By Brett Munster

Crypto’s data advantage

The cryptocurrency market represents a transformative difference when compared to traditional financial markets, particularly in the availability and richness of data.

In traditional financial markets, publicly listed companies typically report financial data on a quarterly basis—just four times per year. Even when they do issue these reports, while informative, often lack transparency in key areas. For instance, Google acquired YouTube in 2006, yet it didn’t disclose YouTube’s individual revenue until 2020, leaving investors to speculate for 14 years about its true financial impact. Even though YouTube had become a massive player, likely generating billions in revenue which would put it in the top half of the Fortune 500 all on its own, its financials were obscured. The streaming platform was so materially big that one quarter Alphabet executives even pointed to issues with YouTube as a key factor for disappointing financial results. This lack of visibility into crucial business segments makes it difficult for investors to assess a company’s overall health. How can shareholders make informed decisions without insights into high-impact business lines like YouTube, which can significantly affect a company’s performance?

In stark contrast, blockchain-based assets offer a level of transparency that is unparalleled. Every transaction that occurs on a blockchain is recorded permanently and publicly, along with detailed metadata. This means anyone—investors, analysts, or even casual observers—can access granular data about network activity in real time. Imagine if you were an Amazon investor and, rather than waiting for a quarterly report, you could access data on every single transaction occurring on Amazon’s platform, from sales by geography to product categories, all in real time. You could track which revenue streams were growing, which customer segments were most active, and where Amazon’s business was gaining the most traction. In the world of crypto, such transparency is the norm. Bitcoin, Ethereum, and other blockchain-based assets allow for real-time monitoring of network health and user activity, providing investors with a continuously updated stream of data.

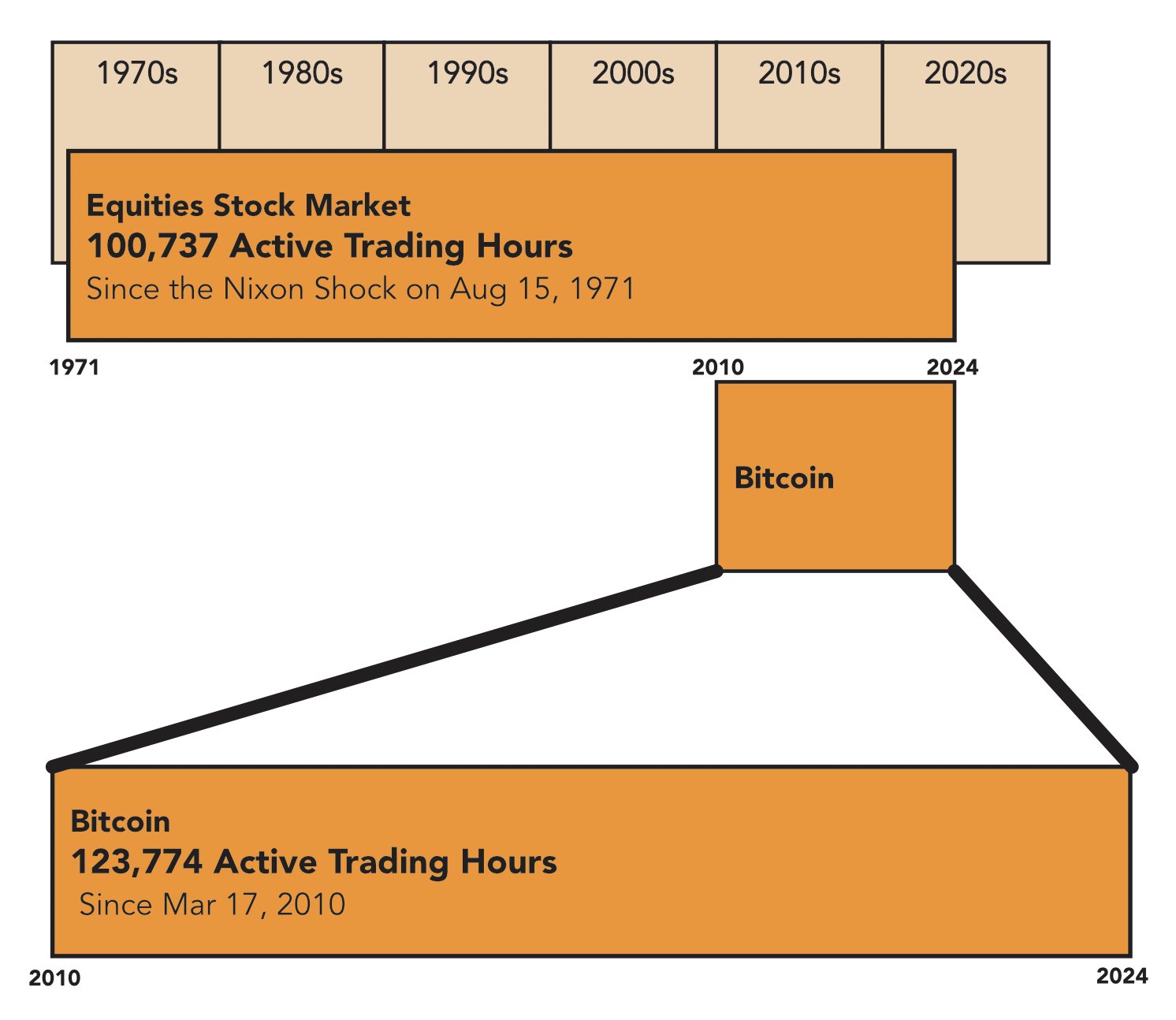

The differences between the stock market and crypto go beyond transparency. Traditional stock markets, such as the New York Stock Exchange (NYSE), operate on highly restricted schedules. The NYSE is open just 6.5 hours a day, five days a week, and it’s closed on weekends and holidays. That adds up to around 1,638 hours of trading per year. By comparison, there are 8,760 hours in a year, meaning the stock market is closed far more than it’s open.

Cryptocurrency markets, on the other hand, never close. They operate 24/7, 365 days a year, in a global marketplace that is accessible to anyone with an internet connection. This continuous operation means there are 5.3 times more hours of trading data available in crypto markets than in traditional stock markets.

This phenomenon led to an interesting observation made by bitcoin investor Anthony Pompliano. In bitcoin’s relatively short 15-year existence, it has amassed more trading hours than the stock market has since 1971, when the U.S. transitioned off the gold standard leading him to claim that “bitcoin is older than the fiat-era stock market.” This comparison is particularly striking because bitcoin was created precisely to address the issues arising from fiat currency debasement, which has fueled much of the stock market’s growth over the past several decades.

It’s important to clarify that this comparison focuses on the fiat era, not the entire history of the stock market. While the NYSE has existed for centuries, the era since the U.S. abandoned the gold standard represents a distinct period in which asset prices have been heavily influenced by the ability of governments to print unlimited amounts of money. If we isolate the stock market’s operation since the gold standard was dropped, bitcoin’s trading hours have already exceeded that period. By April 2053, if bitcoin continues trading continuously, it will have surpassed the total number of trading hours in the entire history of the U.S. stock market.

Crypto markets not only offer a constant flow of data but also eliminate the barriers that traditional markets impose. Investors always have access to their assets and can trade them at any time, without gatekeepers dictating when and how they can participate. In comparison, traditional markets, with their limited hours, periodic reporting, and restricted access, begin to feel antiquated and archaic. The cryptocurrency ecosystem, with its real-time data, constant accessibility, and global reach, represents a significant evolution in how financial markets operate, providing a level of openness and liquidity that traditional markets simply can’t match.

In a world where speed, transparency, and availability of information are crucial to making informed investment decisions, the advantages of cryptocurrency markets over traditional markets are becoming increasingly clear. As the crypto industry continues to evolve, its data richness and constant availability will likely make it an even more attractive option for investors seeking real-time insights and unimpeded access to markets.

SEC admits “crypto asset securities” is a made-up phrase

In June 2023, the SEC filed a lawsuit against Binance, the world’s largest cryptocurrency exchange, for various violations, including operating an unregistered securities exchange. Over the past few years, the SEC has pursued legal action against numerous crypto companies, often employing ambiguous and questionable legal theories. However, the latest development in the Binance case might be the most disingenuous yet.

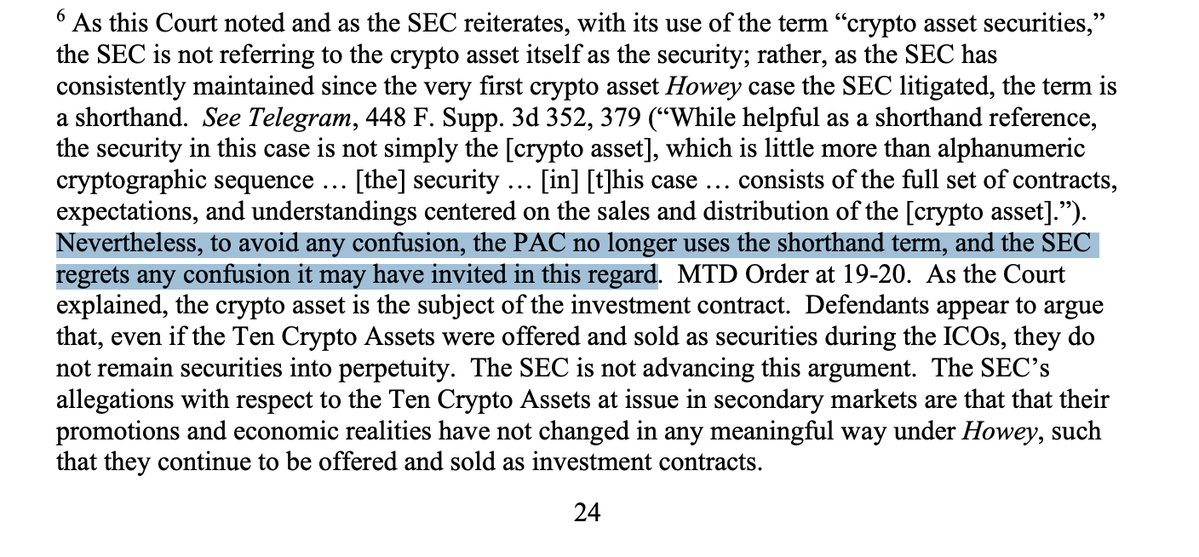

On September 13, 2023, the SEC filed a motion to amend its original complaint in their lawsuit against Binance. While the filing appeared routine, a significant change was buried within the document: the removal of every reference to the term “crypto asset securities.” In a footnote, the SEC acknowledged that it “regrets any confusion it may have invited” by suggesting that crypto tokens themselves are securities, clarifying that this was never their intention. The SEC also explained that even if a token was initially sold as a security, it does not necessarily retain that status once it is traded on an exchange.

Hold up, what now?

The SEC has spent the better part of the last four years and hundreds of millions of dollars of taxpayer money relentlessly suing nearly every crypto company in the U.S. precisely because the SEC claimed those companies were offering unregistered securities. Yet, now the agency admits, almost in passing, that it essentially invented the term “crypto asset securities” and never meant to imply that crypto tokens themselves were securities.

As Paul Grewal, Chief Legal Officer at Coinbase, pointed out, the SEC described XRP as a “digital asset security” in the first paragraph on page one of its complaint against Ripple. The SEC’s cases against Coinbase, Kraken, and others are premised on the idea that the tokens traded on these platforms are securities. Moreover, companies like Robinhood, Ethereum Foundation, ConsenSys, and Uniswap Labs have all received legal warnings—known as Wells Notices—based on the notion that their tokens are securities. SEC Chair Gary Gensler has publicly stated multiple times that he believes all tokens except bitcoin qualify as securities. Despite this clear history of repeatedly claiming that tokens are securities, the SEC can’t possibly be making the argument to a judge that they never meant to describe tokens as securities, can they?

The timing of this shift adds to the confusion. On the very same day the SEC informed a federal court that it would stop using the term “crypto asset securities” to avoid confusion, it issued a settlement order with eToro, using that exact term eight times. This blatant inconsistency is a striking example of the agency’s hypocrisy and muddled approach under Gensler’s leadership.

What’s even more troubling is how the SEC chose to handle this crucial clarification. Rather than issuing a public statement or an apology, the agency tucked the retraction into a footnote, as though trying to obscure the fact that it had misled the public and the courts for years. For an industry that involves millions of investors and billions of dollars in daily trading volume, such a nonchalant approach to regulatory clarification is irresponsible and bewildering. As SEC Commissioner Hester Peirce pointed out in her congressional testimony, “I think we’ve fallen down on our duty as a regulator not to be precise, and so tucking into a footnote that, yes, we admit that now, actually, the token itself is not a security, that’s something that we should have admitted long ago, and then started wrestling with the difficult questions.”

It’s pretty evident at this point that the SEC has very little legal ground to stand on given their arguments keep changing over the years. Initially, the agency directly classified tokens as securities, but after its loss in the Ripple case, it pivoted to arguing that the “ecosystem” surrounding a token could qualify it as a security. This theory was later rejected by a judge in the Kraken case. Now, the SEC’s latest argument in the Binance case is that although tokens were once sold as securities, the “promotions and economic realities” surrounding them have not materially changed, meaning that these exchanges are still violating securities laws.

It’s worth noting that each shift in the SEC’s legal strategy has followed challenges from the courts. The removal of the term “crypto asset securities” in the Binance case occurred only after the SEC faced yet another legal defeat. Instead of recognizing the limitations of existing laws and working toward the clear rulemaking that the crypto industry has long called for, the SEC has opted to revise its language and reframe its arguments. Now, the SEC must demonstrate that the sales of tokens on secondary markets, such as exchanges like Coinbase, are still part of an investment contract—an argument it failed to prove in the Ripple case. What the SEC’s next iteration of this argument will be after the current one fails remains to be seen.

The SEC’s misleading statements and inconsistent legal theories reflect a broader issue: the agency’s lack of transparency and accountability in its approach to crypto regulation. As Chief Legal Officer for Coinbase commented, “Gaslighting the American public is bad enough. But the United States government misrepresenting themselves to a Court in this way is something I’ve never seen in 28 years in the law.”

The crypto industry has consistently called for clear regulations and guidelines, yet the SEC has opted for a strategy of regulation by enforcement, hoping its self-created terminology would gain traction and support its cases. It’s important to emphasize that the term “digital asset security” appears neither in any law passed by Congress nor in any Supreme Court ruling. The SEC seemingly coined the term out of thin air and has used it repeatedly to justify enforcement actions against the industry.

Fortunately, the courts are increasingly pushing back, exposing the SEC’s struggle to maintain a coherent legal approach. Alongside its numerous losses in court, the SEC faced sharp scrutiny during a recent hearing in the U.S. Court of Appeals for the Third Circuit. Judges criticized the agency’s explanation for denying Coinbase’s request for crypto rulemaking, calling it “pretty darn close to vacuous” and devoid of substance. One judge even suggested that the SEC seems more interested in suing companies than in creating clear rules, stating that the agency “won’t tell you the answer until they prosecute you.”

It’s becoming evident that the SEC’s aggressive stance against the crypto industry is less about protecting investors and more about advancing Gary Gensler’s personal political ambitions. Instead of providing regulatory clarity and safeguarding investors, Gensler’s actions reflect a lack of a coherent framework, sound logic, or respect for due process.

This approach has drawn criticism from both sides of the aisle. During a recent Senate hearing, Republican Senator Tom Emmer accused Gensler of having “turned the SEC into a rogue agency,” while Democratic Senator Wiley Nikel condemned the SEC’s “misguided approach of regulation by enforcement and open hostility toward crypto.”

Even other SEC commissioners have begun publicly questioning Gensler’s leadership. During that same hearing, Commissioner Mark Uyeda, who has served under six chairmen, stated, “Our current state of rulemaking is, unfortunately, below average.” Commissioner Hester Peirce echoed similar concerns, noting the SEC’s enforcement actions resemble a game of “whack-a-mole” and “the classification of assets, even from our own perspective, seems to be changing over time.”

Katherine Minarik, Chief Legal Officer at Uniswap Labs, eloquently summarized the core issue:

“Whether or not you care about crypto, if you care about fundamental fairness in our legal system then you should be deeply concerned about the SEC’s approach to crypto. No government agency should work this way. Government agencies are trusted with enormous power to enforce laws which is why they are required to give us all notice of their view of those laws before bringing the full force of the government against any of us. But the SEC is not just inventing new theories of how to apply securities laws in its crypto cases as it goes along. It is contradicting itself with those theories. Sometimes within days or hours. Often within the same courthouse. The SEC has active cases right now premised originally on legal theories that it no longer stands behind when pressed. But instead of dropping those cases, the SEC moves to a new theory and continues on. It’s not about liking or disliking crypto. It’s about the way our system is supposed to work for all of us. America is better than this.”

Silvergate died of murder, not suicide

In March of last year, the two major crypto-friendly banks, Signature and Silvergate, were forced to close under controversial circumstances. As we covered at the time, the New York State Department of Financial Services (NYDFS) cited its decision to shut down Signature and place the Federal Deposit Insurance Corporation (FDIC) as the receiver as a measure to “protect depositors” and prevent “systemic risk.” However, as widely reported at the time, this reasoning did not hold up to scrutiny. According to Barney Frank, a board member of Signature Bank and co-author of the Dodd-Frank Act—the 2010 legislation designed to reform banking practices after the 2008 financial crisis—Signature was financially solvent when it was forcibly taken over. Frank publicly asserted that the bank’s closure was politically motivated, not based on any real financial threat. Further evidence of this emerged when Signature was sold to Flagstar Bank, but only under the condition that no crypto-related deposits would be included in the sale.

This situation highlights a troubling reality: regulatory agencies appeared to have taken control of a stable, private, and regulated company under the guise of protecting the financial system, when in fact, their actions likely were driven by political motives. If you’re wondering whether such actions are illegal, the answer is yes. Washington, D.C. law firm Cooper & Kirk, which had successfully sued the FDIC, Federal Reserve, and Office of the Comptroller of the Currency (OCC) over the original Operation Choke Point, released a white paper detailing how federal regulators once again overstepped their statutory authority. The firm accused these agencies of issuing enforcement actions without due process, in violation of the Administrative Procedures Act.

While the unlawful closure of Signature Bank was widely reported as a result of its involvement with the crypto industry, the narrative surrounding Silvergate Bank was initially different. It was commonly believed that Silvergate collapsed due to insolvency, following the broader downturn in the crypto market in 2022. However, recent developments suggest that this explanation is also false.

We chronicled Silvergate’s rise and fall in March of last year but apparently, we didn’t have all the facts at that time. With the bankruptcy proceedings finally underway, Silvergate executives are now allowed to speak publicly for the first time. In a 132-page sworn statement, Elaine Hetrick, the Chief Administrative Officer of Silvergate Bank, provided crucial evidence that directly contradicts the official narrative. According to Hetrick, “Following the rapid contraction of Silvergate Bank’s business, Silvergate Bank had stabilized, was able to meet regulatory capital requirements, and had the capability to continue to serve its customers that had kept their deposits with Silvergate Bank.” This testimony, supported by regulatory filings, reveals that Silvergate was not insolvent, as federal agencies had claimed. In fact, the bank voluntarily liquidated its business and returned all capital making every last customer whole without requiring government assistance—an action only possible if the bank had remained financially sound.

This testimony directly challenges the claims made by many, including Senator Elizabeth Warren, who asserted that Silvergate collapsed due to poor risk management and that banking for the crypto industry posed a systemic risk to the financial system. Contrary to this narrative, the real reason behind Silvergate’s closure appears to be much more alarming. The San Francisco Federal Reserve had ordered Silvergate to reduce its exposure to crypto clients to only 15% of its overall portfolio. Given that the vast majority of Silvergate’s deposits came from the crypto industry, this directive was effectively a death sentence for the bank. According to sources familiar with the matter, “If the 15 percent limit hadn’t been imposed, Silvergate would be thriving right now.” It is also important to note that such a mandate from the Fed is unconstitutional.

Hetrick further testified that the increased regulatory pressure on Silvergate and other banks servicing crypto businesses forced the institution into an untenable position. Silvergate was left with three options: radically reshape its business model away from crypto, seek to sell the bank under the looming threat of regulatory overreach, or wind down its operations to preserve value for its stakeholders. According to Hetrick, by early 2023, it was clear that “Federal Bank Regulatory Agencies would not tolerate banks with significant concentrations of digital asset customers, ultimately preventing Silvergate Bank from continuing its digital asset focused business model.”

The regulatory pressure on Silvergate did not end there. Nic Carter, who initially broke the story on “Operation Choke Point 2.0,” published an in-depth report drawing on recent evidence and commentary from sources close to the bank. According to these sources, the Federal Home Loan Banks (FHLB) declined to renew Silvergate’s monthly loan agreement due to political pressure from Senator Elizabeth Warren, worsening the bank’s financial situation. Warren also accused Silvergate of facilitating FTX’s illegal activities, which created an atmosphere of fear and uncertainty. This, in turn, fueled concerns and led to customers withdrawing funds. However, no criminal charges have ever been filed against Silvergate, and allegations of wrongdoing related to its connection with FTX remain unproven. In response to these allegations, the Federal Reserve, FDIC (Federal Deposit Insurance Corporation), and OCC (Office of the Comptroller of Currency) issued a joint statement warning banks they faced significant risks if they served the crypto space. Another joint statement from federal bank regulators, again on the risk crypto posed to banks, soon followed.

In short, Silvergate was systematically and unjustly cut off by banking regulators. The bank’s leadership, recognizing that their crypto business had been targeted, chose the most ethical course of action: they returned all customer deposits and voluntarily shut down the business.

Nic Carter also underscored the importance of Hetrick’s testimony. “Hetrick’s testimony is crucial because it provides direct, on-the-record evidence—under penalty of perjury—that confirms what we’ve long suspected. Silvergate wasn’t brought down by mismanagement or risky trades; they were forced out of business because the Federal Reserve decided they could no longer serve crypto clients.”

This testimony is crucial because it exposes a disturbing truth: both Signature and Silvergate, two financially sound banks, were deliberately targeted and shut down by regulators due to their involvement with the crypto industry. This is particularly important because many regulators and lawmakers have used the closures of these banks as “proof” that crypto is too risky for the banking system. These same closures have been leveraged to justify new rules and regulations designed to make it nearly impossible for banks to serve the crypto industry.

And regulators have acted on this justification. Customers Bank and Cross River Bank, which stepped in to replace Silvergate and Signature, have both faced regulatory punishment. In May 2023, the FDIC issued a consent order against Cross River, severely limiting its crypto activities. Similarly, in August 2024, the Federal Reserve Bank of Philadelphia took enforcement action against Customers Bank, citing deficiencies in the bank’s “risk management practices” and compliance with anti-money laundering laws related to its digital assets business.

It is deeply troubling that federal agencies took illegal actions to force the closure of two financially stable banks, and then used these closures as a pretext for imposing even stricter regulations on an industry they appear intent on eliminating from the banking system. While it seems unlikely that anyone will be held accountable for what happened to Signature or Silvergate, at least the truth has now surfaced. The evidence shows that cryptocurrency is not the threat to the banking system some have claimed it to be.

In Other News

Blackrock recently released a new report calling bitcoin “a unique diversifier.”

BlackRock revealed it’s quietly preparing for a $35 trillion Federal Reserve dollar crisis with bitcoin.

The SEC found itself under fire by Congress over its heavy-handed approach to crypto.

Bitcoin rallies past $62.6K after BlackRock white paper and Fed cuts interest rates by 50 bps.

Ether rebounds off key support, signaling long-term bullishness.

Franklin Templeton plans mutual fund on Solana.

SEC greenlights Nasdaq listing of options for BlackRock’s Bitcoin ETF.

Visa has developed a new product to help banks issue fiat-backed tokens on the Ethereum network.

PayPal enables U.S. business accounts to buy, hold and sell crypto.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.

BACK TO INSIGHTS