By Brett Munster

Over the last couple of years, the SEC has taken a very deliberate, methodical approach to cracking down on the crypto industry. It appears the agency started with cases it either knew it could win or went after companies without the resources to fight back knowing they would likely settle quickly (Ether Delta in 2018). They built on the precedent set with those smaller cases to go after bigger fish (Bitrex and Beaxy). Rinse and repeat up the chain (Ripple and Kraken). It now seems that last week was the culmination of the SEC’s multi-year crusade against the crypto industry when the agency announced a pair of lawsuits against Coinbase, the largest US exchange, and Binance, the world’s largest crypto exchange.

The truth is, neither was a surprise. The SEC had issued a Wells Notice to Coinbase and it had been known for months the SEC was investigating Binance. In March, the agency even told the federal court overseeing the bankruptcy of Voyager that they believed Binance was operating an unregistered securities exchange in the U.S. Both Coinbase and Binance expected these lawsuits and are well prepared for them. These two cases, along with the Ripple lawsuit that is likely to be settled in the next few months, should be landmark cases for the industry. Let’s dig into exactly what the SEC is alleging in both lawsuits, the similarities and differences between the two, and what this means for the crypto industry moving forward.

The SEC’s Lawsuit Against Coinbase

Back in March, the SEC issued a Wells Notice to Coinbase which is a fancy way of saying the SEC alerted Coinbase that they intend to sue the company. Thus, it was a matter of “when” not “if”, the SEC was going to file its complaint against Coinbase. That lawsuit was officially filed on June 6th and now we finally know what the SEC is accusing Coinbase of.

The core of the SEC’s complaint is that it believes Coinbase operated an unregistered exchange and offered the sale of unregistered securities. The problem with this charge, as we have covered in previous newsletters and is glaringly missing from the filling, is that there is no viable path to register as a crypto exchange in the U.S. Coinbase met with the SEC more than 30 times in the past year precisely with the intent on seeking a cooperative resolution. So too did Kraken, Gemini, and probably every other major exchange that has operated in the U.S. at one time. Even Robinhood’s compliance chief Dan Gallagher testified in front of Congress last week that Robinhood tried for 16 months to register but couldn’t get the SEC to guide Robinhood into compliance. Dan Gallagher is a former SEC commissioner who spent his entire career in securities law, and he claims that “there is no path” to do so.

Coinbase has over 89 million verified users. That’s more than Charles Schwab and Fidelity combined. Instead of working constructively with U.S. based exchanges to come up with a workable model for a product with clear demand from American consumers, the SEC has opted to accuse Coinbase of failing to do the impossible. It’s like a parent punishing a child for not eating his vegetables at dinner even though the dinner served had no vegetables in the first place.

Nor has there been clarity from the SEC regarding which assets are securities and which aren’t. If we only had a framework to classify cryptoassets based on their characteristics like Europe now has, the exchanges would simply not list the ones deemed securities. But the SEC has refused to provide that framework despite being asked repeatedly for many years. It’s disingenuous for the SEC to bring legal action against companies for doing something in which that same agency refuses to provide any legal guidance on.

In order to back up its claim that Coinbase offers unregistered securities, the SEC identified 13 tokens it all of a sudden decided met the definition of a security. The most notable of which include Solana (SOL), Cardano (ADA), Polygon (MATIC), and Filecoin (FIL). This is the first time the SEC has ever made public comments on any of these tokens and the lawsuit is sparse on details as to exactly why these assets, and not others, are viewed as securities in the eyes of the SEC. Rather than issue formal guidance about which assets the agency deems securities, explain what criteria the SEC used to come to that conclusion, and ask the exchanges to delist those assets, the SEC has chosen to skip all that and go straight to enforcement actions.

Why would the SEC take this approach? Because including these tokens in a lawsuit allows the SEC to make the claim that these assets are securities without letting those projects defend themselves. That’s right, claiming SOL is a security in a lawsuit against Coinbase means the team behind Solana is not actually a defendant in the case and thus will not have an opportunity to defend itself in court. Instead, Solana and others must rely on Coinbase to argue the SEC on their behalf. It’s not clear the SEC could win a straightforward legal case against many of these assets (as evidenced by the Ripple case) and thus has instead found a backdoor to achieve the same ends. By the way, there are multiple organizations now looking into whether this behavior by the SEC is even legal or if it’s a violation of the Administrative Procedures Act. Stay tuned.

The SEC also singled out Coinbase’s staking product as an investment contract that Coinbase failed to register. We covered staking products back in March when the SEC went after Kraken’s staking service which ended in a $30 million settlement. To quickly recap, Coinbase helps individuals who wish to stake their ETH, or other proof-of-stake tokens, by allowing them to pool assets with other customers and taking on the technologically complex process of running a validator node. In Kraken’s case, the SEC took issue with the fact that Kraken was the one setting the reward payout for the staking service rather than simply passing through staking rewards to customers. However, in this lawsuit against Coinbase, the SEC is now claiming that even simply passing any rewards directly back to the customers qualifies as a security. Given the structure of Coinbase’s staking service, it’s going to be tough for the SEC to prove it meets the definition of a security in court.

It’s also very short sighted. As we saw with Kraken, forcing Coinbase to shut down their staking service will not reduce the demand from market participants wanting to stake their assets. They will simply use other services including DeFi and offshore companies. Furthermore, this move only benefits large institutional investors at the expense of smaller retail investors by making it more difficult for retail users to participate in staking. By going after Coinbase’s staking product, the SEC is prioritizing large investors over retail users and forcing retail users to take their assets out of an American company and put it in far less regulated services. Should the SEC win this case, the end result goes completely against the mandate of the SEC. Fortunately, Coinbase CEO Brian Armstrong said Coinbase will not shut down its staking service until after this lawsuit is settled.

Finally, the last claim made by the SEC in its lawsuit has to do with Coinbase’s Wallet product. According to the SEC, Coinbase is offering unregistered brokerage services via its non-custodial wallet. “Non-custodial” means that the user owns and controls the assets in the wallet, not Coinbase. This is not a banking service in which banks take custody over the funds in a bank account. Coinbase’s wallet leaves all control and all custody with the user.

So why does this matter? Because this is a brand-new argument by the SEC, one that has never been asserted in any court of law previously. What the SEC is claiming is that because the wallet can interact with services outside of Coinbase and those services outside of Coinbase potentially could offer unregistered securities, the software product is somehow providing unregistered brokerage services. According to this theory, if you have a Coinbase, Metamask, Ledger, Trezor, or any other wallet that connects to any services that exchanges cryptoassets, you are operating an unregistered broker dealer and are in violation of securities law. Guess I should be expecting my own Wells Notice from the SEC any day now.

This Wallet complaint isn’t about Coinbase as evidenced by the fact it directly refers to using the wallet outside of Coinbase. This is about the SEC positioning themselves to go after DeFi and using this lawsuit to establish precedent for later court cases. Rather than operating in good faith and addressing the issues of DeFi head on, Gensler continues to find backdoor ways to expand the power of his agency.

And that’s not even the craziest part of this lawsuit. The SEC used risk disclosures from Coinbase’s S-1 registration (the document companies file when they go public) as evidence against Coinbase. Here is the problem, the agency you file the S-1 document with is the SEC. Think about that for a minute. The SEC is using disclosures from a document the SEC itself approved as evidence of wrongdoing against Coinbase! And it’s not as though the SEC didn’t know at the time. The same assets listed by the SEC in the lawsuit were trading on Coinbase prior to them going public. The staking service was live 2 years prior to Coinbase filing its S-1. If that isn’t the SEC acting in bad faith, I don’t know what is.

And to complicate matters further, don’t forget that Coinbase sued the SEC first. The U.S. Court of Appeals for the Third Circuit has given the SEC seven days to clarify its position on a rulemaking petition from Coinbase. It will be interesting to see how this development impacts the SEC’s lawsuit going forward.

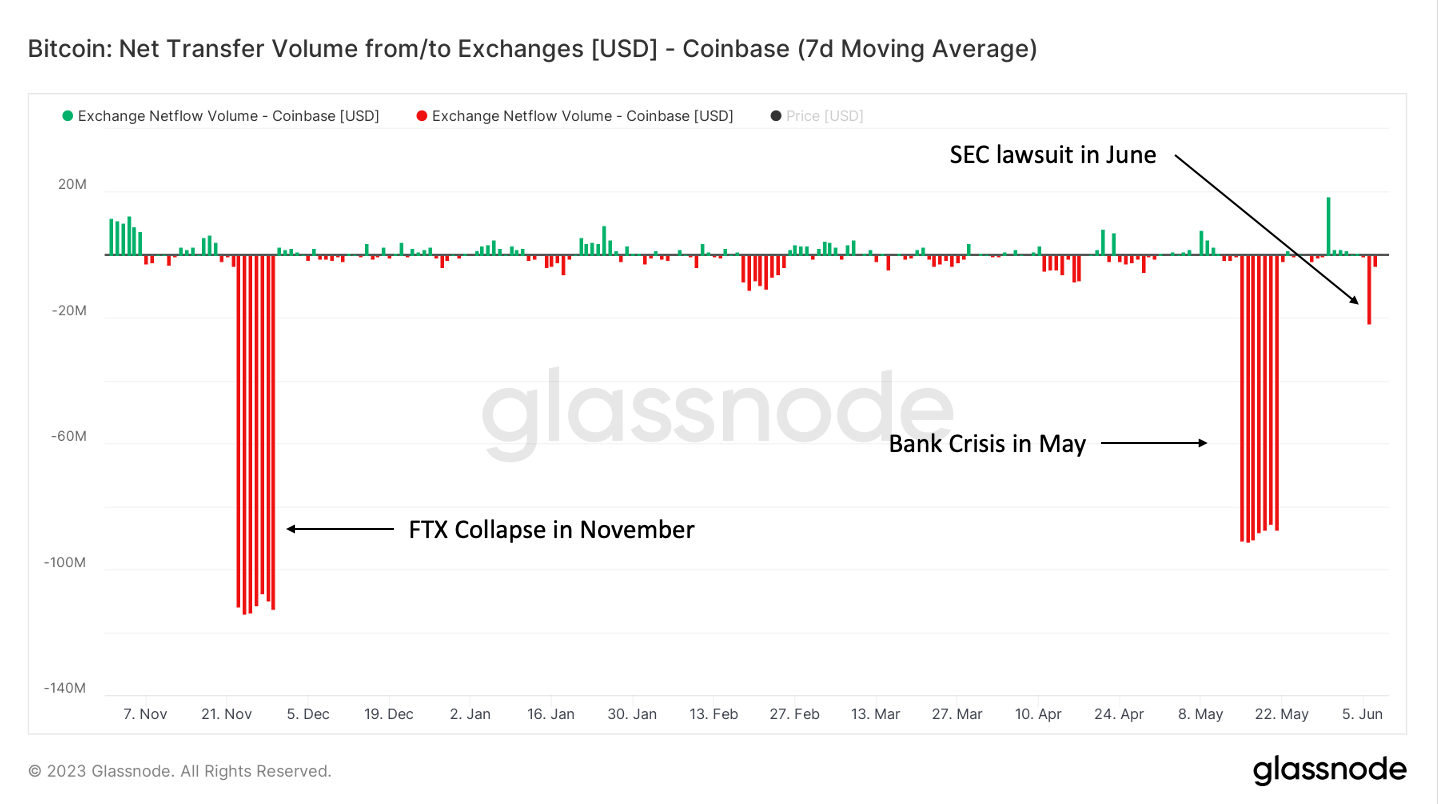

Coinbase customers don’t seem to be too phased about the lawsuit, however. Coinbase did see some initial withdrawals off the platform in the first 24 hours after the news broke but it was pretty minor especially compared to FTX last November and even the banking crisis earlier this year. In fact, net flows turned positive (more assets being deposited onto Coinbase than taken out) within just a couple days of the announcement. It’s basically business as usual for most Coinbase customers. I think this says a lot about the trust in Coinbase vs the credibility of the SEC at this point.

Source: Glassnode

The SEC’s Lawsuit Against Binance

The day before its action against Coinbase, the SEC announced it was filing a lawsuit against Binance, the largest crypto exchange in the world. There are a lot of similarities to the Coinbase lawsuit but some key, notable differences as well. Let’s start with the similarities.

The first claim from the SEC is that Binance knowingly operated an unregistered exchange and unregistered sale of securities. Binance allows users to buy and sell over 350 different crypto assets. Assuming at least some assets available on the Binance exchange should be classified as securities, Binance would be in violation of this law. I don’t think you will find many people who would argue otherwise. The problem with this charge, is the same problem in the Coinbase lawsuit: there is no viable path to register as a crypto exchange in the U.S. nor is there a framework for determining which assets are and are not securities. Just like Coinbase, Binance has met with the SEC in the past to try and find a solution, which the SEC is clearly uninterested in doing. This is the same disingenuous claim the SEC made against Coinbase.

The SEC also identified additional assets as securities beyond what they named in the Coinbase lawsuit. The securities identified include SOL, ADA, MATIC, FIL, ATOM, SAND, MANA, ALGO, AXS, and COTI. Again, this is literally the first time the SEC has ever made public comments on any of these tokens. And like the Coinbase lawsuit, this approach prevents each of these projects from defending themselves in court and forces them to rely on Binance to argue the SEC on their behalf. But the rationale for including these assets goes a step further with regards to Binance than it does with Coinbase.

Back in March, the CFTC filed a lawsuit against Binance, which we argued was likely more about establishing legal precedent that the assets listed on the exchange were commodities, and thus fell under the jurisdiction of the CFTC. Gary Gensler is not about to stand by and let that happen. If the CFTC wins its lawsuit, it basically negates Gensler’s claim that Binance and Coinbase are operating unregistered securities exchanges. They can’t be an unregistered securities exchange if all the assets are deemed commodities. Thus, the SEC had to file its own lawsuit against Binance otherwise the agency would risk ceding control to the CFTC. In fact, the SEC’s lawsuit is mostly a mirror image of the CFTC lawsuit against Binance in its allegations. The only major difference is the SEC says Binance was running an unregistered securities exchange whereas the CFTC claims Binance was running an unregistered derivatives exchange.

That might explain why Gary Gensler decided to share the lawsuit with the media BEFORE serving it to Binance. A government agency, whose job is to enact impartial regulation, would not be engaging in such games unless it had an ulterior motive. It’s likely this lawsuit is as much about the SEC’s turf war with CFTC as it is about Binance.

Just like the lawsuit against Coinbase, the SEC also claims that Binance’s staking product is a security. Binance structured its staking product similar to Coinbase in which it passes the rewards directly to the user rather than setting the payout. For the same reasons as in the Coinbase lawsuit, the SEC is likely to struggle to prove that this product is a security in court.

But that’s where the similarities between the two lawsuits end. Unlike the Coinbase lawsuit, the SEC made further allocations against Binance beyond the standard unregistered exchange infraction. One thing the SEC claims is that there was no real separation between Binance Global and Binance U.S. See, Binance actually has two exchanges. The company has its normal exchange, which most of the world uses, and then it has a watered-down version for U.S. customers. Due to U.S. laws, U.S. retail customers are not allowed to access Binance’s main product because the main exchange has features the U.S. government has deemed too risky for U.S. consumers. In order for Binance to serve the U.S. market, it had to create a second company which is supposed to operate independently and restrict various features such as derivatives. To be clear, there is nothing illegal about this type of structure so long as the US entity remains independent.

In the lawsuit, the SEC alleges Binance only pretended that the international platform and the U.S. arm were operated separately, when in reality they were both fully controlled by CEO Changpeng Zhao (aka CZ). According to the SEC, the creation of the U.S. entity was merely for regulatory appeasement and the company actively helped U.S. customers get around the restrictions through the use of VPNs and shell companies. The lawsuit alleges that any attempts to prevent U.S. customers from trading on Binance’s international exchange were solely “for show.”

The SEC also has detailed accounts from two former Binance US CEOs who are unnamed, but everyone is pretty sure they are Catherine Coley (aka “CEO A”) and Brian Brooks (aka “CEO B”). I mean, the list of former CEOs of Binance U.S. is pretty short after all. The former CEOs told the SEC about being “strong armed” by CZ, having asset transfers within their company conducted without their knowledge, and leaving once it was evident that they were not in charge. It’s long been speculated that there was very little separation between Binance Global and Binance U.S. and it’s likely the SEC has Binance dead to rights on this one. Intermingling of the international and U.S. entities opens up Binance Global, not just the U.S. based entity, to enforcement action from the SEC.

The lawsuit also alleges that Binance engaged in wash trading. Wash trading is an illegal activity in which an entity buys and sells the same security in order to generate misleading market information. The SEC claims to have evidence that a hedge fund called Sigma Chain engaged in wash trading from at least September 2019 until June 2022, which artificially inflated the trading volume on Binance. This made it look like Binance had more volume than it really did and made it look like certain assets were more popular than they really were. For example, Sigma Chain supposedly accounted for about 35% of all trading volume in the first 11 days that some tokens were listed. And it turns out that Sigma Chain was owned and controlled by Binance CEO CZ.

The last and the most concerning claim, is that Binance commingled customer assets. While the SEC is not alleging insolvency, they are accusing Binance of diverting billions of dollars to an entity controlled by CZ called Merit Peak as well as using customer funds for personal expenditures. Predictably, Binance denied the SEC’s allegations in a blog post, specifically stating that customer funds were never at risk. While it’s hard to know how true this is, it’s an extremely serious allegation.

That’s everything the SEC is accusing Binance of doing. The document leaves plenty of blame to go around, starting with Binance and CZ. It appears that there is ample evidence between the SEC’s and the CFTC’s lawsuit to suggest that Binance purposely and knowingly skirted just about every compliance rule in the book. It was only a matter of time until regulators, who have been investigating Binance for years, cracked down hard on the company. Even if Binance, unlike FTX, didn’t lose any of its customers’ money, it’s inexcusable behavior from one of the largest companies in the industry. The entities should have operated separately and adhered to basic compliance standards. CZ should never have had a hedge fund trading on the platform let alone engaging in wash trading. And the company surely should not have touched any customer funds (if in fact that’s true).

If Binance did engage in wash trading and comingling of assets, then the SEC should go after the company. That’s exactly the kind of behavior the agency is there to protect against. Had the complaint just been about those activities, then I don’t think anyone would have much issue with the SEC’s lawsuit. In fact I would applaud the SEC in that regard (never mind they failed to go after FTX even though Gensler met with SBF multiple times before the exchange collapsed or recent reports that Gensler once asked to be an advisor to Binance). But arbitrarily declaring tokens securities, bringing down enforcement action for being an unregistered exchange when the SEC has actively prevented any exchange from registering, and using this lawsuit as a backdoor way to keep up with the CFTC in their turf war is not acceptable behavior either. Even though the SEC apparently had evidence regarding the company’s deceptions, that wasn’t enough for Gensler. He still had to use the complaint as a vehicle to seek to expand his power.

Though Binance has vowed to defend itself vigorously, given both the CFTC and SEC lawsuits, it’s very likely Binance will have to pay an enormous fine and possibly leave the US market altogether (either by choice or by being forced to shut down Binance U.S.). However, the lawsuit from the SEC is a civil matter that can’t result in jail time or criminal penalties. It’s also unlikely the SEC has the power to shut down Binance’s global operations meaning its primary exchange, the core of its business, will continue on uninterrupted. Even if Binance can’t operate in the U.S., it’s still the largest exchange in the world with the most liquidity. All of the assets that the SEC is alleging are securities will continue to trade freely on Binance Global and decentralized exchanges even though U.S. citizens won’t have access. Despite what it seems is the government’s best effort, Binance and the crypto economy will continue chugging along.

Other Thoughts and Reactions

First, it’s worth remembering that everything in the SEC lawsuits are allegations. The SEC still must prove its case in court overseen by a federal judge. Gensler can’t just rely on making comments to the press or avoid answering questions he doesn’t want to answer. He has to prove his case to a neutral third party. It finally gives the industry an avenue to push back on the SEC’s claims and whether or not the SEC has followed the law with its campaign of regulation through enforcement. That being said, these cases are likely to take years to play out. Bloomberg estimates that the earliest possible summary judgment could occur in 2025 and trial in 2026. Appeals are certain to drag this out longer. Both companies are very well capitalized and have the ability to fight this as long as they want to.

Second, the SEC has a stronger case against Binance than it does Coinbase. Both lawsuits claim the companies have operated unregistered exchanges, facilitated the sale of unregistered securities, and offered staking products which the SEC views as unregistered securities. It’s not clear that the SEC can win these arguments, especially given how badly the SEC has been grilled by judges in the past during the Voyager case and Grayscale hearings. Whereas the lawsuit against Coinbase stops there, the Binance lawsuit contains additional allegations of wash trading and commingling of assets. It’s these additional allegations in which the evidence from the SEC (and the CFTC for that matter) appear much stronger. In other words, Binance’s legal troubles are in a category above Coinbase.

Third, the SEC’s concerted efforts to stifle a broad range of actors across the crypto industry is a uniquely American approach. Europe, Singapore, Hong Kong, the Middle East, Brazil, Bahamas, Switzerland, and others are all passing regulations designed to provide clarity and promote the use of crypto. In those jurisdictions, regulators have taken a collaborative approach to crafting new rules. The regulating bodies throughout the rest of the world largely do not share the SEC’s view. While it’s easy to get caught up in what is happening in the U.S., it’s important to realize the industry is flourishing in other parts of the world, from Europe to Asia to Africa to the Middle East. Regardless of the SEC’s actions, crypto and DeFi are here to stay.

Nor do many within Congress agree with the SEC’s approach. In past congressional hearings numerous congressmen expressed concerns that many of the recent actions by the SEC are an overreach of jurisdictional authority. Even within the SEC there isn’t full alignment, as Hester Pierce has routinely issued dissenting letters against the actions of her own agency. Now there is a growing sense in Congress and among former regulators that Gary Gensler is undermining congressional efforts. Representative Ritchie Torres said “the latest enforcement action against Coinbase is an egregious example of regulation by enforcement. It demonstrates a complete contempt for Congress which is in the process of developing a framework” for crypto regulation. It’s possible that these two lawsuits might actually increase the urgency from Congress and help expedite the passing of a workable framework, including bills such as the draft legislation recently put forth by the House Financial Services Commission, that would give crypto exchanges a path to register and framework for the industry within the U.S.

I know in the moment, government actions like the ones we saw last week can cause a lot of uncertainty. But this isn’t the first time we have seen governments go after crypto. China outright banned the asset class a couple years ago. Today, usage is larger than ever. And there are several other examples just like that one. In every case, the value of decentralization has proven its resilience and the networks have grown stronger. Top-down actions only strengthen the case for self-sovereignty and independent access to financial services. This time will be no different.

In Other News

Volcano Energy announced $1 billion in commitments to build a bitcoin mine powered by clean energy in El Salvador.

The Howey test is supposed to determine which cryptocurrencies are securities, but the SEC could be relying on website screenshots instead.

Trading app Robinhood’s legal chief, Dan Gallagher, has announced that the firm started reviewing its crypto offerings which include several tokens in the SEC’s list of securities, such as SOL, ADA, and MATIC.

U.S. court ordered the SEC to respond to Coinbase’s rulemaking petition within a week.

The SEC is seeking a temporary restraining order to freeze Binance US assets.

U.S. Senators are asking the DOJ to investigate Binance for potentially lying to lawmakers.

Binance.US to halt all fiat withdrawals as early as June 13.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS