By Brett Munster

False alarm foreshadows what an ETF approval may look like

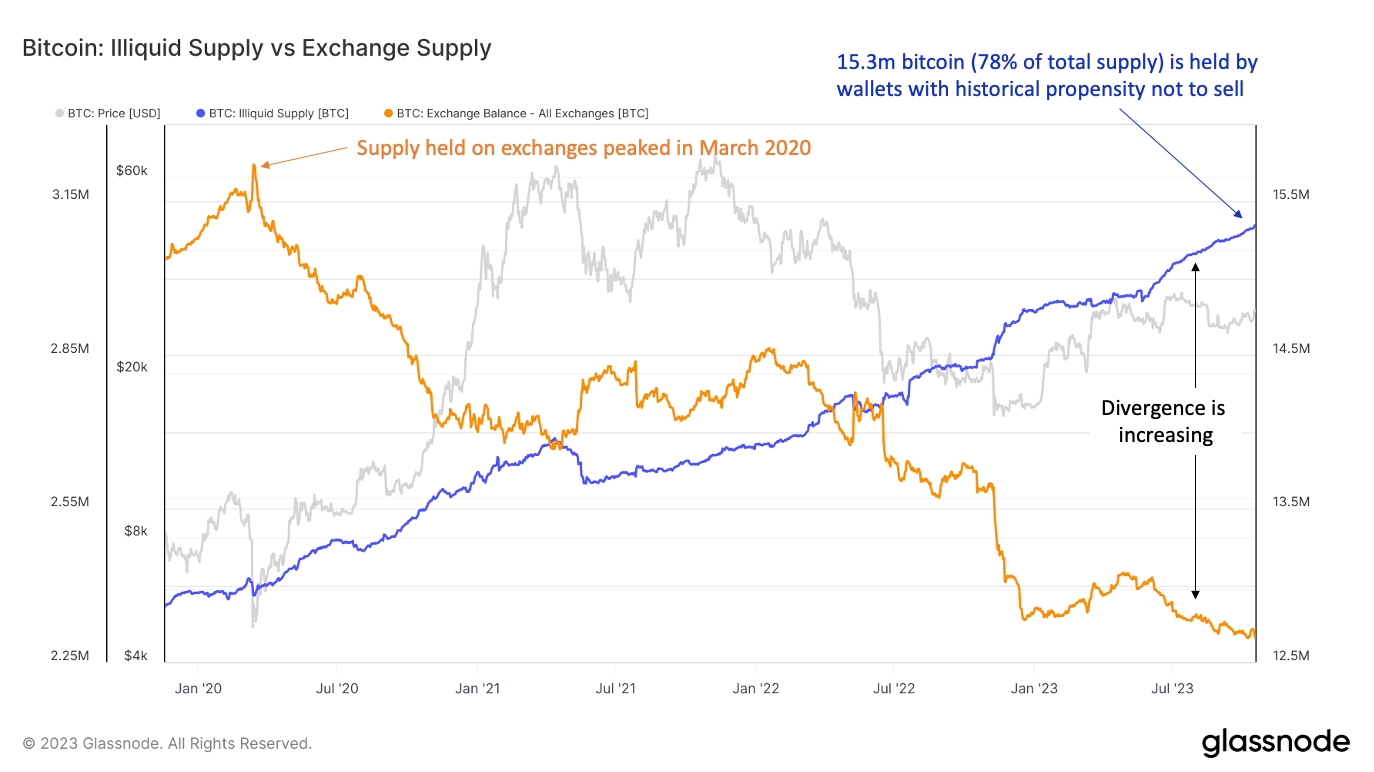

Since June of last year, we have been covering the ever-shrinking supply of bitcoin available to be traded on the market. On multiple occasions we have showcased how since the start of March 2020, the number of bitcoin held on exchanges has been on a steady decline as more and more market participants have taken their bitcoin off exchanges in favor of long term cold storage. We have also used on-chain data to highlight the fact that despite the price drop and blow ups of 2022, the number of coins that haven’t moved in over a year rose throughout last year. This indicates that an increasing percentage of bitcoin holders weren’t phased by price volatility and seem to have much longer-term expectations. That trend has only intensified this year as bitcoin has set all-time highs in coins that have not moved in at least one year and coins owned by wallets with a history of not selling.

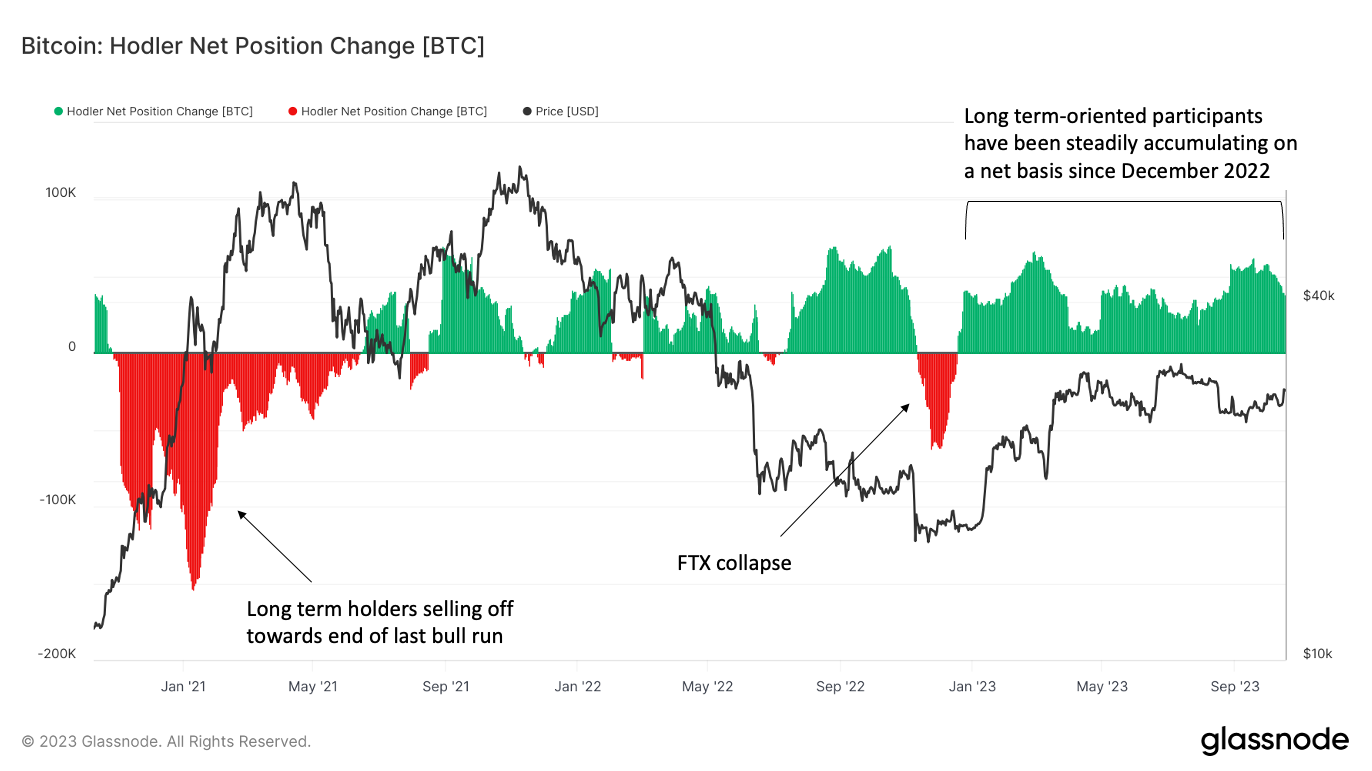

We can track this trend in another way. Hodler Net Position Change is a metric that shows the daily net position change from wallets identified as long-term holders (aka wallets that historically rarely, if ever, sell their bitcoin). When this metric is negative, it means long-term holders are cashing out of their position and selling their bitcoin back to the market. This has historically coincided with the tail end of a bull market when price has risen high enough for some participants to take some profits off the table. However, that is not what is happening now. Hodler Net Position Change has been positive since December of last year, the longest such streak since 2015. And other than a brief panic moment caused by FTX in November last year, Hodler Net Position Change has basically been positive dating back to July of 2022 meaning more and more supply continues to be gobbled up by long term-oriented market participants. The conviction of long-term oriented holders of bitcoin has arguably never been higher.

Why do I bring this back up? We are currently in the midst of one of, if not the largest supply squeezes in bitcoin’s history and just waiting for a demand driver to spark a big move up. Last week, we got a sneak preview of what that might look like.

On October 16th, crypto news publication Cointelegraph tweeted out that the SEC had approved BlackRock’s application for a Bitcoin ETF with an alleged screenshot from Bloomberg’s terminal. This tweet was debunked within 20 minutes, and ultimately taken down by Cointelegraph within the hour. However, in that short time frame, bitcoin’s price rose over 7%.

This event illustrated a couple things. First, the ETF approval is not priced into bitcoin’s current price. When it is approved, and it is a matter of “when” not “if” at this point, it’s very likely we will see bitcoin’s price spike. This past Monday there was a false announcement by a niche-media news outlet that was up on social media for less than an hour and bitcoin’s price still rose 7%. There weren’t even any real capital inflows into bitcoin and the price shot up. Some reports project we could see $24 – $50 billion flow into bitcoin when the ETF is approved. Imagine what happens if that amount of capital actually does start buying bitcoin via ETFs.

Second, the price rise is likely to be higher and faster than most people expect. The simple reason goes back to the beginning of this newsletter: there simply isn’t much supply to buy. If the supply shortage is the kindling, then any demand spark (which I would argue the ETF approval qualifies as) could ignite a larger price rally. Throw some gasoline onto that fire in the form of the Halvening which will occur in April 2024 and the next few quarters could catch a lot of people by surprise simply because of the supply squeeze that has been building up for over a year.

The significant rise in price we saw on Monday based on a rumor that circulated for all of 20 minutes is a sign of what may come when an ETF is approved for real. We don’t know exactly when the ETF will be approved. JP Morgan thinks it will be by January 10th but it’s very possible it could happen later in Q1 of 2024. What we do know, is that when it does get approved, bitcoin’s price is very likely to go up. And based on the current supply dynamics, it’s likely that when that move does come, it will be much bigger and much faster than most people are prepared for.

As always, the on-chain data is provided by Glassnode. If you would like to have access to the data yourself, you can sign up here: Glassnode Sign Up Link

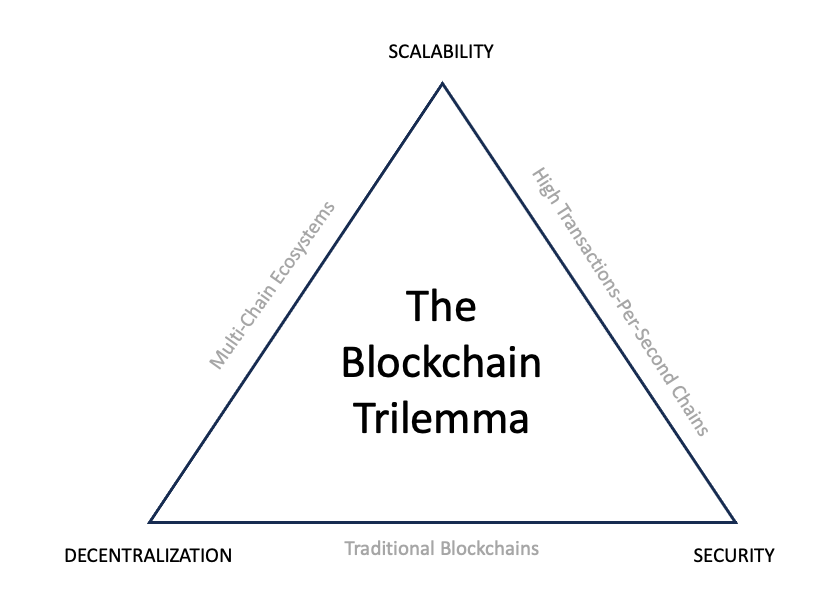

The Blockchain Trilemma

In the crypto ecosystem, there is a widely held belief that there are three core properties attributable to a base layer blockchain: decentralization, security, and scalability. The challenge, however, is that when designing a blockchain from scratch, it’s only possible to optimize for two out of the three properties. The concept of this tradeoff was first introduced by Vitalik Buterin, founder of Ethereum, and is known as the Blockchain Trilemma.

A decentralized base layer blockchain distributes authority across all network participants such that no single entity can control or manipulate it. A secure blockchain is not only free of bugs that can be exploited, but the number of nodes and distribution of power across the nodes is crucial to the network’s resiliency against malicious attacks. Hence, decentralization and security are typically closely intertwined. Oftentimes, however, this limits the ability of a blockchain to support a large number of transactions and users without increasing fees and transaction times. Lowering the number of nodes on a network increases the scalability (less nodes that must come to consensus means quicker and cheaper transactions) but that comes at the cost of decentralization or security of the network.

The Blockchain Trilemma is therefore a useful framework for understanding and evaluating various blockchain networks. Understanding which tradeoffs in design choices the development team have made makes it easier to understand the strengths, weaknesses, and future roadmap of any blockchain project.

Bitcoin

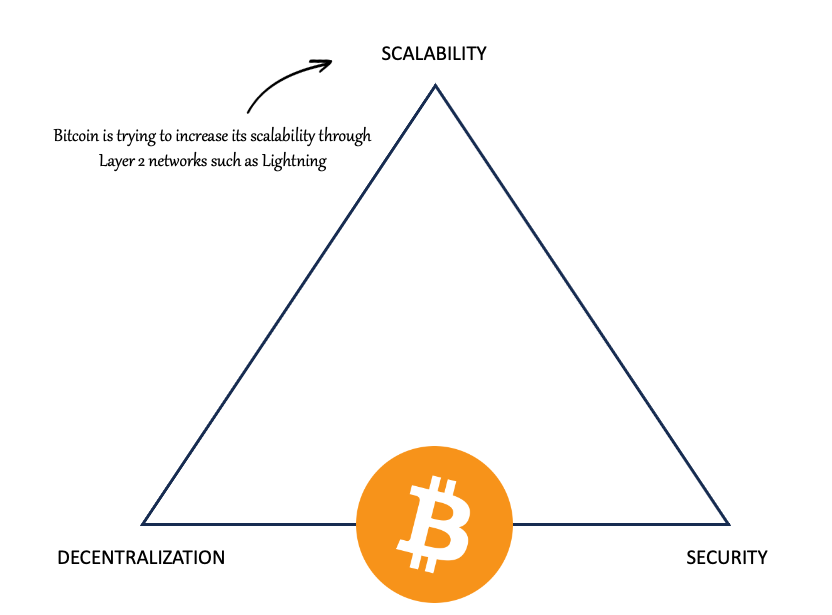

Let’s start by looking at Bitcoin using this framework. Satoshi Nakamoto prioritized decentralization and security when designing Bitcoin’s architecture. As a settlement network and store of value, this is a good choice. The fact that Bitcoin is fully decentralized means that no single entity can alter or manipulate bitcoin’s monetary policy. We therefore can have a high degree of certainty that we know bitcoin’s current supply, its ultimate total supply and its supply issuance rate from now until eternity. That is a key difference and advantage bitcoin has compared to traditional fiat currencies.

Bitcoin is also the most secure computing network ever created. Despite storing upwards of trillions of dollars of value and running for nearly 15 years, Bitcoin has never been hacked or had a fraudulent transaction. In fact, we previously covered why Bitcoin’s network might also become the best cyber-security network for storing and moving not just financial data, but any digital data. That security comes from, in large part, the decentralization of the largest computing network to ever exist.

However, those features do come with a tradeoff. In an effort to maintain its decentralization, Bitcoin’s block sizes have remained small (this was the crux of the Blocksize Wars back in 2015-2017). Smaller block sizes mean lower computing requirements to run a node. This in turn makes it easier for a greater number of people to participate in the Bitcoin network and therefore achieve greater decentralization. Today, anyone could run a node on the network with their home computer or laptop. However, smaller blocks also mean fewer transactions can fit in each block. This is why there is a limit to the number of transactions Bitcoin’s network can process every 10 minutes.

That cap on block size means Bitcoin’s base layer will never scale to accommodate the number of transactions necessary for it to become a payment network such as Visa and Mastercard. That’s ok because while Bitcoin’s base layer is not a great payment network, it does excel at being a settlement network. Bitcoin is already a faster, cheaper, more secure and more inclusive method for settling global transactions than ACH, SWIFT, or FedWire. Bitcoin is not trying to compete with credit card companies, it’s competing with the traditional financial plumbing that credit card companies are built on top of.

And much like credit card companies are built on top of traditional financial infrastructure, Layer 2 networks such as Lighting are being built on top of Bitcoin’s base layer. Lightning allows for near instant and nearly free bitcoin denominated transactions between two parties to occur without a centralized middleman and then settles those transactions back on Bitcoin’s base layer. Lightning has the potential to scale to many more transactions per second than Visa or Mastercard while being cheaper, more secure, and more accessible to anyone around the world.

Whereas Bitcoin optimizes for decentralization and security to become the greatest settlement network ever created, Lightning optimizes for scalability while leveraging the base layer’s security properties to hopefully one day become the greatest payment network ever created.

Viewed in this framework, Bitcoin’s design makes sense for the problems it’s trying to solve and explains the need for Layer 2 networks to address its shortcomings. But Bitcoin isn’t the only blockchain network. Whereas bitcoin aims to be money, other blockchain networks are solving different problems inherent with traditional financial infrastructure. Smart contract platforms aim to create ecosystems that allow developers to build decentralized applications such as exchanges, borrowing and lending, derivatives and more. If bitcoin is digital gold, then these networks are aiming to be decentralized versions of Amazon Web Services (AWS).

Smart Contract Platforms: Ethereum vs Solana vs Cosmos

While Ethereum is definitively the largest smart contract platform today, Solana and Cosmos have also become prominent projects in the crypto ecosystem. What is interesting about these three competitors, is that each has taken a different approach to solving the Blockchain Trilemma problem.

Ethereum: The Traditional Blockchain

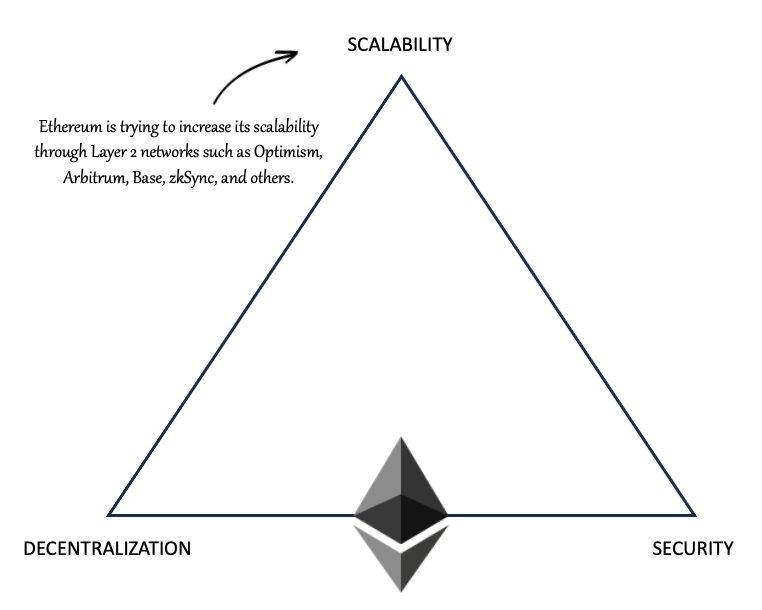

Ethereum has opted to make similar tradeoffs as Bitcoin, optimizing for decentralization and security. Ethereum is the second largest and second most decentralized blockchain network behind only Bitcoin because Ethereum has made being a validator as simple and accessible as possible. Anyone that owns ETH can stake their ETH, either on their own or through a staking service, and participate in validating transactions on the network. This helps maximize the number of global participants and keep Ethereum decentralized.

The tradeoff, however, is less scalability. We have seen in the past that Ethereum has been unable to keep up its transaction throughput as activity increases. When the number of people using Ethereum grows, transaction speed slows down, gas fees rise, and a bottleneck of transactions is created. During DeFi Summer in 2020 and the NFT craze in 2021, transactions could cost over $100 to execute on the Ethereum network due to the network not being able to keep up with demand.

Like Bitcoin, Ethereum is looking to scale its transaction throughput by leveraging Layer 2 networks built on top of the base chain. Layer 2 networks such as Optimism, Arbitrum, Base, zkSync and others can handle a far greater number of transactions and then bundle those transactions together to settle as one transaction on the Ethereum network. This allows for more transactions to get processed and fees to be distributed among a larger number of participants thus driving down the cost to use Ethereum.

Ethereum is also looking to implement sharding in future updates. We covered sharding back in May of this year. Sharding is basically parallel processing for blockchains. Sharding splits the Ethereum blockchain network into multiple, parallel blockchains, each one responsible for processing transactions of a given type. This greatly increases the space for more data which should allow Layer 2 networks to process more transactions. Simply put, sharding is akin to adding additional lanes to a congested highway and is likely to be implemented in 2024.

Solana: The High Transactions-Per-Second Blockchain

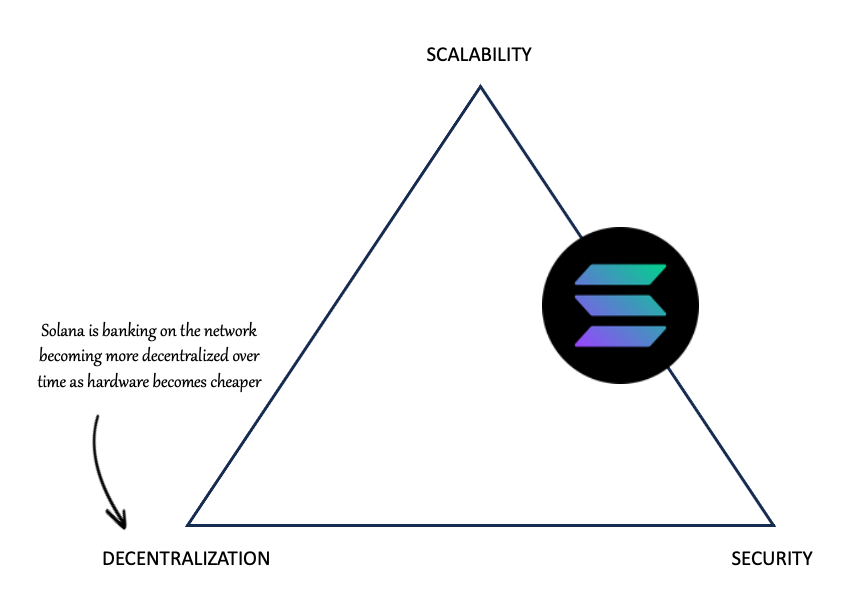

Compared to Ethereum, Solana takes a completely different approach. Rather than creating a modular style architecture the way Ethereum has, Solana has opted for a monolithic approach that aims to have all transactions executed on a single blockchain. In other words, Solana has chosen to optimize for scalability by building a blockchain that can handle a high throughput of transactions on a single layer.

The way Solana accomplishes this is by having much higher computing requirements for its validators. Validators on Solana must use ultra-high-end computers that can produce much greater processing power than a standard laptop. This increase in processing power results in faster transaction speeds. Whereas Bitcoin can handle about 7 transactions per second (TPS), and Ethereum’s base layer can currently handle upwards of 30 TPS, Solana’s TPS has peaked at about 65,000 TPS. Per the Solana whitepaper, Solana is theoretically capable of handling up to 700,000 transactions per second as the technology and bandwidth improve.

The downside of this approach is that this limits the number of validators on the network due to the significantly higher costs of the required computing thresholds. You can’t use your home laptop to be a validator on Solana’s network like you can for Ethereum and most people aren’t going to spend the money to buy the high-end computer required to be a validator. Not surprisingly, Solana has far fewer validators (roughly 2,000 as of writing this) on the network compared to Ethereum (over 950,000). For this reason, Solana’s validators are far more concentrated and the network is less decentralized.

Solana developers have made the conscious tradeoff to be less decentralized than Ethereum in exchange for greater throughput in the network and far less technical complexity. This greater concentration does pose risks as evidenced by the fact that Solana’s network has gone down 10 times over the past couple of years. That being said, it’s worth noting that the development team at Solana has been working on this issue and the network has not experienced any down time in over 8 months so the network appears to be maturing and becoming more reliable.

Solana’s decision to prioritize scalability means they are banking on three key trends to overcome the risks with greater centralization. First, most everyday users care far less about decentralization than crypto enthusiasts do. The next billion users are likely to want a good user experience, faster speeds, and lower costs without thinking about how decentralized their service is. On those attributes, Solana shines.

Second, the bet the Solana team is making is that they can create a network that is “decentralized enough.” Decentralization matters to achieve censorship resistance and greater security. However, there are diminishing marginal returns beyond a certain point of decentralization. Going from 100 to 1,000 nodes is significant in terms of decentralization but the amount of additional decentralization you really get going from 1 million to 10 million is unclear. The threshold for “enough decentralization” is very much up for debate but so long as Solana has enough nodes and is continuing to add enough new nodes over time, then users may be able to maintain censorship resistance with fewer validators.

Third, advancements in processing power and mining equipment should lower the cost for the high-end computers required to mine Solana so that over time it becomes more affordable. This decrease in price would allow a greater number of people to participate in the network in the future. The hope is that the Solana network should naturally become more decentralized over time as the cost of computing power goes down.

Cosmos: The Multi-Chain Ecosystem

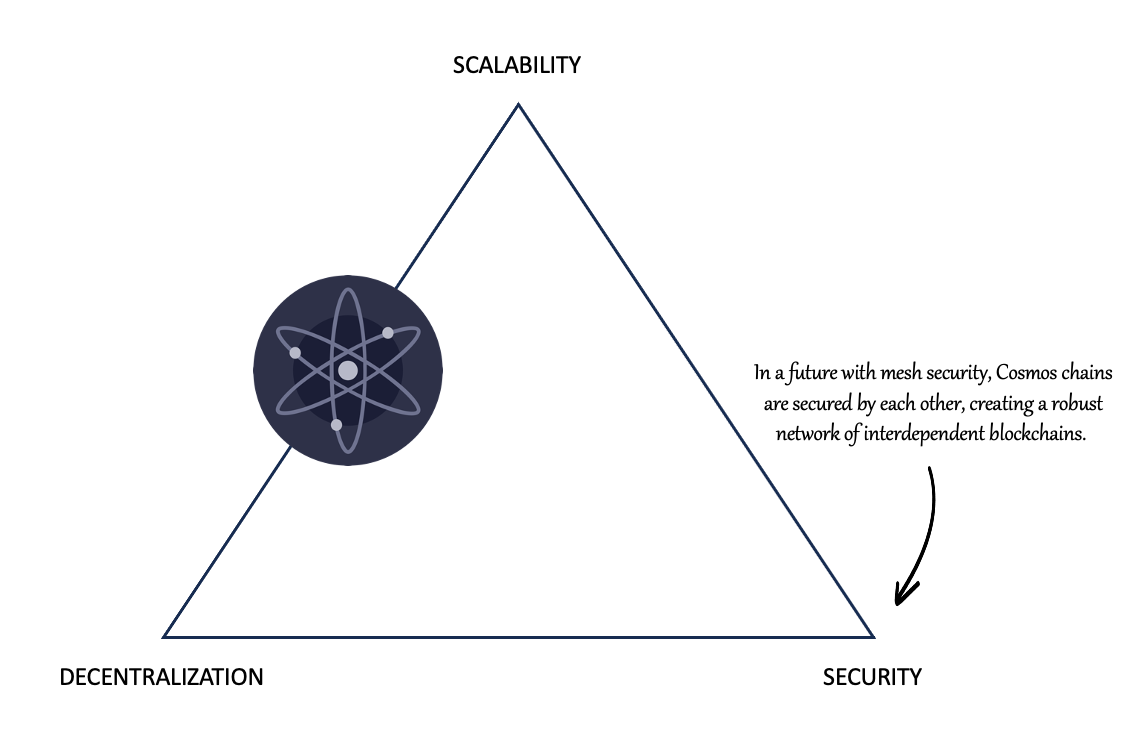

Cosmos is less a blockchain network and more a network of blockchains. Cosmos’s architecture resembles a hub-and-spoke model that allows any developer to create their own independent blockchain (often referred to as appchains or “zones”) and connect that blockchain to the Cosmos ecosystem. Cosmos’s design doesn’t try to unify a global shared state across one chain like Solana or across multiple chains like Ethereum, but instead is trying to build a network of app-specific blockchains that are interoperable with one another. Each application lives on its own chain and uses cross-chain-communication protocols to settle transactions between them.

This approach is decentralized as the hardware requirements of running a node are cheap (although not as cheap as Ethereum) which results in many different blockchains and many different validators in the ecosystem. Also, no single blockchain has sovereignty over another. Cosmos’s approach is also scalable because applications aren’t competing with one another for blockspace. As more applications get created, developers can simply spin up more blockchains to handle the demand. Theoretically, there is no limit to the number of blockchains that could be created within the Cosmos ecosystem.

The tradeoff is that this approach is less secure because each individual developer is responsible for their own validator security measures. The result is different chains within the network will have different degrees of security. Some chains may have more staked on their network than others making the smaller ones more vulnerable to attack. Some chains may be less rigorously tested and have bugs that can be exploited. More chains provide more attack vectors that could possibly cause ripple effects across applications in other chains.

To improve the overall security of the network, Cosmos announced earlier this year they are developing a concept called “Mesh Security,” a collaborative security model where chains become economically interwoven without infringing upon the autonomy of individual blockchains within the system. In the not-too-distant future, validators on one chain will be able to stake tokens to another “partner chain” and receive staking rewards for helping secure that partner chain.

This is important because in a Proof-of-Stake system, increasing the amount staked increases the network security. Smaller blockchains tend to have less value staked and as such are more prone to attacks by malicious actors. With Mesh Security, chains can collaborate to strengthen security in a bidirectional or multilateral manner by harnessing the combined market caps of participating chains. Theoretically this collaboration between chains should strengthen each other’s security while maintaining chain sovereignty.

Conclusion

The point of this article isn’t to say one design choice is better than another but rather, when building any technology there are inherent tradeoffs. The Blockchain Trilemma is a useful framework for identifying what is being optimized by any given blockchain network and the resulting strengths and weaknesses of those design choices. It’s not to say that Ethereum’s approach of many chains that all settle back to a single layer can’t scale. Or Solana’s monolithic single chain design won’t become more decentralized over time. Or Cosmos’s numerous sovereign chains each with their own settlement layer isn’t secure. It’s that each of these networks has consciously chosen to optimize for different attributes in building their ecosystems. It also means that each of them is now working on building solutions to address the third leg of the stool.

To be honest, I don’t know definitively which is the best approach. It’s still very much up for debate what the optimal solution will turn out to be. Perhaps one approach will win out or maybe all of them will prove to be viable for different applications. But I am excited to see entrepreneurs tackle this problem in various ways and see what comes of this experimentation.

In Other News

JPMorgan has carried out its first live blockchain-based collateral settlement transaction involving BlackRock’s tokenized money market funds.

Standard Chartered predicts ETH could hit $4,000 by the end of 2024 and $8,000 by the end of 2026.

Billionaire and legendary hedge fund manager Paul Tudor Jones is bullish on bitcoin and gold as geopolitical risks rise.

BlackRock CEO Larry Fink says he is seeing increasing global client demand for crypto.

WisdomTree extends the reach of its Prime app, plots new features.

The Stablecoin Bill is a vital upgrade for the US financial plumbing.

California Governor Gavin Newsom signed into law a crypto licensing bill which is set to take effect in July 2025.

Italian luxury car manufacturer Ferrari has started accepting payments in cryptocurrencies for car purchases in the U.S.

Citigroup is broadening its digital asset services through the launch of a pilot tokenizing client deposits.

The New York Attorney General filed a complaint against crypto exchange Gemini, crypto lender Genesis, digital asset investment firm DCG, over financial discrepancies relating to the Gemini Earn program.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS