims the blockchain industry will be used by billions of people and grow to $5 trillion in value by 2030. Don’t let the short-term news cycle distract you from the long-term trajectory crypto is currently on.

The FDIC’s signature move

In the crypto industry, there were two primary banks, Silvergate Bank and Signature Bank, that most of the industry used over the last several years. Unlike Silvergate, where the majority of deposits were derived from crypto firms, Signature primarily serviced real estate. At the end of 2022, Signature had around $110B in deposits, of which roughly 20% came from crypto related clients. Similar to Silvergate’s SEN network, Signature had its own 24/7/365 settlement network for fiat to crypto called Signet. After Silvergate wound down and shuttered SEN, Signet was positioned to benefit as one of the last remaining critical crypto banking infrastructure providers. As we covered in our March 14th edition, Silvergate announced on March 8 that it would wind down operations and voluntarily liquidate the bank in an orderly manner including full repayment of all deposits. Four days later, Signature Bank was taken over by the NYDFS and FDIC.

The official reason for the New York State Department of Financial Services’ (NYDFS) decision to close Signature and name the FDIC as the receiver was to “protect depositors” and stop “systemic risk.” Here’s the puzzling thing about that explanation, Signature Bank was still fully solvent at the time the NYDFS forcefully took it over. In fact, Signature only held 7% of its total assets in long-dated securities, far less than Silvergate, SVB, and First Republic Bank. Furthermore, its unrealized losses on these securities were not particularly large, indicating that the bank was not actually at risk of a bank run. And as we just explained, Signature did not have the concentration risk that Silvergate had in crypto or SVB had in venture backed startups. This was not a case of bankers making bad loans or having poor risk management, which begs the question, why was Signature Bank forced into receivership?

The day after Signature was closed, Barney Frank affirmed that Signature was solvent, that leadership was shocked when the bank was put into receivership, and stated that the business would have been able to operate as normal had the NYDFS not stepped in. Who is Barney Frank you ask? Well, he is a former congressman and the “Frank” in Dodd-Frank, the 2010 bill designed to reform banking practices following the 2008 crash. He just so happens to also be a board member of Signature Bank. If there is anyone who is intimately knowledgeable on the intersection of banking policies and this particular bank, it would be this man. And he has said numerous times in various interviews that not only was Signature not at risk of going under but that the bank was shut down for purely political reasons. According to Frank, a noted crypto skeptic himself, Signature was closed to instill fear into other banks and incentivize them not to provide banking services to crypto companies.

And based on the evidence at hand, Barney Frank might have a point. First off, the NYDFS has avoided claiming that Signature was insolvent, even when asked directly. There appears to have been no credit risk, no interest rate risk, and no liquidity risk with regards to Signature. Instead, the regulator has made vague and subjective claims when pressed about why Signature was taken over such as “a lack of confidence in the bank’s leadership.” Assuming the claims about the financial health of the bank are true (and we have no reason at this point to believe otherwise), that would make Signature Bank the first ever bank to be put in receivership that was liquid and solvent. Second, other banks in presumably worse financial positions were given time to either save themselves by raising capital or accessing the Fed’s new BTFP facility. However, Signature was never given either of those opportunities. Third, most receivership situations occur on Friday afternoon after the market closes. However, Signature’s forced closing was snuck in on a Sunday night. Fourth, normally these types of actions get their own press release but not Signature. Instead, the FDIC decided to communicate the decision by burying it in the press release regarding Silicon Valley Bank. Even the FDIC was reportedly surprised on Sunday having not been previously told by the NYDFS that they would be taking over Signature Bank the following day. None of these are standard operating procedures.

And just in case you think I have my tin foil hat on, spewing government conspiracies, I’m not the only one with questions. The Wall Street Journal, notoriously critical of the crypto industry, wrote not one but two articles agreeing with Barney Frank and claiming Signature was closed down because “its customers were politically unpopular” and that “the FDIC all but confirmed it closed the bank over crypto.” In addition, Republican House leader Tom Emmer is questioning the FDIC’s recent actions stating the agency is “weaponizing the recent instability in the banking sector to purge legal crypto activity from the U.S.” And Jake Chervinsky, the Chief Policy Officer at the Blockchain Association sent FOIA requests to the Fed, FDIC, and OCC, demanding information about what he calls “the unlawful de-banking of crypto companies.”

But if there was any doubt that Signature was closed because of its ties to crypto, the FDIC’s next move all but confirmed it. Following the receivership, the FDIC began looking to sell Signature Bank but made it a condition that the buyer must not take on Signature’s crypto related accounts nor operate Signet, the bank’s crypto transfer network. David French wrote for Reuters that his sources confirmed “any buyer of Signature must agree to give up all the crypto business at the bank.” If true, the FDIC broke the law because when the FDIC takes receivership of an entity, they become a fiduciary to all stakeholders including shareholders and debt holders. That means they have a legal obligation to maximize the value of the assets. The crypto deposits were worth billions of dollars and Signet gives any acquiring bank an enormous competitive advantage in the market as one of the only bank-controlled fiat to crypto rails still operational. Not including these assets in a sale objectively does not maximize the value for shareholders.

On March 20, the FDIC did in fact sell Signature to Flagstar Bank and lo and behold, none of the crypto deposits or Signet were included in the sale. Flagstar left billions of dollars’ worth of deposits held by Signature Bank’s digital assets business on the table. Nor did Flagstar acquire Signet. Again, why wouldn’t FDIC or Flagstar want to include these given their value? Even if Flagstar didn’t want the crypto business for some reason, there have reportedly been other bidders for Signet and Signature’s crypto deposit base which the FDIC has refused to sell. Unless of course, the FDIC’s motivation all along had nothing to do with Signature’s financial health or the value of the bank and Signature was shut down solely to cut off another bridge between crypto and the traditional banking system.

Though regulators have publicly denied it, it appears that regulatory agencies stepped in and took control of a financially stable, private, regulated company in an effort to impose a political agenda. The bank crisis of SVB and First Republic provided an opportunity and excuse to take down the second and last remaining crypto bank. You can bet there will be investigations launched and lawsuits filed because if that is in fact what happened, the NYDFS and FDIC broke the law. It’s not the job of unelected bank regulators to determine which industries should and shouldn’t have access to banking. In fact, it’s illegal to systematically prevent any legal industry from accessing banking services.

Washington D.C. law firm Cooper & Kirk, the same firm that successfully sued the FDIC, Federal Reserve, and OCC over the original Operation Choke Point, released a white paper that details evidence that federal regulators have once again gone far beyond their statutory authority, handed out enforcement actions without due process and committed Administrative Procedures Act violations. It’s a shame our regulatory agencies have resorted to this approach causing companies to shut down operations in the US while jurisdictions in other countries are embracing crypto companies and banks.

Toss a Coin into the wells

On March 22, 2023, Coinbase received a “Wells Notice” from the SEC. A Wells Notice is a formal communication from the SEC that the agency is planning on bringing enforcement action against the recipient but hasn’t officially done so yet. It’s like when you were young, and your mom was threatening you in the car that you are going to be in big trouble when you get home. The purpose of a Wells Notice is to alert the recipient to the violations that the SEC believes the accused party committed. It also provides the accused party an opportunity to publicly make a case as to why such an action shouldn’t be brought and oh boy, did Coinbase respond.

Coinbase’s Chief Legal Counsel Paul Grewal published a response later that same day in which he listed numerous reasons the SEC has not operated in good faith and how Coinbase is looking forward to arguing the case in court. Grewal started with the fact that the regulator’s accusation against Coinbase was extremely vague in describing what exactly Coinbase has done wrong. The notice doesn’t address which products (Coinbase Exchange, Coinbase’s staking service, Coinbase Earn, Coinbase Prime, and/or Coinbase Wallet) violated securities laws leaving the company to have to guess what exactly they have to defend themselves against.

Grewal also laid out numerous examples of Coinbase’s attempts to work with the SEC over the years and yet never received any guidance, clarity, or rules from the agency. According to Grewal, Coinbase met with the SEC many times over the past several years including “more than 30 times over nine months” prior to the Wells Notice being issued. In those meetings, Coinbase repeatedly asked the SEC to identify which assets on the exchange they believed to be securities so that Coinbase could understand what criteria the SEC was using. Instead, the SEC routinely declined to answer. When the SEC asked Coinbase to provide its views on what a registration process could look like because there is no way for a crypto exchange to register today, Coinbase spent millions of dollars drafting proposals for the SEC which the SEC promptly ignored. Last July, Coinbase filed a petition for rulemaking as well as additional comment letters to the SEC in regards to many unresolved issues facing the crypto industry. The SEC never responded. Every time Coinbase, or any crypto company for that matter, has attempted to work with the SEC to establish reasonable rules by which companies could operate inside a regulatory framework, provide investors and consumers the info they need while still accommodating the unique elements of cryptoassets, the SEC has refused to engage. Rather than provide a clear set of rules for the industry, Gary Gensler has continuously chosen to bring enforcement actions not designed to protect consumers, but in an attempt to expand the scope of the agency’s authority.

Grewal also raised the point that the SEC’s own actions are contradictory. Coinbase is a publicly traded company which means back in 2021, the company had to file an S-1 with the SEC. Coinbase’s business, including the assets listed on its exchange and its staking service, are largely unchanged since the SEC first reviewed and approved Coinbase to go public. In fact, the “staking service was referenced 57 times in the S-1 the SEC reviewed in 2021” when Coinbase became a public company. If any accusations made by the SEC now predate Coinbase’s IPO, why on earth did the SEC approve Coinbase to go public if it was violating securities laws? Retroactively and arbitrarily changing your mind for what is and isn’t allowed is not an acceptable basis for regulatory action. Even the courts are beginning to question the SEC’s inconsistent positions.

Grewal also argues that the SEC isn’t the only regulator Coinbase is potentially beholden to, but other regulators have publicly communicated contradictory positions to the SEC. The CFTC Commissioner has said that “the SEC has no authority over pure commodities or their trading venues, whether those commodities are wheat, gold, oil…or crypto assets.” Whereas SEC Chair Gary Gensler has publicly claimed every cryptoasset but bitcoin is a security, the Chair of the CFTC recently testified to Congress that Ethereum and other cryptoassets are commodities. In our current regulatory environment, it’s possible a company like Coinbase could attempt to adhere to regulations from one entity only to break the rules of another. If our regulators cannot agree on who regulates which aspects of crypto, how on earth are companies expected to know how to operate?

The truth is that today there is no clear rule book from the SEC on crypto, and all efforts from the industry to engage with the SEC have been met with silence or enforcement actions. They have not acted in good faith when it comes to crypto. The SEC has opportunistically stepped up their enforcement in areas identified as regulatory gaps for digital assets as an attempt to expand their power. According to a report from The Block, multiple people close to the SEC have said that Gary Gensler has actively worked to prevent any new laws from filling those gaps because it would undermine his efforts.

The only difference now is that Coinbase is willing and able to fight the SEC. This is existential to their business and Coinbase is one of the few crypto entities well-capitalized enough to take on the regulators. As Grewal tweeted, the case will provide an opportunity to publicly debate the application of the Howey and Reves test to cryptoassets. It’s possible this case could lead to legal precedent for determining when an asset is decentralized enough to exempt it from being “solely dependent on efforts of others” as well as other key concepts regarding the classification of cryptoassets. With Coinbase intent on meeting the SEC in court, it’s very likely we may finally get legal clarity one way or the other.

“Tell us the rules and we will follow them. Give us an actual path to register, and we will register the parts of our business that need registering. In the meantime, the U.S. cannot afford for regulators to continue to threaten the good actors in the crypto industry for doing the same legal and compliant things they’ve always done. This unfair approach will only drive innovation, jobs, and the entire industry overseas.”

– Paul Grewal, Chief Legal Officer at Coinbase

CFTC’s lawsuit against Binance may not even be about Binance

On March 27th, the CFTC filed a lawsuit against Binance for numerous commodity regulation violations including operating a derivatives trading operation in the US without registering with the CFTC, actively helping customers skirt Know Your Customer (KYC), Anti-Money Laundering (AML) and other compliance rules, knowingly facilitating illegal transactions, faking compliance audits, and trading against their own customers using more than 300 in house accounts. Investigators apparently got hold of internal Binance communications (exactly how still remains a mystery), including internal messages from CZ’s own cell phone which revealed that Binance’s executives were allegedly aware its geofencing tools were inadequate, and even had procedures for assisting large accounts to get around it.

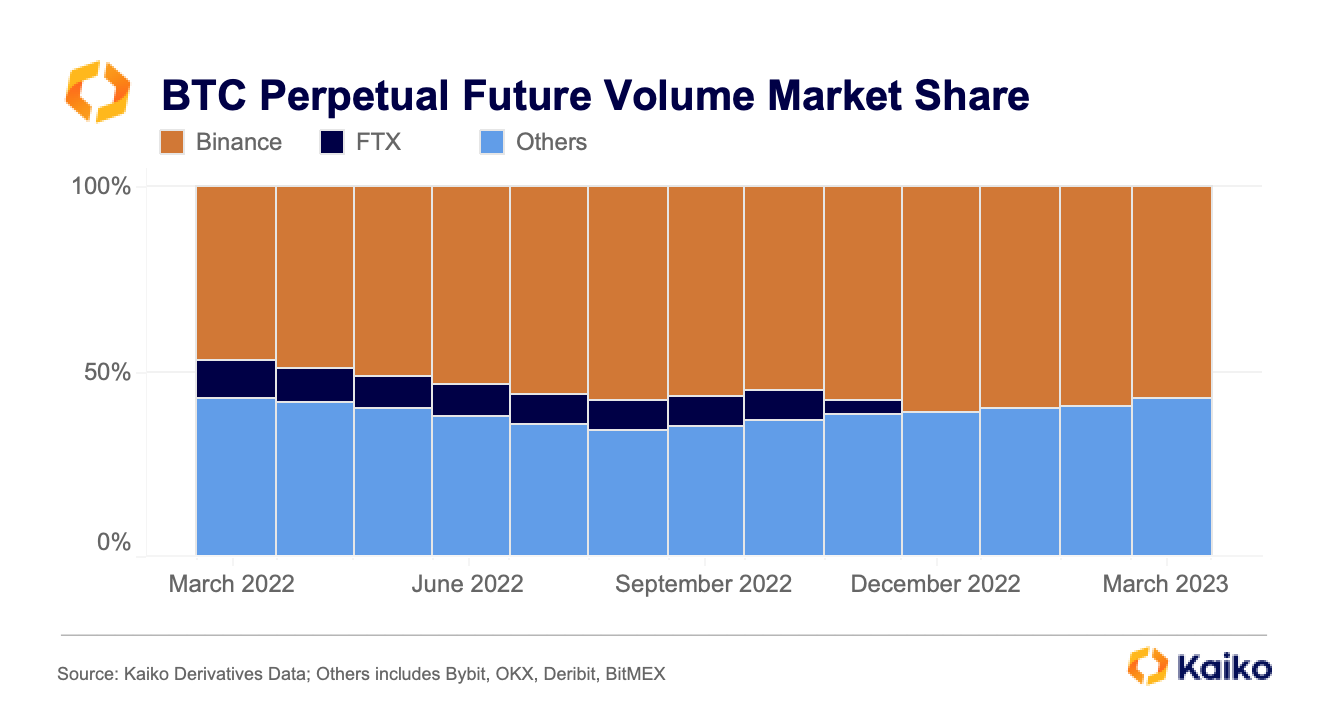

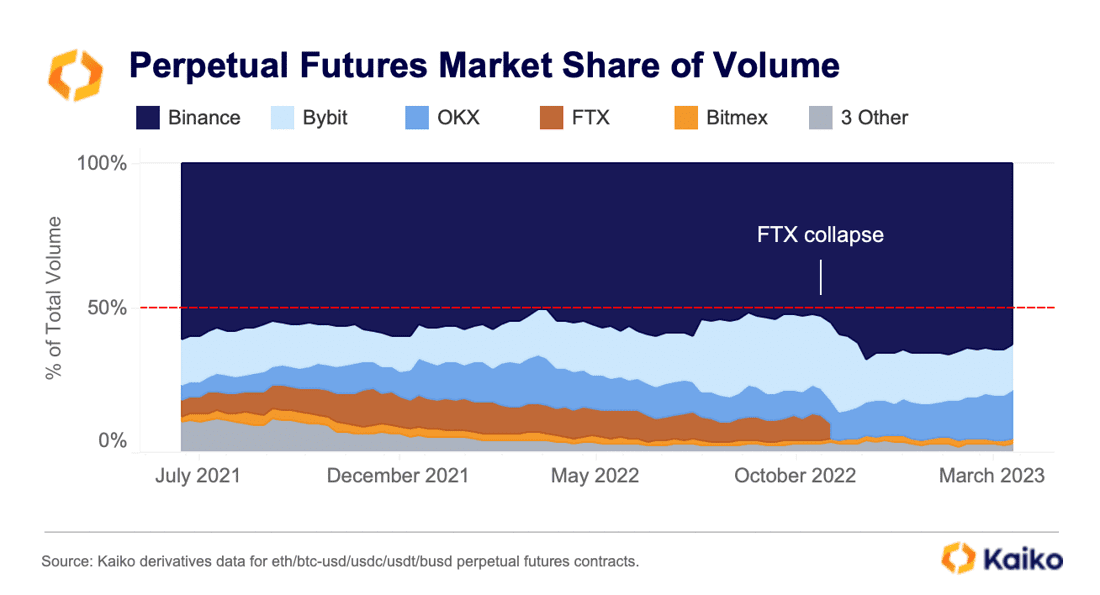

Binance is by far the world’s largest crypto exchange. The exchange has 90 million customers worldwide and peaked at 70% market share earlier this year. Part of the reason for its dominance is that due to US regulations, US based exchanges such as Coinbase, Kraken, and Gemini can’t offer the same suite of financial products, such as derivatives, that offshore exchanges can. As a result, investors have limited choices on where to trade crypto derivatives which are used to employ more sophisticated trading strategies including the ability to short various assets. The combination of significant volumes and the most instruments available allowed Binance to dominate the derivative market for years. With the fall of FTX last year, Binance has increased its market share to the point where it now processes the majority of all bitcoin perpetual futures volume.

Source: https://marketing.kaiko.com/cftc-v.-binance

Thus, the CFTC lawsuit is potentially a big deal for the crypto industry but what this lawsuit exactly means for Binance is a topic of much conversation. The CFTC doesn’t have the power to bring criminal charges to Binance or its executives, but it does have the power to shut down Binance’s operations in the US. Hence, it’s likely to lead to Binance US (the US arm of the organization) being shut down. Some have theorized it could lead to a significant drop in market share for Binance. However, the data has yet to support that theory. Although Binance appears to have recently lost 16% of its trading volume, Binance only lost about 2% of market share for perpetual futures trade volume following the CFTC’s announcement. This suggests that any recent decrease in spot market volumes on Binance had more to do with the exchange ending their zero-fee spot trading, rather than trepidations about the CFTC lawsuit.

Source:https://blog.kaiko.com/binance-market-share-tumbles-16-fcb6d1dce7fe

Bloomberg’s Matt Levine posed a different theory in which he argued that the case is not centered on consumer safety but is mostly about preventing an international exchange from making money off big market-making firms based in the US. I think Matt is correct in his assessment but there is potentially an even more interesting, wider reaching implication of the CFTC’s lawsuit.

The CFTC is alleging that Binance operated a derivative trading operation in the U.S. and specifically named bitcoin (BTC), ether (ETH), litecoin (LTC), tether (USDT) and Binance USD (BUSD) as commodities. If these assets were considered securities, the CFTC would have no jurisdiction and thus no lawsuit. In order for the CFTC to even litigate this case, let alone win it, it must first establish that the CFTC has jurisdiction which means establishing legal precedent that these aforementioned assets are commodities.

It’s possible the ultimate goal of this lawsuit might not even be about Binance at all. By going through a federal court rather than waiting for Congress to pass a bill, the CFTC might be looking to establish legal precedent for cryptoassets being considered commodities rather than securities. This is in direct contradiction to the SEC’s claim that all crytpoassets other than bitcoin are securities and thus Gary Gensler believes the SEC has authority over this asset class. The CFTC is saying the activity Binance engaged in for this set of tokens, and possibly other assets in the future, falls under the CFTC’s jurisdiction alone and therefore the CFTC is the only agency in charge of regulating.

Assuming no party challenges this assumption, the CFTC gains jurisdiction by default. In theory Binance could argue these assets are securities (not sure why they would as that would just bring potentially more legal action from the SEC) or the SEC could intervene to argue against the CFTC (though it would be highly unusual for one federal regulator to argue against another federal regulator in federal court). Should the CFTC’s claims stand, this means in the future, if the CFTC wanted to assert regulatory authority there is legal precedent for them to do so but if the SEC were to try and bring enforcement actions, its likely they would have to contest the precedent that is being set before even being able to enforce any action.

By suing Binance, the CFTC is forcing a judge to decide if these assets are commodities or securities and thus who has regulatory oversight. The lawsuit is directed at Binance, but the second order effects that emerge from this lawsuit could have much bigger implications for the regulatory environment of crypto within the US moving forward.

In Other News

Banks step up to serve crypto firms after Signature and Silvergate wound down.

Crypto venture firm Paradigm published an article arguing there is not a path to registering crypto assets as securities in the United States and thus, securities regulators are exercising muscle beyond their statutory authority.

Binance is being sued by the CFTC for allegedly violating federal laws and not registering the exchange in the U.S.

Bitcoin, the perfect option.

Gemini is looking to launch an overseas derivatives exchange.

Ethereum developers announced the Shanghai upgrade is now scheduled for April 12th.

It sure looks like the U.S. is trying to kill crypto.

A National Defense Fellow at MIT is proposing the U.S. to stockpile bitcoin, build a domestic Bitcoin mining industry, and extend legal protections to the technology.

Crypto exchange Bittrex is winding down their U.S. operations due to an uncertain regulatory and economic environment in the U.S.

PostFinance, the financial services firm fully owned by the Swiss government, is rolling out bitcoin and ethereum services for clients.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS